Warning: This writer may, very soon, eat humble pie. Still, I believe we need a bit of nuance around the term “energy crisis.” Bottom line: We’re using it too loosely. The American attack on Iran is bad news for the global economy, but I don’t anticipate that it will spark a 2022-style inflation shock.

Looking at the energy market with a wide-angle lens, I don’t see anything remotely approaching the pain of 2021-22, when the energy crisis label was appropriate for Europe. There’s nothing matching the contours of the 1990-91 shock, let alone the 1973-74 and 1979 crises.

First, a bit of background. An energy crisis has three elements: the number of commodities affected; the magnitude of the price increase; and the duration of the increase. And there’s an additional element that we should always take into consideration when analyzing the energy market: the starting point, in terms of price, but also of the overall supply and demand balance.

Historical context matters, too. During the 1973-74 crisis, oil was the only game in town — even for generating electricity. At the time, petroleum accounted for nearly 25% of global power generation. Today, its share has dropped to less than 3%. For the average family in Europe, electricity and gas could be as important, if not more important, than oil. For many businesses, particularly in the services economy, oil is irrelevant — power is what matters. For China, the price of coal is typically key.

The energy market has changed over the last 50 years, but many still analyse it through paradigms that belong to another era. What made 2021-2022 truly a crisis is the fact that all major forms of 21st century energy — oil, gas, coal and electricity — became simultaneously expensive. The price increases were extreme, several magnitudes larger than what we have seen since the start of the Iran War. And the price pain was long-lasting, measured in quarters, rather than days.

Naturally, worst-case scenarios do happen. In fact, my worst-case for the impact of the Gulf conflict is significantly worse than most. I see scenarios that model oil rising just above $100 a barrel if everything goes wrong. If it does all go to hell, we should be so lucky.

Let me paint a possible — but improbable — nightmare scenario: The US miscalculates the tenacity of Iran and the Strait of Hormuz remains closed for three months; fighting for survival, Iran bombs key Saudi, Kuwaiti and Emirati oil facilities; those countries retaliate in turn, annihilating the Iranian petroleum industry. The world loses 20 million barrels a day for a quarter, and another 10 million for a year. If anyone thinks the market stops at $100 per barrel in such a scenario, I have an oilfield to sell to you.

Fortunately, we aren’t there, and I suspect we wouldn’t get there.

So what’s going on in reality? The Iran War affects a narrow set of energy commodities: oil and liquefied natural gas. It hasn’t spread to the electricity or coal markets; neither has it impacted the important, but isolated, US and Canadian natural gas market. The oil price surge is limited — just over 15%. As the war has just started, it is so far short-lived. The starting point was favorable: Prices were low, and both oil and LNG markets were facing a glut this year.

