New Delhi: Every June, Pakistan’s Ministry of Finance issues two pivotal documents in close succession. The Economic Survey provides an analysis of the country’s past economic performance, while the Federal Budget outlines the government’s future economic strategies. When examined individually, each document may appear optimistic. But when read together, they reveal a fundamental contradiction in Pakistan’s current economic situation.

The nation has achieved stabilisation without transformation, satisfied its creditors without adequately serving its citizens, and its most lauded fiscal accomplishment is deteriorating, even before it is fully realised.

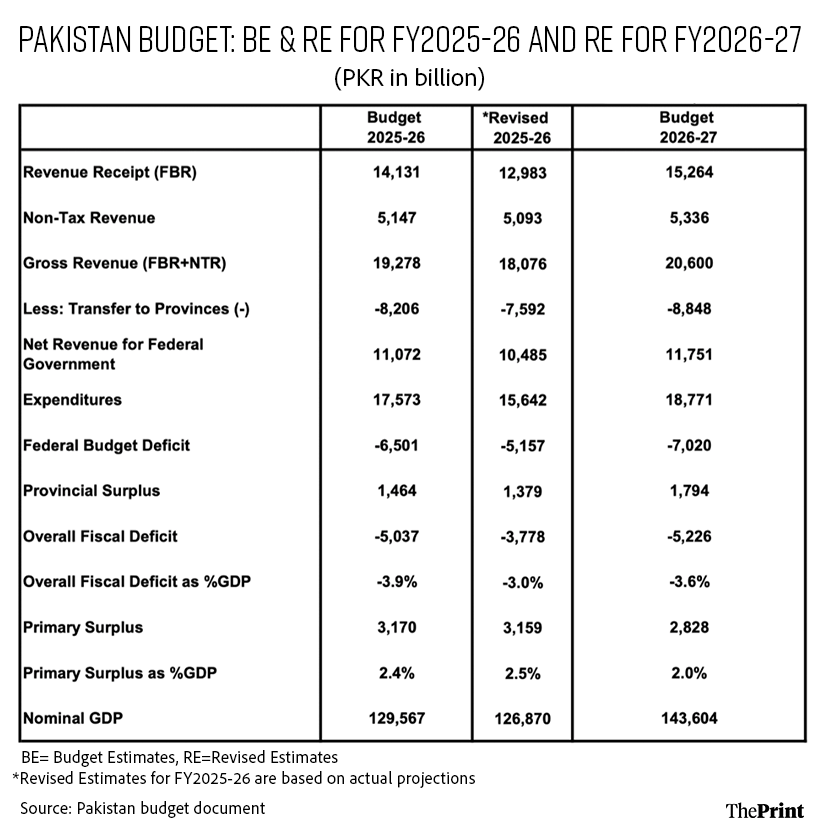

The Pakistan Economic Survey 2025-26 presents a narrative of recovery from crisis. GDP growth has increased to 3.7 percent from the previous fiscal’s 3.18 percent. Inflation, which reached a catastrophic 28-38 percent in FY2023, averaged at 6.2 percent over the first 10 months of the financial year. The current account, traditionally in deficit, recorded a surplus of USD 72 million in the first three quarters. Foreign exchange reserves have reached multi-year highs. A primary surplus of PKR 4091.5 billion, representing 3.2 percent of GDP for July-March FY2026, is highlighted as a historic achievement. Pakistan’s financial year begins on 1 July and ends on 30 June.

These figures are genuine, and the efforts behind them substantial. Pakistan has retreated from the brink of economic collapse.

However, stabilisation does not equate to development. It merely removes an impediment. When you place the Economic Survey beside the Federal Budget for FY 2026-27, the disparity between Pakistan’s current state and its developmental aspirations becomes starkly evident.

Surplus built on borrowed time

The acclaimed primary surplus deserves examination prior to celebration for Pakistan. It rests on two elements that are neither structural nor sustainable.

First, markup payments decreased by 23.2 percent—not due to a reduction in the country’s debt burden, but as a result of State Bank of Pakistan’s decision to lower interest rates following the crisis period. Markup payments are the interest costs the government pays on its accumulated borrowings, basically the price of carrying public debt. The larger a country’s debt stock, and the higher the interest rates at which it has borrowed, the heavier this burden becomes.

The crisis period spanned roughly FY2022 through FY2024, when Pakistan faced its worst economic emergency since Independence, marked by inflation peaking at 38 percent, a near-sovereign default, and the SBP’s policy rate being raised to a record 22 percent. The rate-cutting cycle began only in June 2024, making the markup payment decline in the subsequent fiscal year a direct consequence of that belated easing.

