New Delhi: India’s three-decade-long growth story was built on a critical engine: Information Technology (IT) services exports—worth $225 billion a year—that funded India’s current account, created a million middle-class jobs each year, and powered domestic consumption.

That engine is now slowing due to the maturing global outsourcing market and the substitution of cognitive labour by Artificial Intelligence (AI). The consequences are already visible: decelerating consumption, softening real estate prices in IT cities, and mounting pressure on the rupee.

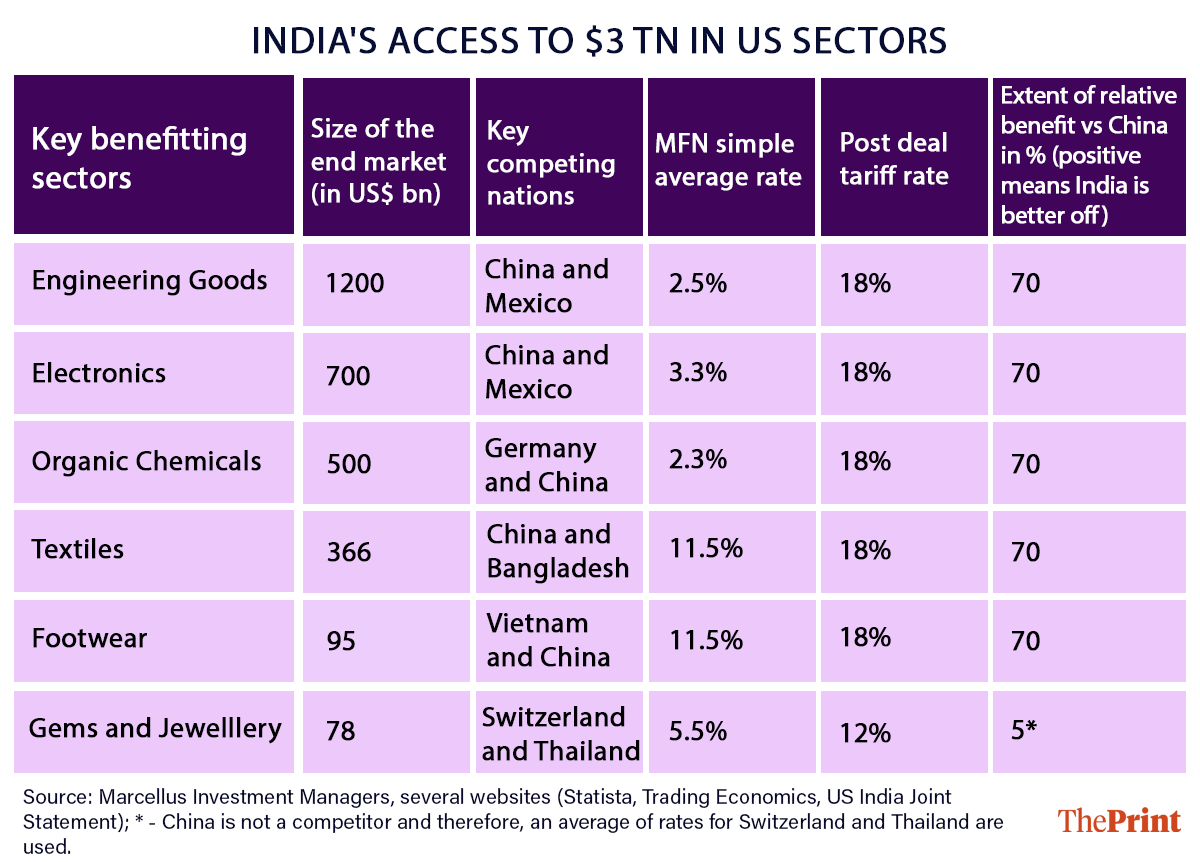

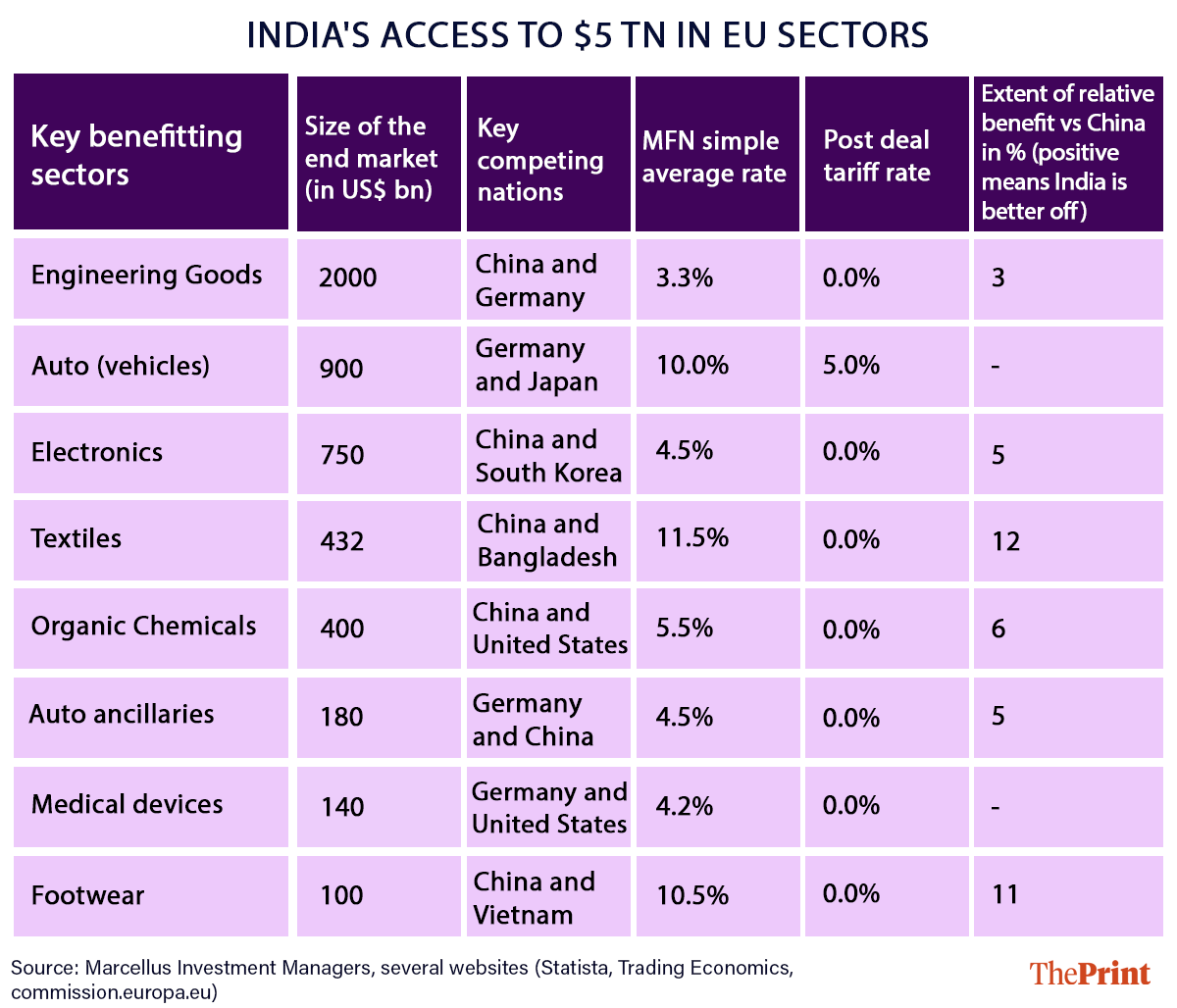

Yet within this disruption lies a significant structural opportunity. A depreciating INR, combined with landmark Free Trade Agreements (FTAs) with the United Kingdom and the European Union and another interim FTA framework with the US, gives India tariff advantages over China, Vietnam, and Bangladesh.

Export-led manufacturing is poised to take over as India’s next engine of growth. This transition from IT to manufacturing will be uneven and painful in the near term: the winners are few and localised, while the losers are many and dispersed.

In Principles of Political Economy (1848), John Stuart Mill wrote, “In every age, there comes a time when the old ways of earning a living pass away and new ones must be built in their place. The nation that moves first, with clear eyes and steady nerve, inherits the next era of prosperity. The nation that mourns too long for what was lost shall find itself mourning its future as well.”