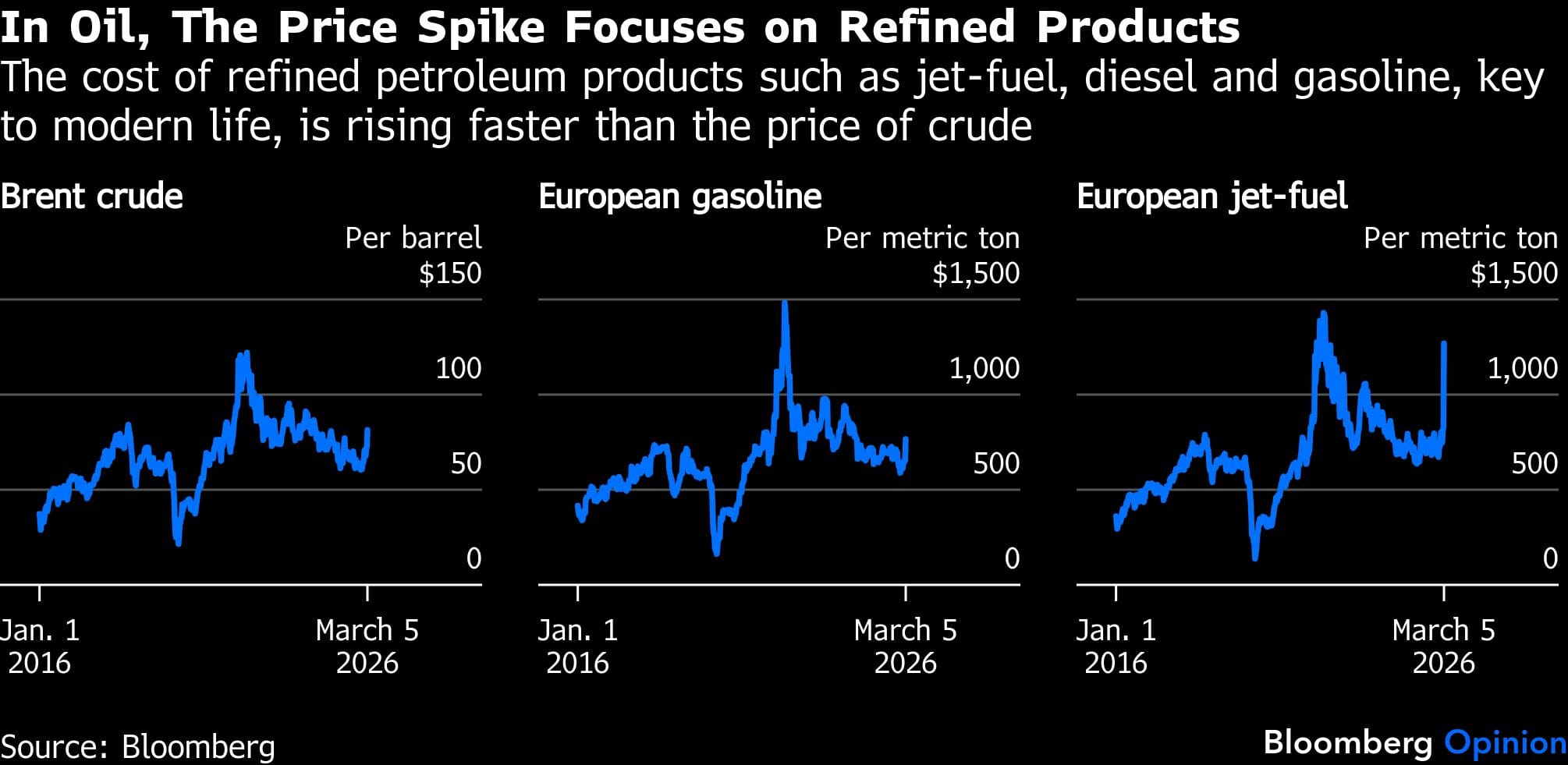

How do current oil and gas prices compare to previous crises? Pretty well, actually. Brent is hovering just above $80 a barrel. After Russia invaded Ukraine, it surged to more than $130 a barrel. Zoom out and current prices are within ranges that, in the past, had been considered normal, even, ahem, low! European gas is trading around €50 ($58) per megawatt hour; admittedly, that’s high, nearly double where it was a few days ago, but nowhere near the record high of €350 ($405) per MWh of 2022.

While I’m not worried about oil for now, refined petroleum products merit attention. Only oil refiners buy crude — and therefore, are exposed to its price, which so far hasn’t risen much. The rest of us — the real economy — purchase refined petroleum products like gasoline, diesel and jet-fuel. It’s those post-refinery prices that matter to us. Right now, they are rising much faster than the price of crude, particularly for diesel and jet-fuel. If there’s an energy crisis, it would be because of them.

