Punjab National’s butter chicken is truly cooked, as the RBI continues to force all lenders to flush out dud loans.

Other than the embarrassment of asking the country’s second-largest state-run lender to, well, stop lending, there’s no other reason why India should allow Punjab National Bank to advance even one rupee to anybody except the government.

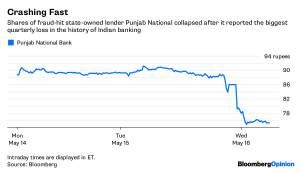

The financial institution, at the epicenter of a massive fraud allegedly committed by uncle-nephew jeweler duo Mehul Choksi and Nirav Modi, on Tuesday reported a $2 billion loss, the biggest in the history of Indian banking.

A 14 percent drop in the bank’s shares Wednesday morning suggests investors expect worse to come.

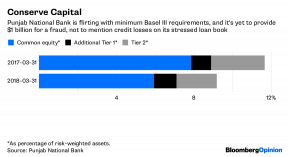

Punjab National has so far made a provision for only half the hit it has taken in the so-called letter-of-undertaking scam. Once you account for the remaining $1 billion, the bank’s capital would fall way below the minimum 9 percent of risk-weighted assets required under Basel III norms. (That’s assuming there won’t be any profit in the coming quarters to soften the blow.)

Punjab National’s butter chicken is truly cooked. For one, the hemorrhaging will continue as the Reserve Bank of India forces all lenders to flush out dud loans. More than 18 percent of the bank’s assets are nonperforming.

Besides, there’s no chance of an equity infusion, except from taxpayers who forked out $800 million in March. Punjab National did raise $750 million from institutional investors in December, but that was before the fact it had been merrily handing out promises to pay other lenders on behalf of the uncle-nephew duo came to light.

The pair have since left India. As for the broken bank they left behind, all that remains is for the RBI to take it under Prompt Corrective Action. As many as 11 of India’s 21 state-run banks are already inmates of that sanitarium. Dena Bank’s shares crashed to a 15-year low after the RBI told it to stop lending altogether. Allahabad Bank has also been saddled with restrictions on advances. Should Punjab National be hit with similar curbs, it might mean – among other things – an early recall of the $800 million in additional Tier 1 bail-in bonds the bank has issued. That would make a bigger hole in its tattered capital cushion.

It’s hard to see how the floundering enterprise can get steadied. Forcing Punjab National to lend only to the government until it gets better may be part of the solution. Granted, it already has $11.5 billion of government bonds in its available-for-sale portfolio, and in an environment of rising interest rates, mark-to-market losses on these investments are starting to bite.

However, being a state-run bank means Punjab National’s $39 billion deposit franchise in current and savings accounts is intact. These deposits, which cost 4.8 percent in the March quarter, yielded 7.3 percent when invested – but only 6.5 percent when lent out. So Punjab National should look to expand its $30 billion investment book, the bulk of which comprises government bonds, while it waits for its $64 billion loan book to stop bleeding.

The lender, which claims to be “the name you can bank upon,” has done enough banking for now. It should take a rest. – Bloomberg