India’s economic identity was built on IT services

India’s post-liberalisation story is, in many ways, a story about software.

For over three decades, IT services have not merely been an industry—they have been the very engine of India’s integration with the global economy. Since the early 1990s, India’s largest export by value, after petroleum products, has been IT services, generating roughly $225 billion per annum in foreign exchange earnings in FY2024-25. This sector financed India’s current account deficit, allowing the country to import the essentials of modern life—electronics, energy, machinery—predominantly from China and the West.

Beyond the balance of payments, IT services created a class of urban, aspirational, middle-income professionals. It generated jobs for millions of engineering graduates, funded consumption across metros, and—through that consumption—drove ancillary employment in real estate, retail, and services. Bangalore, Hyderabad, Pune, and Gurgaon became cities which grew up around the IT services sector.

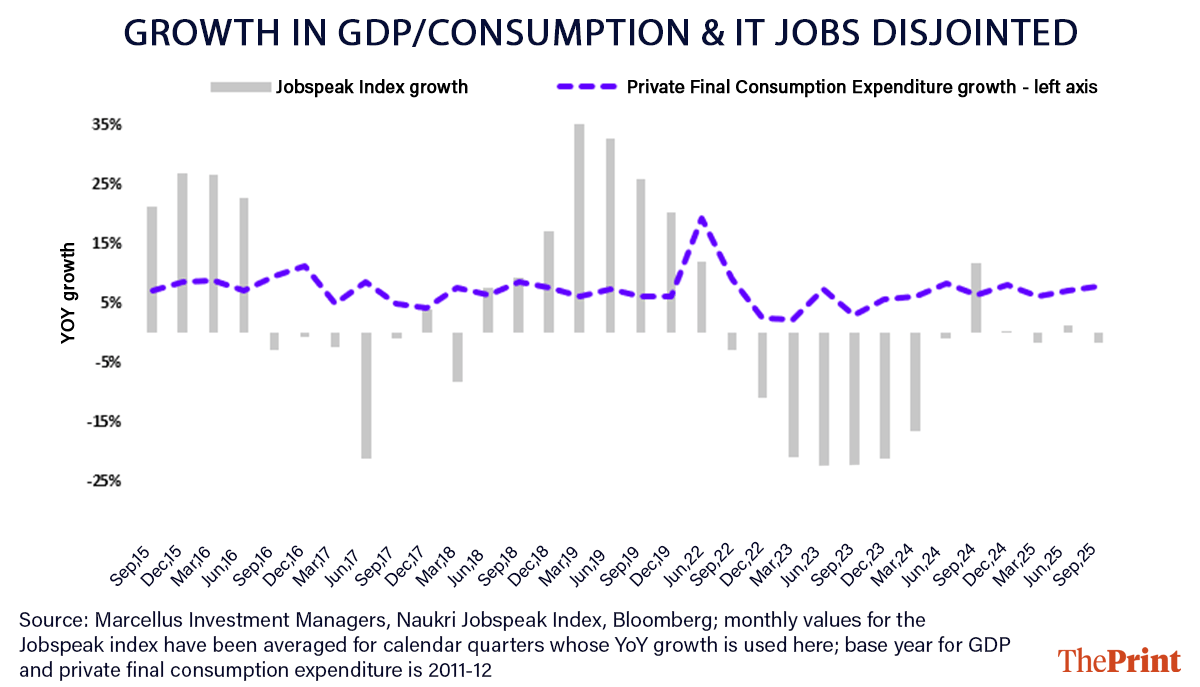

The sector’s steady expansion over 30 years was not merely an industry success story; it was the primary driver of India’s economic growth rate, anchoring the country’s fiscal stability and its external account. The four largest listed IT services firms—TCS, Infosys, HCL Tech, and Wipro—grew revenues at a compound annual growth rate (CAGR) of 15.8 percent between FY2005 and FY2020. During this period, they absorbed over a million new employees each year and generated further waves of ancillary employment. As the graph below shows, however, this era of synchronised growth between IT jobs and consumption has now decisively broken down.

Also Read: Borrowing to survive: Indian households are saving more, why are they still in debt?

