New Delhi: India’s middle class is grappling with simultaneous crises of jobs, wages and debt. Yet many of its most cherished assumptions about getting ahead—rote learning to crack competitive exams, logging long hours in pursuit of promotions, acquiring the visible tokens of corporate success (corner office, large car, weighty job title)—are precisely the beliefs least suited to the country’s emerging era of entrepreneurship and disruption.

Five of these beliefs are directly contradicted by India’s economic data.

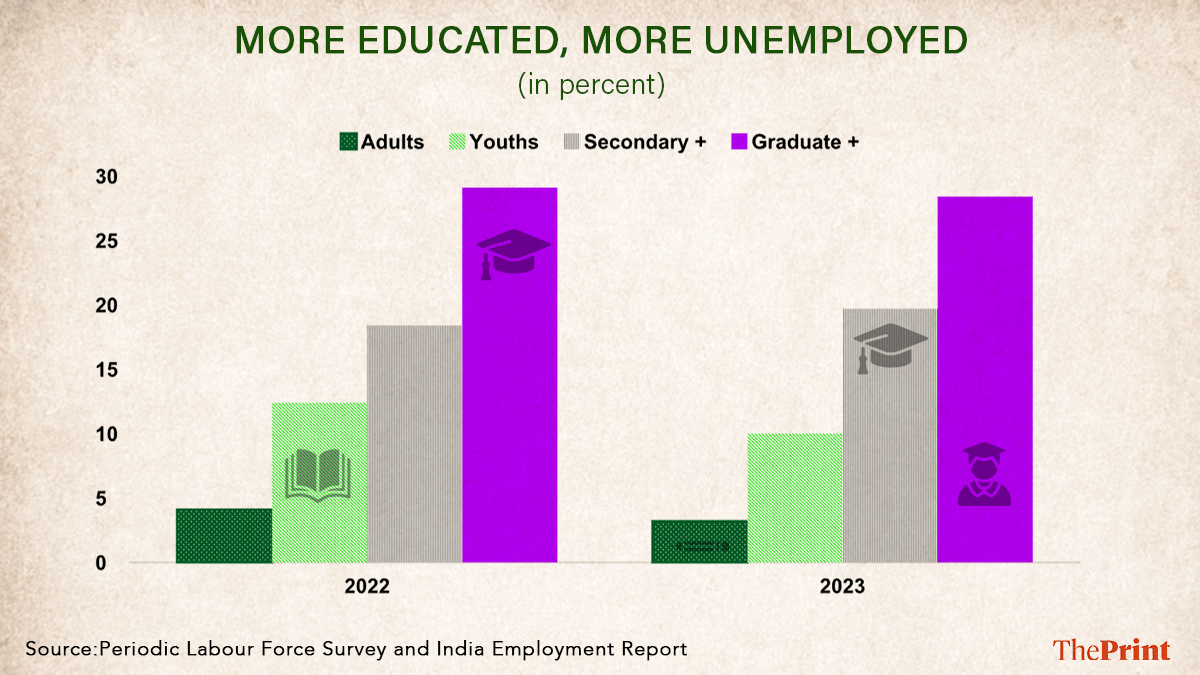

Belief #1: University education is essential

The middle class has long defined itself by its faith in education—the conviction that a university degree is the gateway to prosperity. Pent-up family ambition constructs a mirage of employment and success that is disconnected from the reality of available jobs and necessary skills.

Data tells a different story; that acquiring a degree reduces both earnings and employment prospects. The unemployment rate for graduates stands at 29.1 percent—nine times higher than for illiterate people.

The crisis is visible even at the country’s apex institutions. Minimum placement salaries at IIT-Bombay fell from Rs 6 lakh per annum in 2023 to Rs 4 lakh p.a. in 2024. Roughly 8,000 of 21,500 IIT graduates nationwide were unemployed in 2024.

The Parliamentary Standing Committee on Education’s March 2025 report also cited an “unusual decline in placements in IITs and IIITs between 2021–22 and 2023–24”.

A TeamLease survey from October 2024 estimated that only 10 percent of engineering graduates would find employment that year; a March 2025 survey put the figure more bleakly still, finding 83 percent of engineering graduates without work.

None of this is an argument against education itself. The goal is not to discourage learning, but to spark an honest conversation about how we educate—and for what. There is a need to shift focus toward quality over credentialing, to align curricula with the skills the economy actually demands, and to invest in upskilling that translate qualifications into genuine opportunities.

