New Delhi: More and more poor households in India now have access to institutional sources of credit, reveals the latest round of the All India Debt and Investment Survey (2019) released by the Ministry of Statistics and Programme Implementation earlier this month.

The data shows that in the last couple of years, this enhanced institutional credit has led to a decrease in usury, a common practice in rural India, in which poor households are charged exorbitant interest rates on loans they get from traditional moneylenders.

According to the survey, in 2018, institutional credit amounted to about 66 per cent of the total outstanding credit in rural areas, the highest since Independence.

In sharp contrast, nearly five decades ago in 1971, institutional credit was available to hardly 29 per cent of the households in India’s rural areas.

The survey, however, notes that the change has not occurred uniformly everywhere. In certain states, non-institutional creditors still dominate the lending business, but the trend is shifting downwards there too.

As on 30 June 2018, non-institutional financiers, mostly professional money lenders and relatives, accounted for about 34 per cent of the total credit in rural India, the survey states.

But in states such as Andhra Pradesh, Telangana and Bihar, they still accounted for more than 50 per cent of the total outstanding loans. Even in Jharkhand (40.6 per cent), Odisha (40.8 per cent), Rajasthan (46.6 per cent), Uttar Pradesh (37.2 per cent) and Madhya Pradesh (34.4 per cent), non-institutional lending was a bit higher than the national average of 34 per cent in rural areas.

But the share of non-institutional credit in rural areas is falling in all these states except Andhra Pradesh and Telangana.

According to the survey, Bihar saw the steepest fall in non-institutional rural credit, from about 78 per cent in 2012 to 51.5 per cent by 2018.

In Rajasthan, the share of non-institutional agencies to total rural credit fell from 69 per cent to 47 per cent in the same time period. The fall in Odisha (43 per cent to 41 per cent) and Uttar Pradesh (43 per cent to 37 per cent) in this regard was relatively slow.

Also read: Rich getting richer, poor getting poorer — answer to India’s V vs K economic recovery question

Sahukars losing out

Between 2012 to 2018, professional money lenders lost out to commercial banks, the data shows.

In 2012, traditional moneylenders and agriculture lenders accounted for 33 per cent of the total rural credit. In 2018, their share has come down to just 22 per cent. This figure includes lending by both professional and agricultural lenders.

Traditional moneylenders or sahukars have existed in Indian villages for centuries. These lenders charge a usurious amount of interest that often puts the debtor into a debt trap.

According to the All India Rural Credit Survey conducted by the Reserve Bank of India in 1951, these money lenders accounted for about 70 per cent of the total rural credit at the time.

The mere convenience of low or no collateral and availability made these lenders accessible to the poorest households in rural India and they faced no competition from organised banking even decades after India’s Independence.

Until 1971, non-institutional credit accounted for over 70 per cent of rural India’s debt, which fell to 38 per cent by 1981 as effects of 1969 bank nationalisation started showing results, with bank branches being spread across the country.

The debt survey notes that credit by scheduled commercial banks, which did not account for even a percent of rural India’s credit in 1951, have recorded a great jump. As of 2018, about 42 per cent of rural India’s credit was channelised through these banks, up from 25 per cent in 2012.

According to Narayan Chandra Pradhan, assistant advisor at the Reserve Bank of India, “Rural finance is picking up after the 2014 Jan-Dhan scheme, but real helpers are Non-Banking Financial Corporations (NBFCs), small finance banks and cooperatives through the mobile banking system.”

While public sector banks, since nationalisation, have been at the forefront of providing credit to rural areas, private banks have played their role, thanks in part to increased financial literacy.

Over a period of time, ever since people have started receiving subsidies directly in their accounts, transparency in transactions has brought millions of account holders on paper.

India’s leading private sector bank, HDFC, currently caters to 1 lakh villages, which it envisages to expand to 2 lakh villages by 2023, Rahul Shukla, the bank’s Group Head (Commercial and Rural Banking) told ET Now.

Shukla also said that if the banks want their businesses to grow sustainably, then they’ll have to move to the hinterlands.

A senior private bank official, who did not wish to be named, told ThePrint that “even if banks can’t set up a branch, they keep sending their agents to the villages”.

“Direct transfer of sale proceeds to the farmers’ bank accounts, increase in use of ATM cards has put their financial transactions on record, which has reduced the hurdles farmers faced while accessing credit from a bank,” the official said. “The competition is rising, more and more private banks are trying to tap this market.”

ThePrint reached SBI Group Chief Economic Advisor, Soumya Kanti Ghosh, via email for a comment, but received no response till the time of publishing this report.