A structural shift is bringing this era to an end

What took 30 years to build is now fraying—not because of a single shock, but because of two compounding structural forces fundamentally altering the dynamics of India’s IT services sector. Together, they are ending the era of IT-led job creation and with it, the economic model that underpinned India’s middle-class expansion.

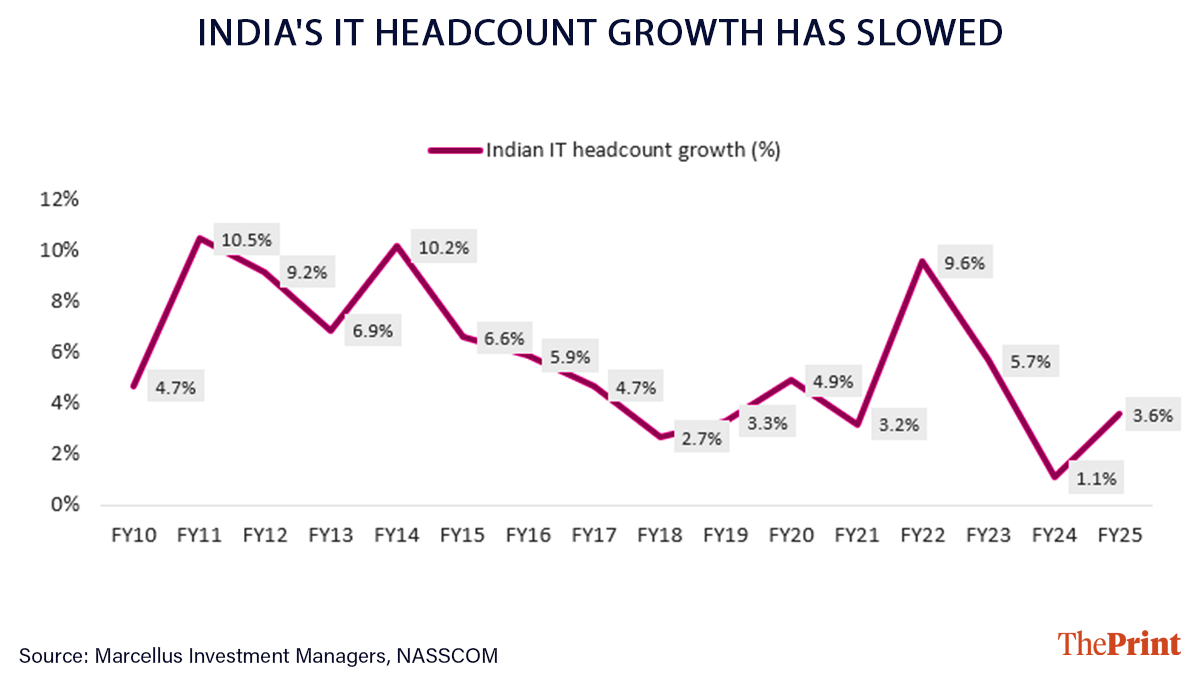

The maturing of the IT services sector: With eight million employees, India’s IT services sector remains the country’s largest formal employer. But growth has decisively decelerated. In the post-COVID era, as Fortune 500 companies—the largest clients of Indian IT firms—accelerated their own technology adoption, the need for incremental outsourcing slowed sharply. Revenue growth for the four largest IT services firms dropped to a CAGR of just 6.8 percent in the five years ending FY2025, roughly half the historical rate. Proportionately, employment growth slowed: the sector now absorbs fewer than 0.5 million new recruits per annum, down from over a million.

As Vishnu Gopal, Marcellus’s technology analyst, explains, global outsourcing penetration was in the mid-single digits in the early 2000s and has since risen to approximately 30 percent. That headroom is now largely exhausted. Clients in developed markets are also diversifying their vendor base across geographies to manage geopolitical risk, which further limits the market share gains historically available to Indian IT players. As the graph below illustrates, the downward trend in IT headcount growth is unmistakable and structural.

AI replacing humans in routine cognitive tasks: Artificial intelligence is substituting human labour at an accelerating pace across both blue-collar and white-collar roles. In the blue-collar world, India’s 12 million security guards—one of the largest employment categories in the country after construction—now face displacement by cameras, sensors, and automated systems. In the white-collar world, IT services companies are cutting thousands of jobs as AI handles coding, quality assurance, customer support, and back-office operations.

