There are moments when financial markets perceive shifts in global dynamics well before they are acknowledged by policymakers. We are currently living through one such phenomenon. Interest rates across developed economies, particularly long-term government bond yields, which indicate the cost of borrowing over a decade or more, are exhibiting behaviour similar to wartime-like conditions: stubbornly high, resistant to reduction, and grounded in caution.

A simple explanation would be to blame this to the recent escalation in West Asia. However, that would be incorrect. The persistence of high interest rates did not originate with recent tensions; rather, it commenced earlier, around 2023, when markets quietly concluded that global instability had transitioned from being episodic to structural.

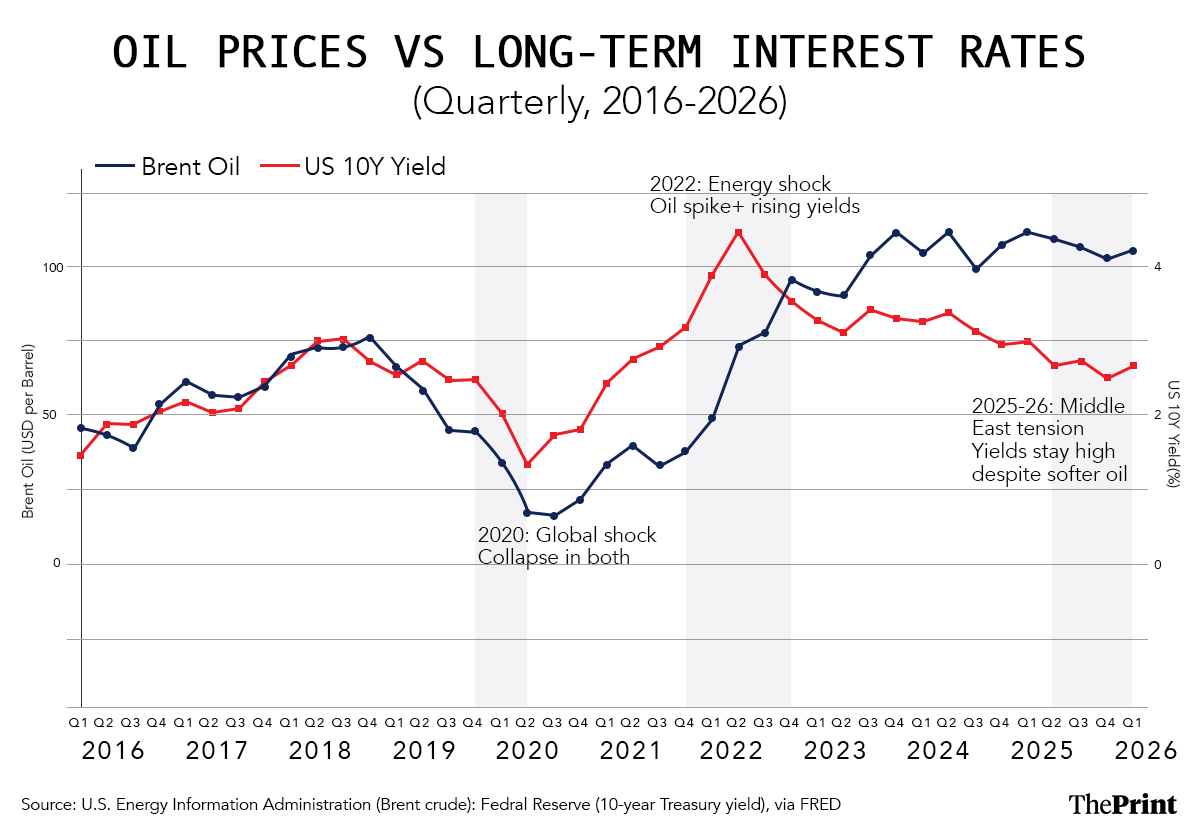

Over the past decade, the correlation between oil prices and long-term interest rates followed a familiar, well-established pattern. As energy prices increased, inflation followed, prompting central banks to implement tighter monetary policies. On the other hand, when energy prices declined, inflation subsided, leading to more accommodative policies. This cyclical pattern persisted through the pandemic-induced economic shock of 2020 and the energy price surge of 2022. However, beginning in 2023, something more significant emerges. Despite the stabilisation and marginal decline of oil prices, interest rates remain elevated. The expected transmission from reduced energy prices to decreased inflation and, subsequently, lower interest rates weakened.

