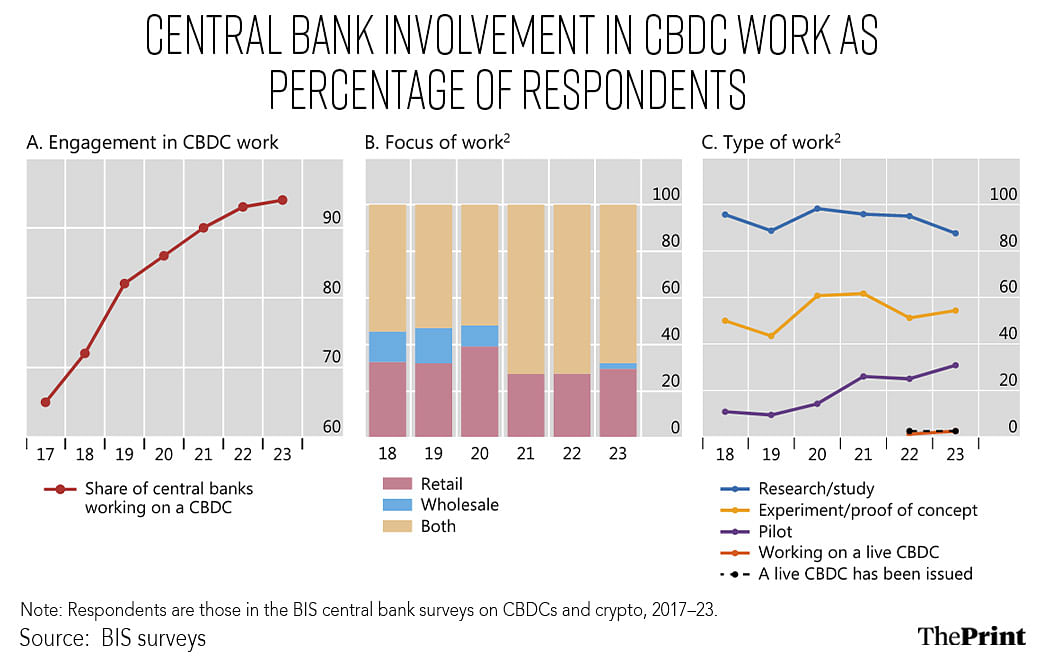

Over the course of 2023, there has been a sharp uptick in the number of central banks exploring a Central Bank Digital Currency (CBDC). A survey conducted by the Bank for International Settlements (BIS) in 2023 shows that 94 percent of the participating central banks are engaged in CBDCs. Central banks globally have adopted different approaches and are advancing their engagements with CBDCs at varying speeds.

The advanced economies central banks seem more inclined towards exploring the use cases of the wholesale version of a CBDC. Jurisdictions are motivated to enhance cross-border payments through wholesale CBDCs, ideally addressing prevalent challenges such as high costs, low speed, limited access and insufficient transparency.

On retail CBDCs, the survey shows that central banks are studying the implications for monetary policy and the role of banks.

A key finding of the survey is that central banks seem in no hurry to roll out the digital version of their national currency. As compared to last year, they seem more likely to issue a CBDC in the medium term than in the short-term, indicating an increased degree of uncertainty on the issuance of CBDCs. Overall, central banks are more likely to issue a wholesale CBDC within the next six years in comparison to a retail CBDC.

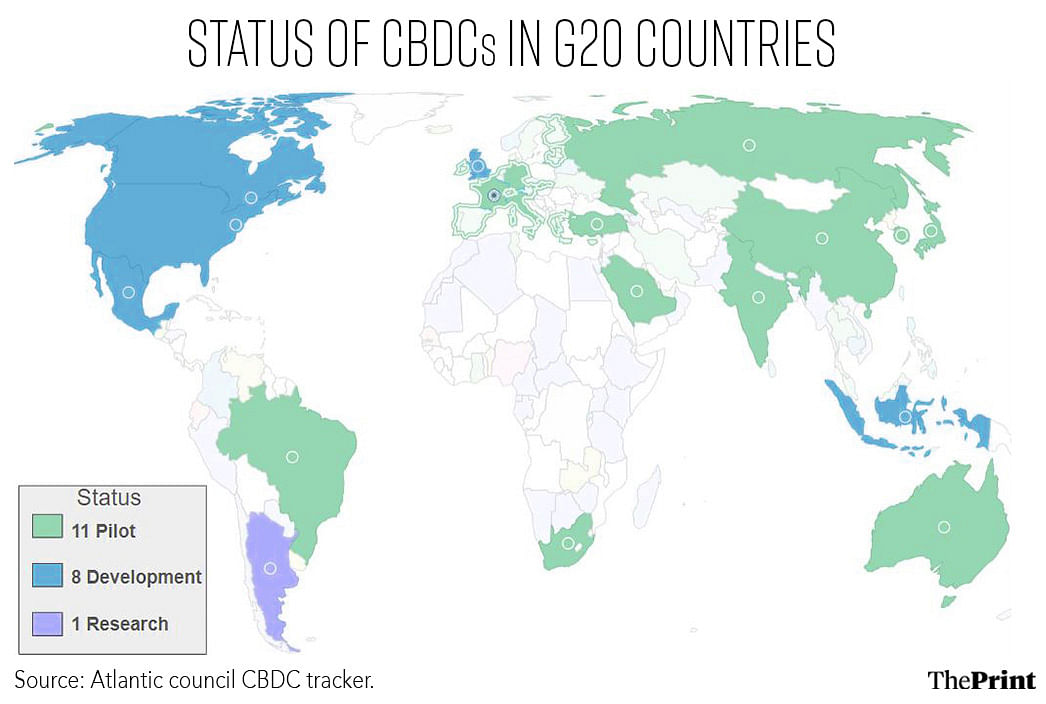

India is one of the 11 G20 countries and 36 countries in the world that have started CBDC pilots, as of May 2024. Both wholesale and retail digital Rupee (e-Rupee) pilots were kicked off in 2022.