Major firms, including TCS and HCL Tech, have announced significant workforce reductions. A Niti Aayog study projects 2 million job losses in the IT and customer experience sectors by 2031. The asymmetry here is stark: Western countries facing labour shortages benefit from automation. India—with a median age of just 29 and millions of young workers seeking employment—confronts the opposite problem. For a nation already struggling to generate sufficient jobs, AI’s substitution effect threatens to eliminate white-collar employment options before the complementarity effects—where technology makes remaining workers more productive—can materialise. India’s white-collar job creation engine has, in effect, comprehensively jammed.

If IT services—the sector that finances India’s current account, employs its graduates, and powers the aspirations of its middle class—enters a prolonged period of stagnation, the resulting questions are consequential: What happens to the Indian economy’s growth drivers? What fills the foreign exchange gap? And critically, are there sectors where this disruption creates genuine new opportunities for the country?

Costs are immediate; opportunity is real but delayed

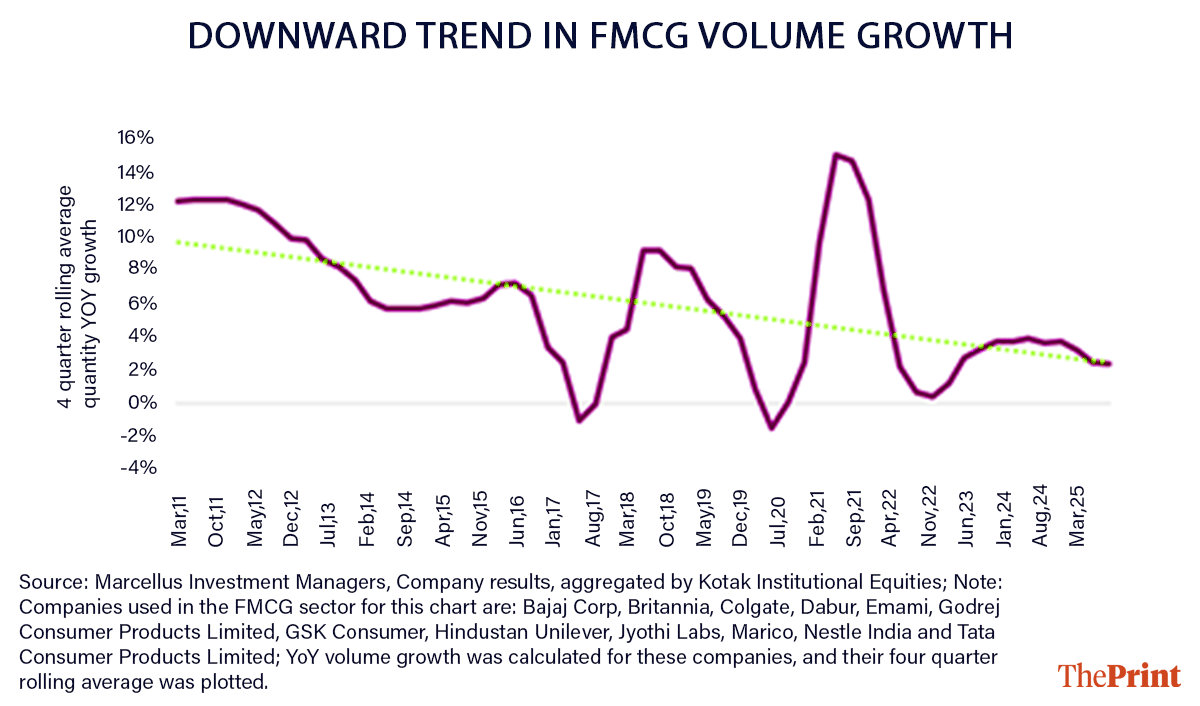

Consumption growth slows: The most immediate consequence is a structural deceleration in domestic consumption. India’s middle class—a cohort of urban, educated professionals that sits squarely in the middle of the income distribution—was the primary beneficiary of three decades of IT services expansion. This class precisely drives the bulk of discretionary spending in the country. The evidence is already visible.

