New Delhi: While battles may be fought on the front line, a decision of equal strategic importance is made far away from the frontier—in the government’s balance sheets.

Every February, headlines echo a familiar theme: India’s defence budget has increased once again—larger figures, greater commitments, enhanced ambitions. As a result, discourse remains centred on allocations—how much has the government earmarked for national security? Yet the more insightful question has received considerably less attention: How much of that allocated money was actually spent, and why did the gap between promise and delivery widen in certain years, only to narrow significantly in others?

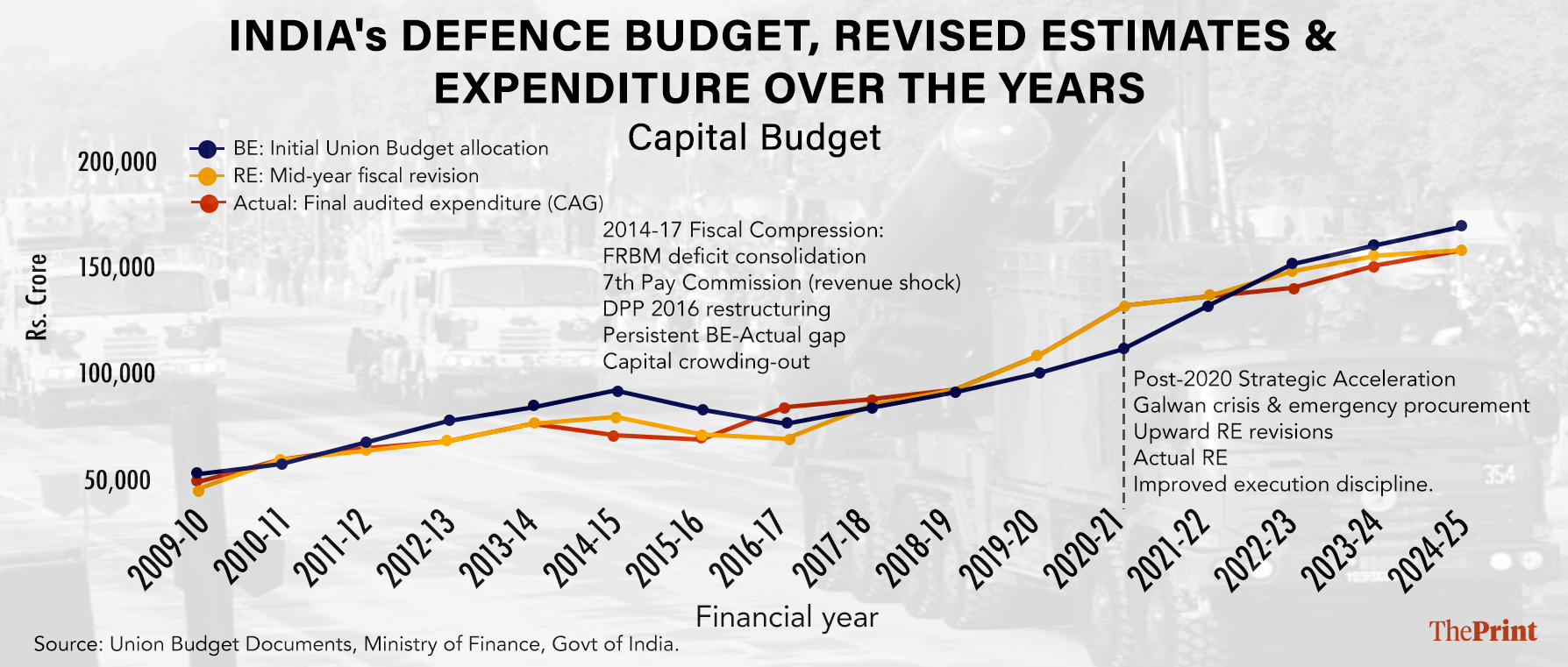

An examination of three long-term datasets—Budget Estimates, Revised Estimates, and actual expenditure—reveals a pattern that extends beyond merely increasing capital outlay. The Indian government, across both UPA and NDA regimes, has often struggled to spend the entirety of what it sets aside as defence capital at the beginning of a financial year.