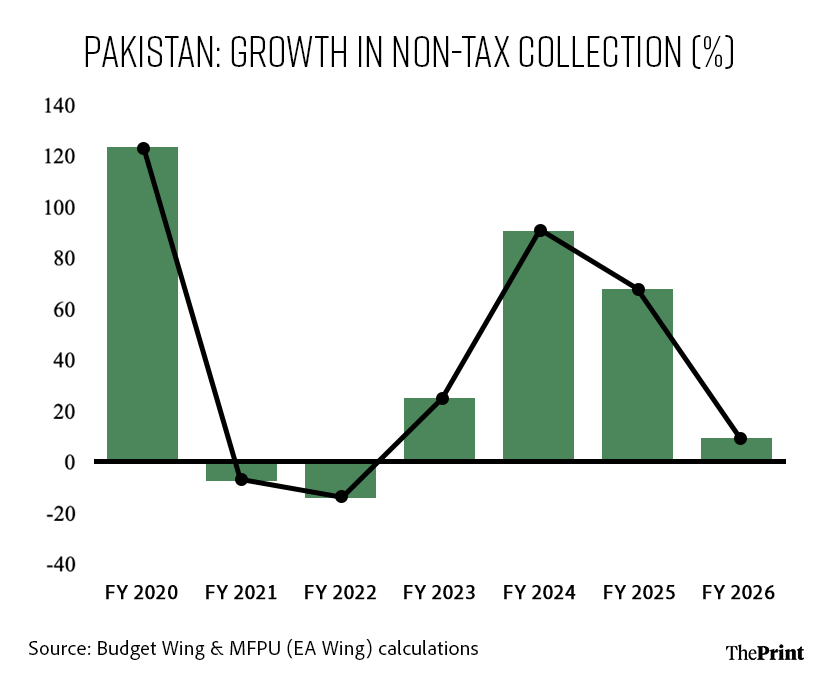

More significantly, the SBP transferred profits amounting to PKR 2,428 billion to the government, a windfall resulting from high-interest earnings during the crisis years that inflicted substantial damage.

Excluding these two factors, the fiscal outlook appears considerably less remarkable.

Examining the Federal Budget for FY 2026-27, SBP’s profit is anticipated to decline to PKR 1,435 billion, representing a decline of nearly PKR 1 trillion in a single non-tax revenue category.

This is not a matter of forecast uncertainty. It is a reflection of financial inevitability. When a central bank’s earnings from crisis periods normalise, they do so predictably. The overall federal fiscal deficit for FY 2026-27 is projected at PKR 7,020 billion, exceeding the revised estimate for FY 2025-26. The primary surplus is expected to decrease from 2.5 percent of GDP to 2 percent. Thus, the peak of Pakistan’s fiscal consolidation has already been surpassed.

Growing in the wrong direction

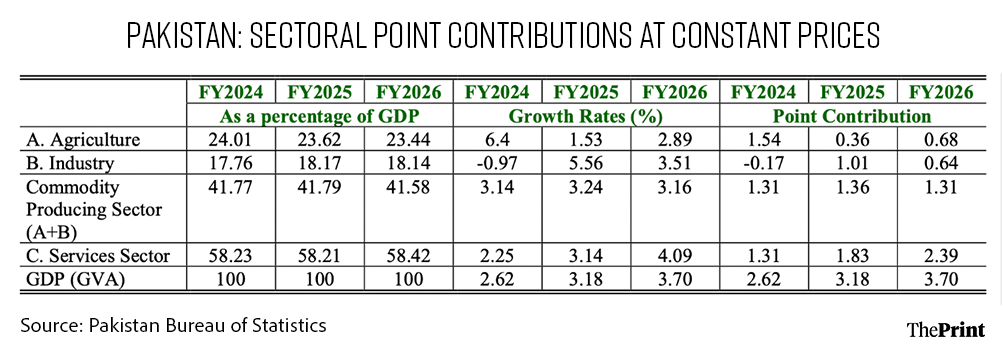

The sectoral breakdown presented in the Economic Survey reveals a noteworthy statistic for economists. Of Pakistan’s 3.7 percent GDP growth, the services sector accounted for 2.39 percentage points, surpassing the combined contributions of agriculture (0.68 points) and industry (0.64 points).

Although large-scale manufacturing has rebounded from the previous year’s contraction, the structural core of the economy continues to be centred on retail trade, public administration and digital services.