Also Read: India’s IT-led growth is slowing – can manufacturing become the next engine?

Belief #2: In a private sector job, income rises over time

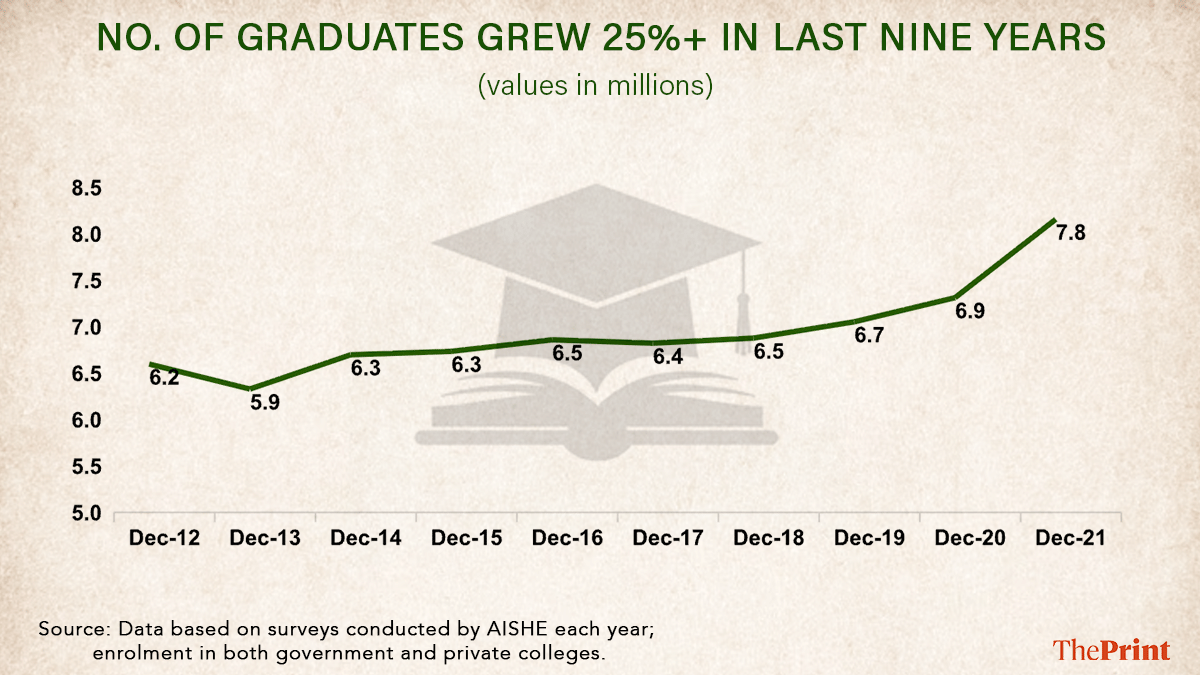

India has spent decades producing more graduates each year, driven by a younger demographic. A record 1.2 million students sat the IIT entrance examinations in January 2024 alone. Going by the All India Survey on Higher Education (AISHE), an exhaustive source of data for higher education in India, over eight million students graduates every year.

The resulting graduate pool is burgeoning. But the problem is not only supply—it is quality. Efforts to democratise access to higher education have expanded enrolment while depressing graduate quality, creating a labour market stuck in an adverse equilibrium: abundant supply of low-skilled graduates pushes wages down, while genuinely skilled talent remains scarce.

That wage compression is not confined to the margins of the economy. Even among employees of India’s Nifty50—the country’s largest and most profitable companies—real wages have declined.