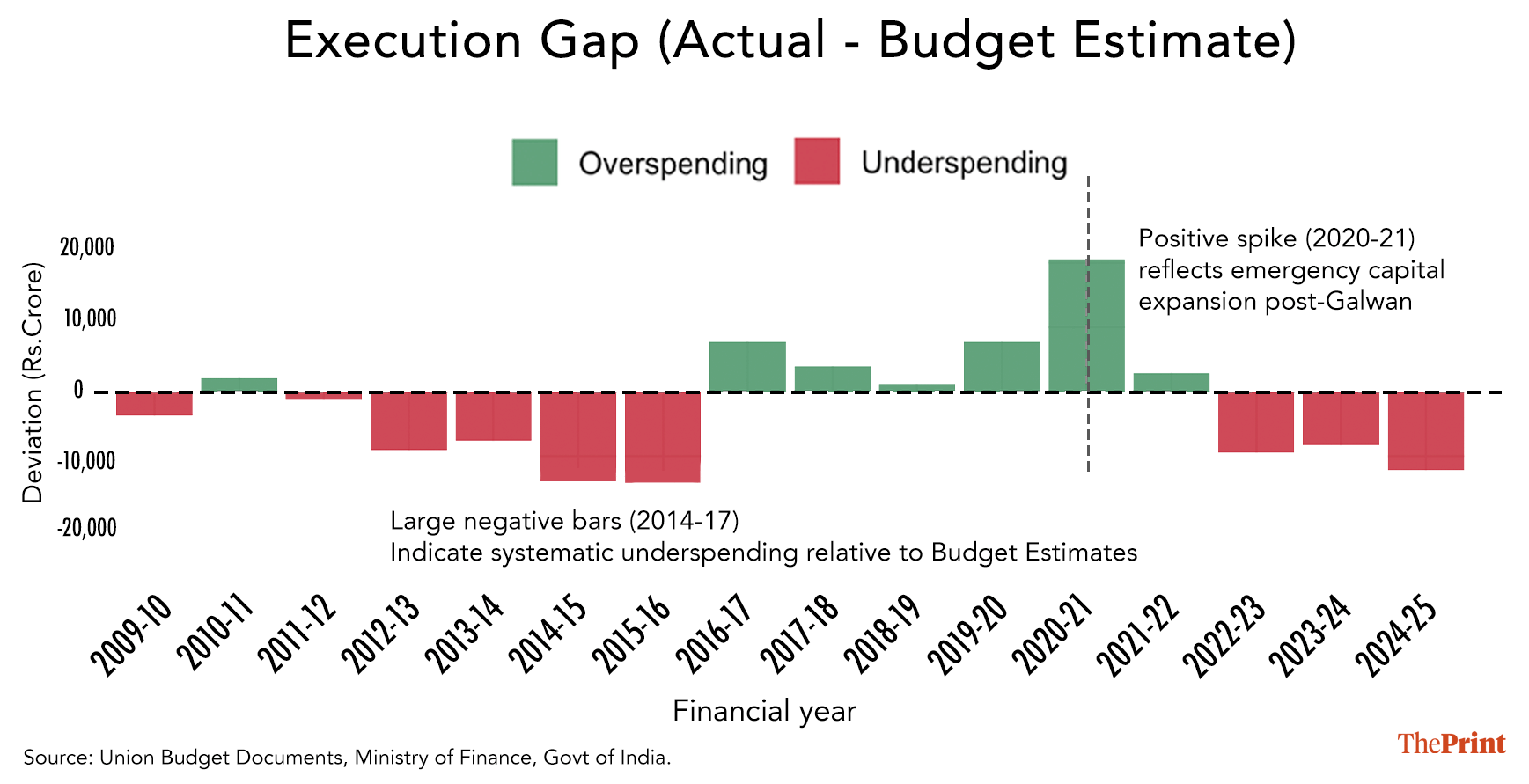

Between FY 2009-10 and FY 2013-14, the Manmohan Singh-led government underspent its defence capital budget, with the exception of FY 2010-11. The trend continued into the tenure of NDA-I under Narendra Modi for the first two fiscal years, with a reversal in FY 2016-17. Massive overspending occurred in FY 2020-21, owing to emergency capital expansion post the Galwan clash. But the trajectory changed soon after, with significant underspending between FY 2022-23 to FY 2024-25.