This is exactly where the story changes, and it changes well before the onset of recent geopolitical tensions.

The shift that began in 2023

In 2023, a significant transformation occurred in how markets interpret global dynamics. Initially, inflation stopped behaving as a temporary anomaly. The prevailing “transitory” narrative gave way to a more disconcerting reality: inflation had become sticky, influenced not only by demand but also supply constraints and geopolitical factors. Energy markets evolved from being merely volatile to becoming strategic in nature. Similarly, supply chains were no longer simply inefficient; they were being actively restructured along geopolitical lines.

Furthermore, the nature of economic shocks underwent a transformation. Previously, disruptions whether in oil or trade were expected to be reversible. By 2023, markets began to regard these disruptions as persistent. The conflict in Ukraine, the fragmentation of global trade, and the emergence of industrial policies across major economies indicated that the global system itself was undergoing a fundamental reconfiguration. At the same time, costs were not expected to revert to previous levels; instead, they were expected to remain structurally higher.

Critically, this shift manifested in financial markets through a concept known as term premium, which refers to the additional compensation investors require for holding long-term debt. Throughout much of the 2010s, this premium had been suppressed by quantitative easing and a stable global environment. However, from 2023 onward, it began to rise, reflecting uncertainties surrounding inflation, policy credibility, and geopolitical risks.

Simultaneously, inflation expectations became less firmly anchored. When inflation is perceived as temporary, households, firms, and markets anticipate a swift reversion, allowing central banks to ease monetary policy. However, when inflation is perceived as being shaped by recurring supply disruptions, such as energy shocks, trade fragmentation, and climate-linked volatility, expectations begin to adjust. Inflation is no longer viewed as a one-off deviation; it becomes a recurring risk. As a result, long-term interest rates, which incorporate these expectations, respond accordingly.

The outcome was a subtle yet decisive change: long-term interest rates were no longer anchored solely in expected policy rates or growth prospects. Instead, they became increasingly anchored in uncertainties, pertaining to inflation, supply, and the geopolitical environment itself.