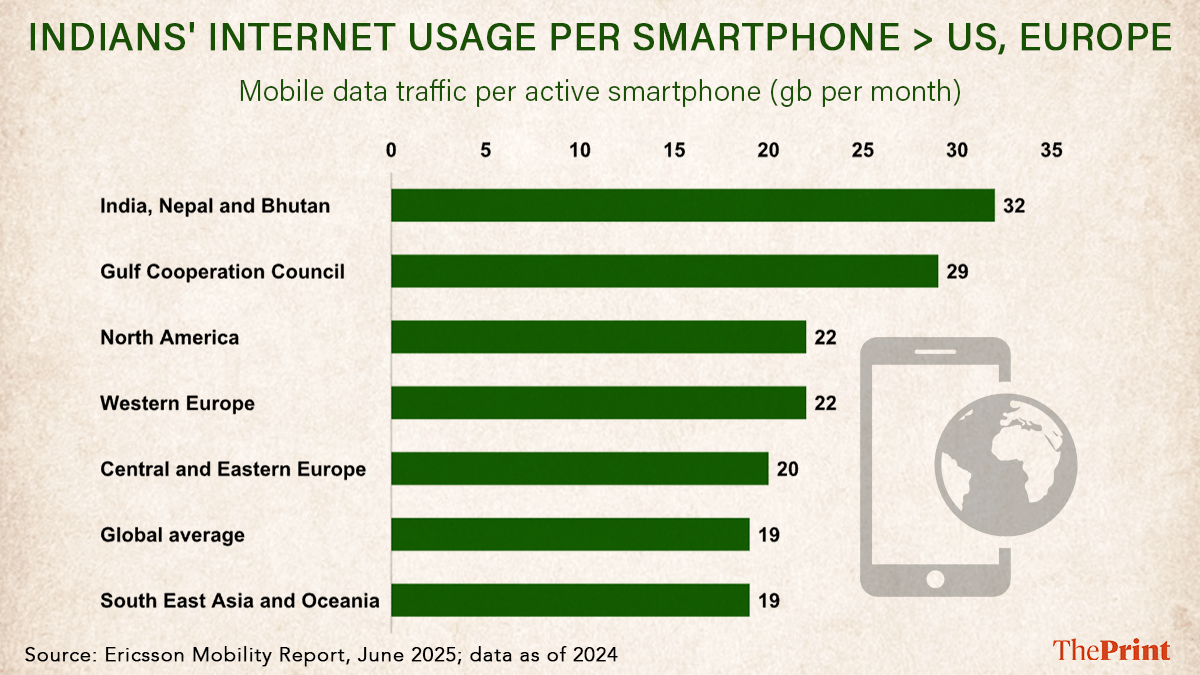

Belief #3: Smartphone and internet data are essential

When Jio launched in 2016 and made mobile data effectively free, millions of young Indians gained unlimited internet access within months. What followed was not merely a technological revolution. It was a psychological and financial catastrophe.

Cheap smartphones, near-free data and social media created a perfect storm. A generation unable to secure graduate employment despite their degrees now spends hours daily scrolling through curated images of wealth and success they cannot attain. The psychological toll is measurable: anxiety and depression medications are growing at twice the rate of other pharmaceutical categories.

