IL&FS is an unwieldy, opaque hydra. More than size, it’s the diffuse nature of its operations that should worry its new directors.

New Delhi: For its roads, power stations and other useful assets to live, a bankrupt Indian infrastructure lender must die.

Infrastructure Leasing & Financial Services Ltd. was seized by the government this month after unexpected defaults on its $12.5 billion of debt spread panic through money and equity markets. A new six-member board chaired by banker Uday Kotak will have to sort out the mess.

IL&FS is an unwieldy, opaque hydra that doesn’t just finance long-term assets, but also constructs, operates and owns them. It has 348 entities for the government-appointed board to untangle – double the number of subsidiaries, associates and joint ventures listed in the firm’s last annual report.

More than size, it’s the diffuse nature of operations that should worry the directors. That, and the fact that neither the Indian company law nor the bankruptcy code is prepared to handle the insolvency of a large, systematically important financial institution.

Getting the job done in six to nine months, as the government hopes, is next to impossible. But if New Delhi provides a liquidity backstop for the group’s debt coming due over the next year, perhaps by swapping it with state-guaranteed long-term paper, the nervousness around defaults will subside. That will buy Kotak more time to extract maximum value for stakeholders and minimize the hit to taxpayers.

Kotak’s first instinct must be to sell the group’s construction arm, a business where he and the other directors have little experience. In its previous life, publicly traded IL&FS Engineering and Construction Co. used to be run by the family of a software tycoon who admitted to cooking his outsourcing firm’s books and went to jail. When the government carved up B. Ramalinga Raju’s fraud-ridden empire in 2009, IL&FS bought Maytas Infra Ltd., and later renamed it.

Now, this asset is problematic on several levels. IL&FS Engineering’s consolidated net debt is $370 million, while its equity is negative $19 million. To keep the business – and its messy payment disputes with customers – would be folly. A sale to a distressed-asset specialist would mean writing off the $215 million the group has put into the business as equity and debt, but at least it would stop throwing good money after bad.

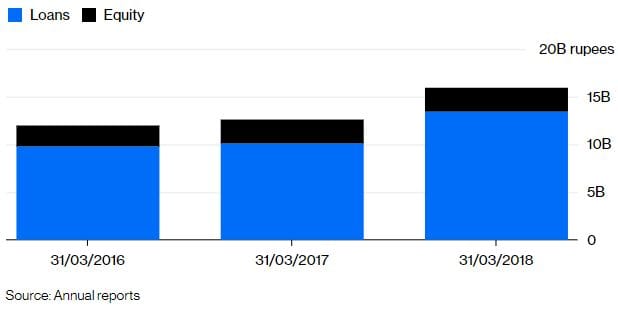

Throwing Good Money After Bad

Loans from its parent are keeping IL&FS Engineering & Construction Co. afloat; the bankrupt Indian infrastructure lending group must sell this unit and write off its exposure

Next stop for the new IL&FS board should be its 13,000-plus lane kilometers of road assets. IL&FS Transportation Networks Ltd. has missed payments on its debt. Here, a little help from the government would go a long way. Granted, the current debt to tangible equity ratio of 7 is too high. But rather than pump in fresh capital or force haircuts on creditors, New Delhi could swap their debt for long-term paper issued by the state-owned National Highway Authority. These bonds would pay less, but for creditors such quasi-sovereign securities would be safer to hold than defaulted notes of a private borrower.

The highway authority would manage the roads and collect revenue from tolls or annuity payments. The new bonds could be serviced without taxpayers’ largess. What’s more, once interest costs stop eating into as much as 75 percent of the business’s Ebitda, there will be something in these projects for equity holders, including the IL&FS parent.

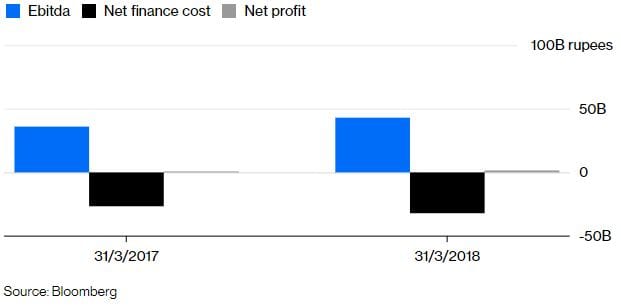

Costly Finance Takes a Toll on Roads

A big part of IL&FS Transportation Networks Ltd.’s earnings before interest, taxes, depreciation and amortization goes into paying finance charges, almost wiping out net profit

A similar solution could be worked out for power, where assets of IL&FS Energy Development Co. could perhaps be given to the government-owned National Thermal Power Corp. to manage.

It’s still not too late to save the financing business. Infrastructure lending is the core that IL&FS founder Ravi Parthasarathy should have stuck to, rather than try to capture value at every step for 30 years – before he took one last fat paycheck and left for health reasons in July.

After this unscrambling, the parent will have one owner left. The employees’ welfare trust deserves to be left hugging a dead shell, given how well staff appear to have done from IL&FS. Ensuring that should be Kotak’s last task.

–Bloomberg Wire