In the field of development economics, the term “premature deindustrialisation”—as identified by Dani Rodrik—describes a significant challenge faced by contemporary developing economies. These countries often bypass the manufacturing stage of economic growth, transitioning directly to a service-based economy without establishing a robust industrial foundation. This results in economic activity that fails to generate large-scale employment, exports that lack substantial export capacity, and growth that does not lead to structural transformation.

In contrast, East Asian economies, which have achieved sustained development, invested between 30-40 percent of their GDP during periods of rapid growth. Pakistan’s investment-to-GDP ratio, however, has stagnated at approximately 14.38 percent for several years. Despite its challenges, India has strategically promoted manufacturing investment—a path not pursued by Pakistan.

The Federal Budget for 2026-27 does not offer a solution. The total allocation for the Public Sector Development Programme (PSDP) remains at PKR 1,000 billion, unchanged from the previous year in nominal terms, indicating a real decline. The allocation for Defence Affairs and Services is set at PKR 3,010.9 billion for the upcoming year, while education has received PKR 117.7 billion and health PKR 37.4 billion.

Notably, the defence budget is approximately 25 times the education budget, and 80 times greater than that of health. In a nation where the Economic Survey reports education expenditure at merely 0.8 percent of GDP, these budgetary allocations do not reflect a government recognition of its structural issues, nor a commitment to addressing them.

An economy sustained by its diaspora

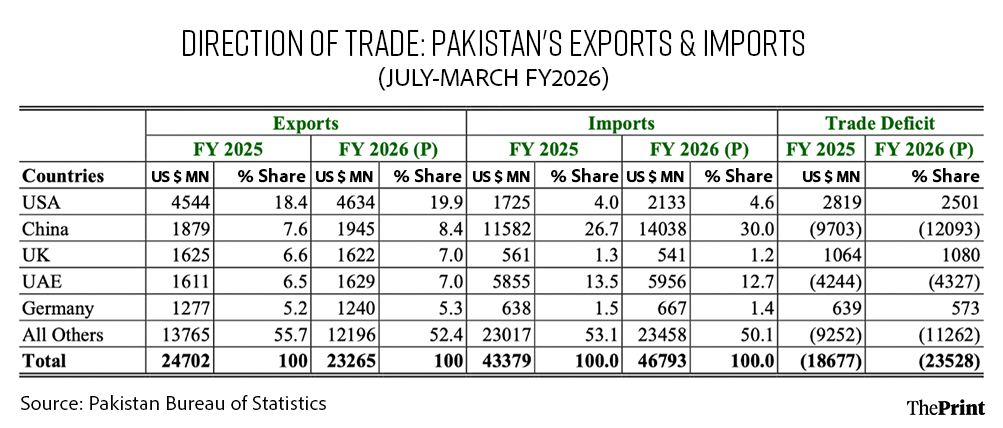

Among the insights provided by the Economic Survey and Budget, the external account narrative is particularly illuminating. Pakistan’s current account surplus of USD 72 million is primarily attributable to workers’ remittances, which reached USD 30.3 billion in the first three quarters, marking an 8.2 percent increase. In contrast, merchandise exports decreased by 5.8 percent to USD 23.3 billion. This indicates that Pakistan is not achieving economic success through competitive production, but is reliant on the labour of its expatriates.

The direction of trade data in the Economic Survey highlights a significant structural issue.

Pakistan’s bilateral trade deficit with China alone amounted to USD 12.1 billion in the first three quarters of FY2026, with exports of USD 1.9 billion and imports of USD 14 billion. Although the China-Pakistan Economic Corridor (CPEC) has facilitated infrastructure investment, it has not—even after a decade—enhanced export capacity. This imbalance represents a policy shortcoming, which neither the Survey nor the Budget adequately addresses.

Meanwhile, IT exports, which the Survey identifies as a positive development, increased by 19.7 percent, reaching USD 3.38 billion from July 2025 to March 2026. While this growth is promising, it is important to note that India’s IT services sector generates a similar amount every two weeks—a disparity not acknowledged in either document.

In macroeconomic terms, Pakistan has achieved what is known as successful stabilisation: inflation down from crisis levels, reserves replenished, IMF tranches secured, and a primary surplus achieved. By the standards of multilateral institutions, Pakistan has met the necessary criteria. However, for the 252 million residents, 28.9 percent of whom live below the poverty line—a figure that is increasing—the situation is far less favourable.

The Survey and the Budget together provide a clear observation: Pakistan has bought itself time. However, they fail to address how this time will be utilised as the policies outlined do not tackle this issue. Stabilisation without transformation ultimately leads to a prolonged journey to the same endpoint.

(Edited by Mannat Chugh)