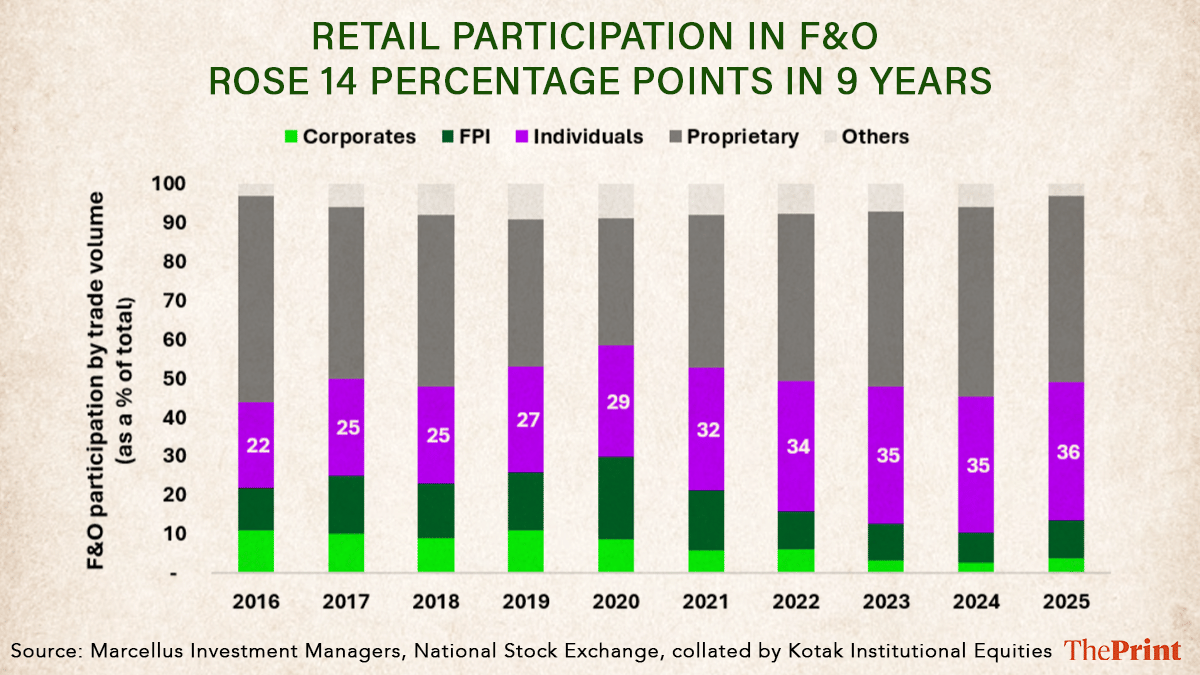

The financial damage is equally stark. Egged on by influencers promising easy money, nine million Indians—mostly young men—have poured into futures and options (F&O) trading. Over three years, they collectively lost Rs 3 lakh crore to institutional investors and brokers.

Meanwhile, the same AI tools that glamourise trading on social media are eliminating the very jobs these traders need to fund their losses. From call centres to coding, automation is gutting white-collar employment even as eight million new graduates enter the labour market every year.

Belief #4: Promotions are career milestones

In corporate life, advancement comes from meeting targets, avoiding surprises and keeping the machine running. Thinking and doing are separated by layers of hierarchy. When a crisis hits, one looks upward for strategy.

Entrepreneurs have no such fallback. They must conceive the plan, revise it constantly and execute it personally. As Infosys co-founder Nandan Nilekani described it, the entrepreneur is simultaneously thinker and doer, toggling between the two without pause. Crises are not exceptional events; they arrive annually, sometimes monthly.

The contrast in personal development is equally sharp. Large organisations reward the outer scorecard—titles, ratings, visible symbols of upward mobility—because committees determine promotions. Conformity is safe; unconventional risk is not.

If India’s job creation is to come from thousands of small firms rather than a handful of industrial giants, the workforce’s mindset must shift. The old model of lifetime employment—joining a bank as a probationary officer and retiring as a deputy managing director—is fading. The entrepreneurial mindset is becoming not the exception but the norm.

Belief #5: Working long hours to impress the boss is important

What will matter most in India’s emerging entrepreneurial economy is not performative signalling—the kind that often pays dividends in large companies—but the ability to cope and think on one’s feet.

Nor is it only the ‘mandatory hours’ mindset that must change. Entrepreneurship is guided by the inner scorecard. Investor Warren Buffett speaks of the quiet accumulation of capability, curiosity and judgement. Godrej Consumer chief executive Sudhir Sitapati—author of The CEO Factory—describes how insights are formed: by observing constantly, reading widely and making lateral connections. These are instincts that India’s most enduring business builders reflect.

The Dhingra family of Berger Paints, for instance, built an exceptional company not by cultivating status but by staying grounded and strengthening the substance of their business year after year.

The sharpest divergence between the corporate and entrepreneurial mindsets lies in their relationship with risk. In a corporate setting, the safest course is often to fail conventionally rather than try something new and risk visible embarrassment; after all. committees are not built to reward brave failures. Entrepreneurs inhabit the opposite world. Every consequential decision is a risk; setbacks are constant. As Harsh Mariwala, founder of Fortune 500 company Marico, had said: “Sometimes you win, sometimes you learn.” For a founder, failure is not reputational damage; it is part of the apprenticeship.

Taken together, these differences point to a new entrepreneurial mindset that India must cultivate: improvisational, internally driven, comfortable with risk, frugal, and oriented towards building something that lasts. It is a shift from asking ‘what is expected of me?’ to ‘what can I build here?’, and from a three-year performance cycle to thinking across decades.

Saurabh Mukherjea, Nandita Rajhansa and Sapana Bhavsar write about the jobs, wages and debt crisis facing the Indian middle class in this age of automation and AI in their new book ‘Breakpoint: The Crisis of the Middle Class and the Future of Work’, published by Juggernaut on 23 March 2026. Mukherjea and Rajhansa work for Marcellus Investment Managers, and Bhavsar is an HR professional with two decades of experience.

Also Read: Borrowing to survive: Indian households are saving more, why are they still in debt?

This article kind of collates together in a concise manner what I have been saying, in bits and pieces, about the education and job market all these years. Very succinctly put together!