About 50 lakh users and 4.2 lakh merchants were participating in the retail CBDC pilot as of June 2024. The transactions of retail CBDC through interoperability with UPI reached a high of one million per day on 27 December, 2023. However, the RBI has noted that the preference for UPI among retail users still persists.

Interest and non-interest bearing CBDCs

A key question in the context of the design feature that central banks are exploring is whether CBDC should be remunerative, i.e. whether the digital currency should bear interest or not. An argument in favour of interest bearing CBDCs is that it enhances the transmission of monetary policy i.e. changes in policy rate get passed on quickly.

The argument against having an interest-bearing CBDC is that banks could face a withdrawal of deposits, should people choose to hold interest-bearing CBDCs in greater volume.

Banks would have to raise alternative sources of funding or offer higher interest rates on deposits to retain customers. In both cases, banks would be faced with a compression of their margins. While India will be offering a non-interest bearing CBDC, akin to cash, central banks globally seem to be divided on this feature.

Bank of Israel, for example, has announced that its retail CBDC will be interest-bearing. This, according to the Bank, will nudge banks to pass on higher interest rates to depositors and spur competition in the financial system.

CBDCs as an alternative to cryptoassets and stablecoins

The BIS survey shows that an increasing number of central banks have accelerated their work on CBDCs in response to developments in stablecoins and other cryptoassets. In recent years, stablecoins are increasingly being used for remitting payments. For instance, USDC, a stablecoin that is redeemable 1:1 for dollar, is being used for sending remittances by immigrants in the US to Latin American countries.

Financial technology companies are leveraging blockchain technologies and partnering with crypto exchanges to ensure low-cost transfer of funds.

Many central banks are studying the uses of stablecoins and cryptoassets to motivate the use cases and design choices of CBDCs. In parallel, the BIS Survey shows that 60 percent of the jurisdictions are developing a regulatory framework for stablecoins and cryptoassets. The work on developing regulatory frameworks may be in response to the growing recognition that banning cryptoassets may be a sub-optimal outcome.

In the UK, the Financial Services and Markets Act (FSMA) was amended to bring cryptoassets into the realm of financial regulation. Regulations governing fiat backed stablecoins are expected to be implemented in a phased manner. The regulations governing payments would be amended to capture stablecoins as means of payment. Regulations would cover requirements for backing assets and redemption, conduct of business, and prudential requirements, among others.

In the EU, Markets in Crypto-Assets Regulations (MiCA) have kicked in from 30 June, 2024. The regulations aim to bring the issuers and service providers of cryptoassets within the legal and regulatory framework. Among the emerging and developing economies, Turkey has recently approved legislation for oversight on the crypto market. The legislation aims to introduce a licensing scheme for crypto firms.

Challenges in regulating crypto and need for cross-border cooperation.

The regulatory landscape for crypto is still evolving. A key challenge in regulating crypto is the lack of consensus on definitions, taxonomies and classification of cryptoassets. Jurisdictions may term a cryptoasset as a ‘virtual asset’, a ‘virtual digital asset’, a ‘crypto token’, ‘virtual currency’ or ‘cryptocurrency’ — each incurring a different definition.

Regulators within a country may also assess a cryptoasset differently based on the nature of an asset, the services provided, associated design, etc. For instance, the USA’s Securities and Exchange Commission (SEC) treats cryptocurrencies as securities while the Commodity Futures Trading Commission (CFTC) treats cryptocurrencies as commodities. Currently, both, the CFTC and SEC, are trying to assert their jurisdiction over the crypto/digital/virtual asset space, while continuing to pursue oversight enforcement actions as and when deemed fit in the backdrop of an evolving landscape.

Moreover, the regulatory approaches adopted across jurisdiction can vary widely. Some countries may impose stricter crypto regulations in comparison to others. The borderless nature of cryptoassets and the fragmentation in the regulatory treatment within and across jurisdictions can increase the risks arising from regulatory arbitrage.

Therefore, international standard setting bodies have underscored the need for extensive cross-border cooperation, a global approach to regulating crypto, and timely implementation of international standards/recommendations.

The security breach of the Indian crypto-exchange and trading platform WazirX on 19 July, resulting in a loss of USD 230 million worth cryptoassets, further suggests the need for robust regulation in the crypto ecosystem. Preliminarily, the platform has proposed a ‘55/45’ compensation plan, wherein the consumers absorb 45 percent of their losses. While further developments on this matter are awaited, such an approach compels further clarity on aspects of swift recovery, resolution and consumer protection in the crypto ecosystem at large. In this context, the government’s decision to come up with a discussion paper seeking comments on the remit of regulations on cryptocurrencies is a welcome development.

Radhika Pandey is associate professor and Anandita Gupta is a research fellow at the National Institute of Public Finance and Policy (NIPFP).

Views are personal.

Also read: In tradeoff between fiscal prudence & boosting economy, budget should focus more on demand & jobs