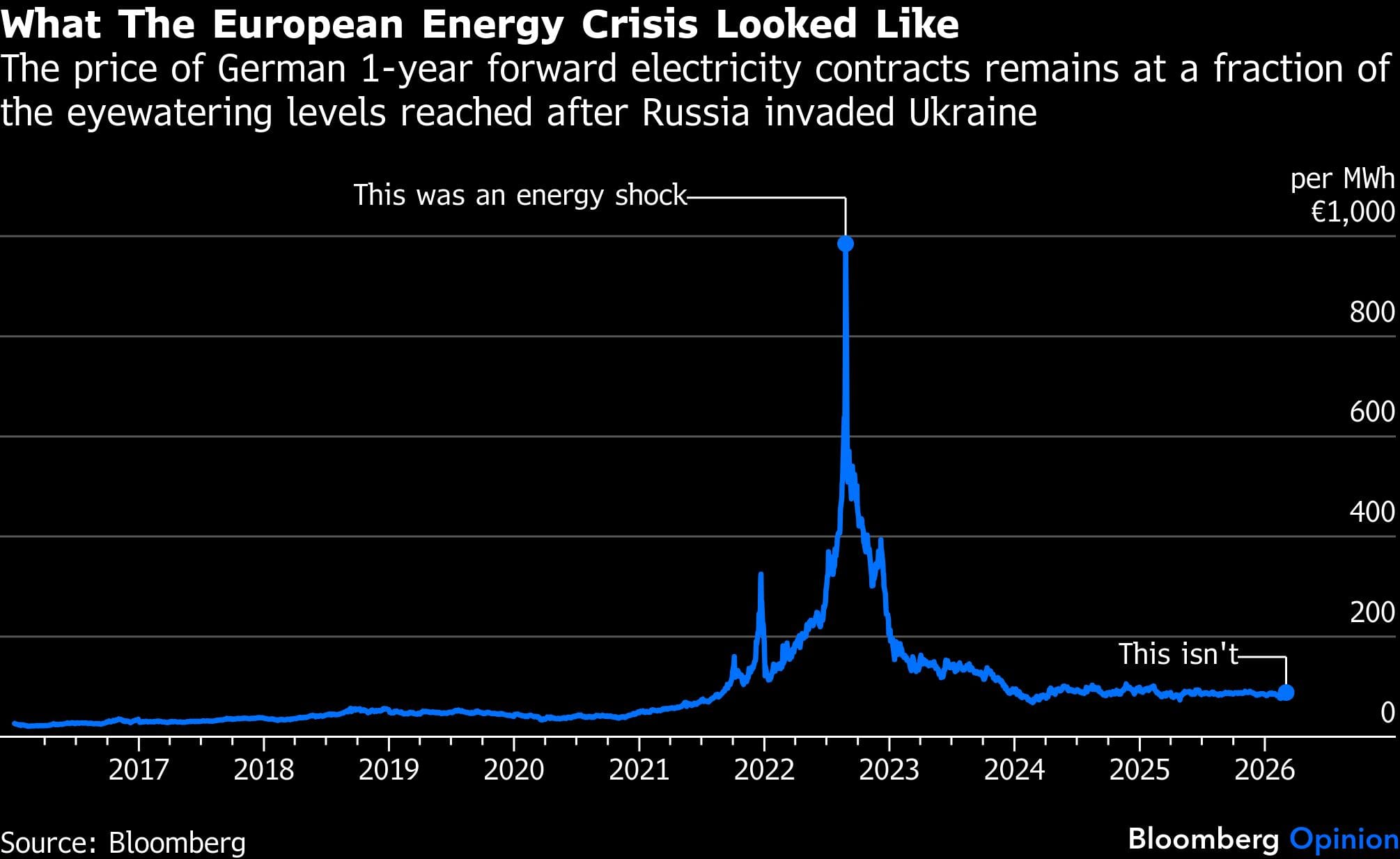

What about other energy commodities? Zip. Nada. Zero. OK, a tiny movement here and there. Let’s look at German wholesale electricity costs, using the one-year forward. The contract is a benchmark for the whole of Europe. It’s trading at €88 per MWh; in 2002, it touched €985 per MWh. Yes, you read that correctly: German electricity prices are 91% below their all-time high. By the way, they are also lower than four weeks ago.

Coal is similar. The commodity is forgotten in the West, but ask anyone in Asia — from India to Japan, let alone China — and it’s king. The Asian benchmark is changing hands at around $130 per metric ton; in 2022, it surged to $440 a ton. And what about American natural gas? It’s an embarrassment of riches. The benchmark Henry Hub contract trades under $3 per million British thermal unit. In 2008, during the commodity super-cycle, it touched $14 per mBtu. That’s energy dominance.

Energy crises go down in history by the name of their main trigger: the Arab oil embargo in 1973, for example, or the Russia-Ukraine War in 2022. But those crises didn’t happen in a vacuum, only driven by that single event. Multiple contributing causes added to them. Back in 1973, US oil production had just hit its maximum capacity and the world was facing runaway demand growth. In 2022, multiple contributing factors made the crisis what it was: low nuclear power production in France, poor hydropower generation due to droughts, panic buying by the German government and ill-conceived hedging strategies by utility companies hit by a wave of margin calls.

So far this time, the contributing factors are offsetting: Millions of barrels of Iranian and Russian oil were unsold, with tankers keeping them on floating storage. Those barrels are now finding buyers. For Europe, in particular, the timing is great: Hydropower reservoirs are good, and with spring arriving, solar power generation would make a significant contribution.

The risk, of course, is that the conflict goes on, intensifies, and spreads beyond LNG and oil, pushing up coal and electricity. Could it still be painful? Yes, no doubt. Could it become a true energy crisis? Sure, but only if one assumes a worst-case scenario. In the meantime, zoom out on the price charts. When looking at the last decade, the last week doesn’t look as scary as it does at first sight.

This column reflects the personal views of the author and does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Javier Blas is a Bloomberg Opinion columnist covering energy and commodities. He is coauthor of “The World for Sale: Money, Power and the Traders Who Barter the Earth’s Resources.”

Disclaimer: This report is auto generated from the Bloomberg news service. ThePrint holds no responsibility for its content.

Also read: Will US waiver on Russian crude help India offset Middle East losses? What market analysts say