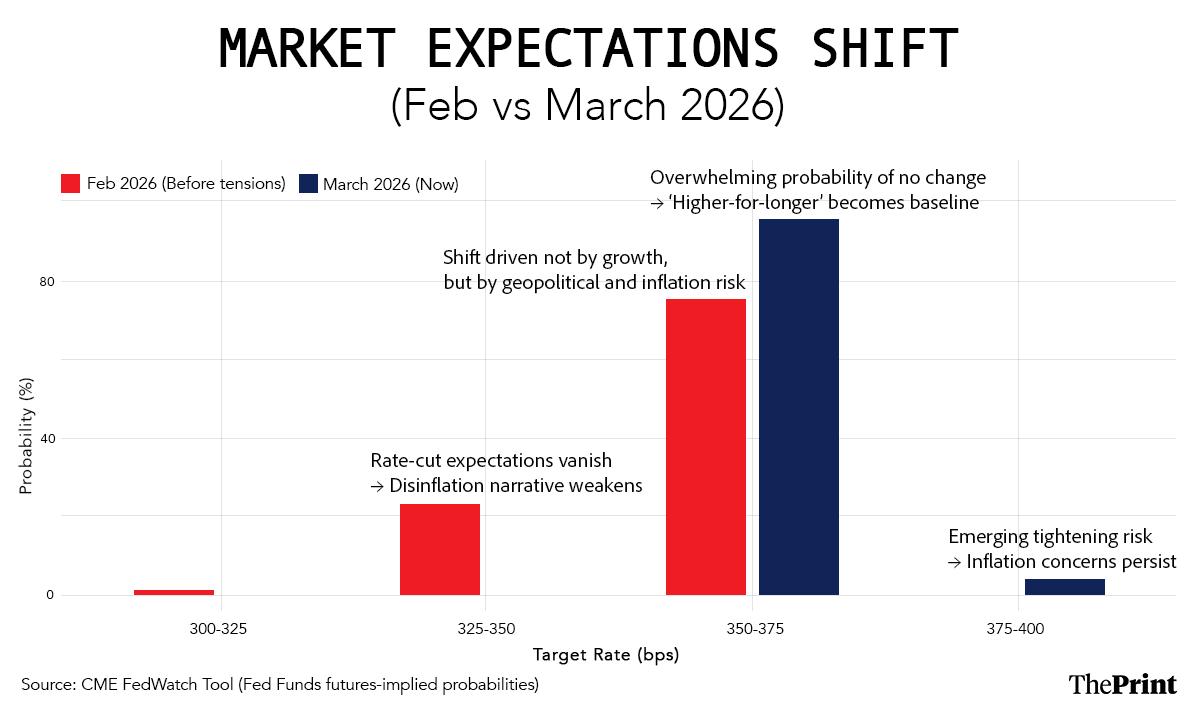

If the first chart captures the occurrence of a structural break, the second chart demonstrates the extent to which this has been established. The shift in market expectations between February and March 2026 indicates a swift consolidation around the notion of “higher for longer”. Anticipated rate cuts have been excluded from pricing, and the potential for further tightening has re-emerged within the distribution.

Notably, this shift occurs without a corresponding increase in economic growth. It is not economic strength that is keeping rates high, but rather the persistence of risk.

Recent tensions in West Asia do not instigate this dynamic; instead, they reinforce it. Markets had already adapted to a context where inflation could resurface, supply could be disrupted, and stability could not be assumed. New shocks simply validate this prior assessment.

Monetary policy as a substitute for strategy

In previous eras, a prolonged increase in geopolitical and supply-side risks would have been met with a coordinated fiscal response. Governments would have significantly increased spending on defence, energy security, and industrial capacity. Monetary policy would have operated alongside this expansion.

This is not the current scenario.

While fiscal responses have been implemented, they are fragmented and limited, lacking the scale and coordination characteristic of historical wartime budgets. Nevertheless, the economic environment increasingly mirrors one influenced by such risks. As a result, the burden of adjustment has disproportionately fallen on monetary policy. This situation represents wartime finance without the corresponding war budgets.

Interest rates are maintained at high levels not solely to confront current inflation but to also prevent its recurrence. They reflect not overheated demand but the possibility of renewed disruptions. In doing so, they directly transmit the cost of uncertainty to the private sector through increased borrowing costs, deferred investment, and tighter financial conditions. Central banks are, in essence, pricing a world that fiscal policy has not fully addressed.

Also read: How West Asia crisis can play out for PM Modi and BJP in Assembly polls

A policy response that must catch up

For economies such as India, this transition holds significant implications. Global financial conditions are expected to remain stringent for an extended period, irrespective of domestic growth dynamics. Capital flows will be influenced less by relative performance and more by global risk sentiment. The cost of capital will incorporate not only macroeconomic fundamentals but also geopolitical uncertainties originating from external sources.

More fundamentally, this represents a shift from a business cycle to what may be termed as a risk cycle. In this context, policy cannot be limited to managing inflation and growth in isolation. It must directly address the sources of structural uncertainty, including energy security, supply chain resilience, and the fiscal capacity to absorb shocks.

As previous analyses of inflation dynamics in emerging economies have demonstrated, including my own work on the impact of supply shocks on inflation expectations, price pressures are often driven as much by disruptions as by demand conditions. When such disruptions become persistent, managing inflation expectations becomes as crucial as managing inflation itself.

There is a temptation to misinterpret high interest rates as a sign of resilience. However, they are not; they are a signal of caution. Markets lack sufficient confidence to anticipate relief because they remain unconvinced that the shocks of recent years have been resolved.

The world did not suddenly become unstable in 2026; markets had already reached this conclusion by 2023. Policy must now align with this reality. Until it does, through credible, coordinated responses that address the roots of uncertainty rather than merely its symptoms, interest rates will remain where they are: elevated, unyielding, and quietly signalling that the global economy is still bracing for what comes next.

Bidisha Bhattacharya is Consulting Editor (Economy) at ThePrint. She tweets @Bidishabh. Views are personal.