As the graph below shows, FMCG volume growth—a broad proxy for consumption across India—has trended steadily downward over the past 14 years. The time series charts for consumer durables and cars look almost identical to the FMCG chart shown below. It is believed that this trajectory will worsen as the combined effects of sector maturation and AI-led displacement ripple through this class’s incomes and expectations. Residential real estate markets in Bangalore, Hyderabad, and Pune—cities that rose on the back of the IT services boom—are also beginning to see moderation.

Sustained pressure on the Indian Rupee: India’s development path was unusual. The country leapfrogged a large manufacturing phase and moved directly to a services-led growth model. IT services, in particular, generated foreign exchange surpluses that kept the current account deficit in check and the rupee relatively stable. As that engine decelerates—with no immediate alternative source of dollar inflows at scale—the rupee faces structural downward pressure.

India’s RBI forex reserves are already declining by roughly $10 billion per month (stripping out the mark-to-market impact of rising gold prices). The RBI cannot absorb the shortfall from falling IT services exports indefinitely; at some point, it is more likely to let the currency find a new equilibrium. Adding to this pressure, the Trump administration’s

“expectation” that India purchase $100 billion in American goods will place further

exogenous strain on the rupee. A weaker INR is not simply a macroeconomic data point; it has real consequences for import costs, inflation, and the purchasing power of middle-class households.

We have used only a few sectors where we are likely to benefit the most. And therefore, we have only considered those sectors’ market sizes in the US and EU.

Asymmetry between winners & losers is here to stay

A critical asymmetry exists in this transition that must be understood. The beneficiaries of India’s coming boom in manufactured exports will be manufacturers in industrial towns: Coimbatore, Hosur, Chennai, Hyderabad, Vizag, Pune, Surat, Baroda, and Ludhiana. They will be real, and their prosperity will be significant.

The casualties of slower IT services growth will be millions of employees living in

condominiums in Hyderabad, Bangalore, Pune, Gurgaon, and Mohali—people whose

careers, mortgages, and identities were built around the assumption of the continued IT sector growth. This mismatch between the scale of winners and losers in this economic ‘Sagar Manthan’ will weigh on property prices and on the lives of tens of millions of families.

The pain that the losers will feel is already upon us. The prosperity that the winners will see is still several years away—most likely arriving between 2027 and 2037. Overall, the Indian economy faces a few genuinely difficult years as it navigates an epic inflection point in its post-liberalisation history.

Investment implications

This inflection point demands individual-level action. There are three things that can be

done to navigate the turbulence ahead. First, retrain for the era of white-collar gig jobs

that is upon us. Structured, long-term corporate employment will diminish gradually—especially for younger people in the IT and ITES sector—as AI does more of the repetitive tasks that white-collar workers like coders and equity analysts are accustomed to.

Second, while entering an era of white-collar gig jobs, the volatility of personal incomes will increase. Therefore, maintaining a substantial financial buffer to help through the difficult years is key. Third, as the broader economic climate becomes more volatile in this Trumpian age, planning financial futures assumes significance, especially since employers would not be around to inject structure and stability.

Nandita Rajhansa and Saurabh Mukherjea work for Marcellus Investment Managers (www.marcellus.in), a SEBI-registered portfolio management service provider. Nandita and Saurabh, along with Sapana Bhavsar, are authors of ‘Breakpoint: The Crisis of the Middle Class and the Future of Work’ which will be published later this month.

This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice.

Note: The above material is neither investment research, nor investment advice. Tata

Consumer Products Limited forms part of Marcellus’ Portfolios. We as Marcellus, our

immediate relatives and our clients may have interest and stakes in the mentioned stocks.

The stocks mentioned are for educational purposes only and not recommendatory. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”)

registered Investment Advisor. No content of this publication including the performance

related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such

jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of

this material must before dealing and or transacting in any of the products and services

referred to in this material must make their own investigation, seek appropriate

professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by

anyone other than the addressee is unauthorized. If you are not the intended recipient,

please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any

impression or a claim that these products/strategies achieve the respective objectives.

Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer, or an employee. This

material may contain confidential or proprietary information and user shall take prior

written consent from Marcellus before any reproduction in any form.

(Edited by Madhurita Goswami)

Also Read: IT sector as India’s ‘growth engine’: Budget boosts tax certainty with safe harbour revisions