Who benefitted the most?

The fall of traditional money lenders has actually benefited people from the lowest stratum of the economy.

Data shows that the shift from professional money lenders to commercial banks was the highest among the bottom 30 per cent asset holding classes (or poorest 30 per cent).

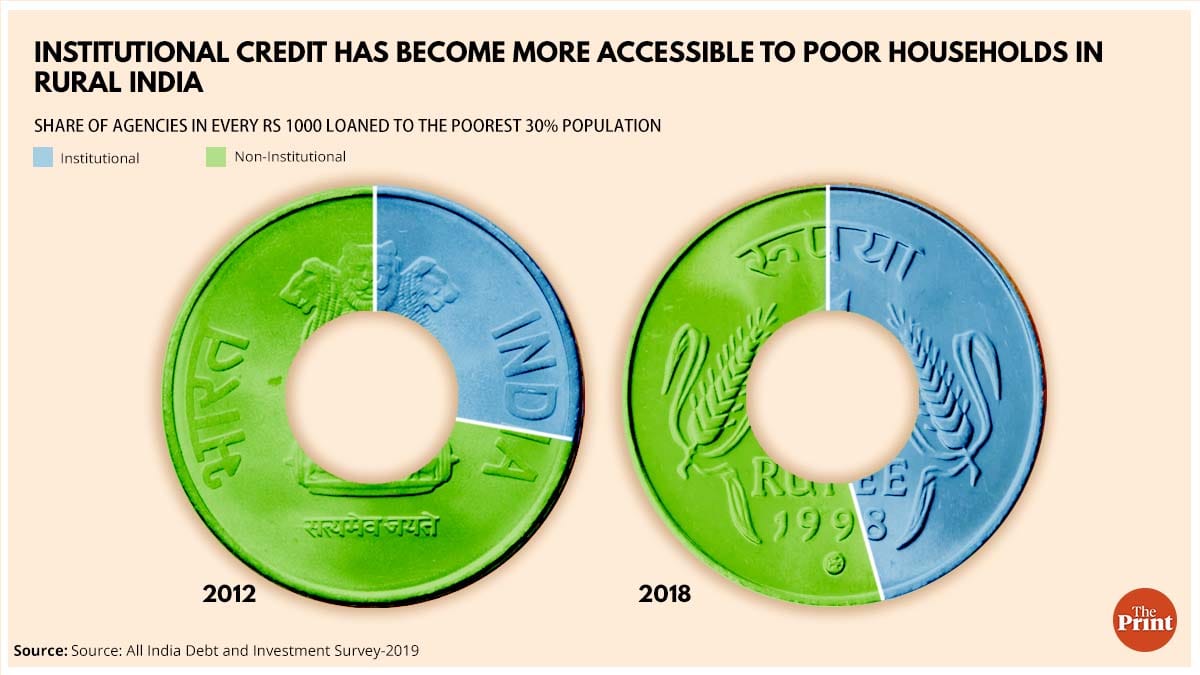

In June 2012, according to the survey, for every Rs 1,000 that was loaned to the poorest 30 per cent, over Rs 500 had come just from money lenders. This figure in 2019 has been halved as they were the source of credit for only Rs 277 for every Rs. 1000 loaned to this particular demographic.

This is primarily because institutional sources of credit have become more accessible in these areas, the survey states. In 2018, for every Rs 1,000 loaned to the poorest 30 per cent, more than Rs 453 came from institutional sources, a nearly 60 per cent jump from Rs 286 in 2012.

This growth was primarily led by the scheduled commercial banks, whose share in total credit given to poor rural households has almost doubled between 2012 and 2018. In 2012, SCBs accounted for about Rs 107 for every Rs 1,000 that was loaned to rural India, which jumped to 233 by 2018.

This, according to JNU professor Praveen Jha, is a “welcome change”. He, however, said it still needs scrutiny with respect to the agrarian crisis that has prevailed over time.

“We need to inspect the new sources of institutional finances. If people are pawning gold for a bank loan, then it will show up in institutional credit but this might not reflect the distress in the economy,” he told ThePrint.

“Rise in institutional credit among the poorest households might mitigate the harms of the usurious rates charged by moneylenders otherwise but we have to acknowledge that increase in the cost of cultivation has made agriculture a less profitable business,” Jha added. “This essentially means that the farm distress cannot be completely ruled out even if the source of credit has improved.”

(Edited by Arun Prashanth)

Also read: India’s world-beating GDP data can’t hide the pain of the pandemic

*A previous version of the story erroneously said HDFC has over 1 lakh branches in rural areas, which has been corrected.