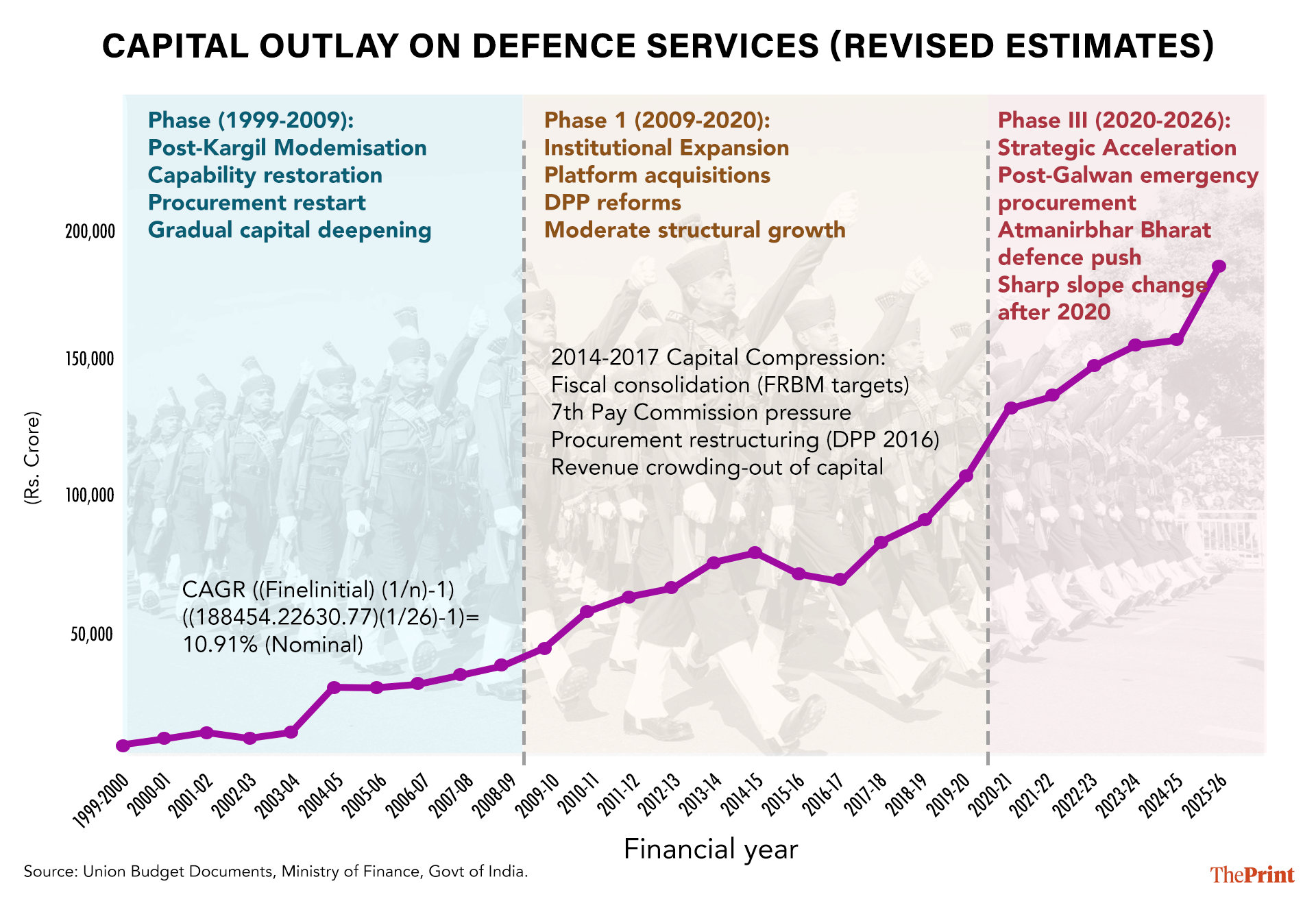

Even if one was to rewind to the tenure of the Vajpayee government, Budget Estimates saw downward revision mid-year from FY 2000-01 to FY 2003-04.

The numbers, through the years, are a reflection of the country’s strategic priorities, intertwined with economic and fiscal factors. They narrate the evolution of a system learning, under pressure, to align ambition with absorption. Beneath the upward trajectory of spending lies a deeper transformation in India’s fiscal governance of defence.

India’s defence budgets have historically been kept controlled and constrained keeping in mind the country’s deficit economy and other key budgetary priorities, such as welfare, subsidies, interest payments, education, health etc. Governments, both UPA and NDA, have in the past been hesitant about spending on defence.

In the last three decades, several events have also shaped the movement of the defence capital budget—from the 1999 Kargil war, to an economic stall (2000 to 2002), One Rank One Pension (2014), the 2016 demonetisation, the Galwan clash (2020), to Operation Sindoor (2025). While some spurred a sense of urgency that pushed up expenditure rapidly, others came in the form of shocks that triggered dips in defence allocations. There was also a phase of underspending due to macroeconomic pressures and possibly, stability-driven complacency.

ThePrint explains this complex trajectory of India’s defence capital budget:

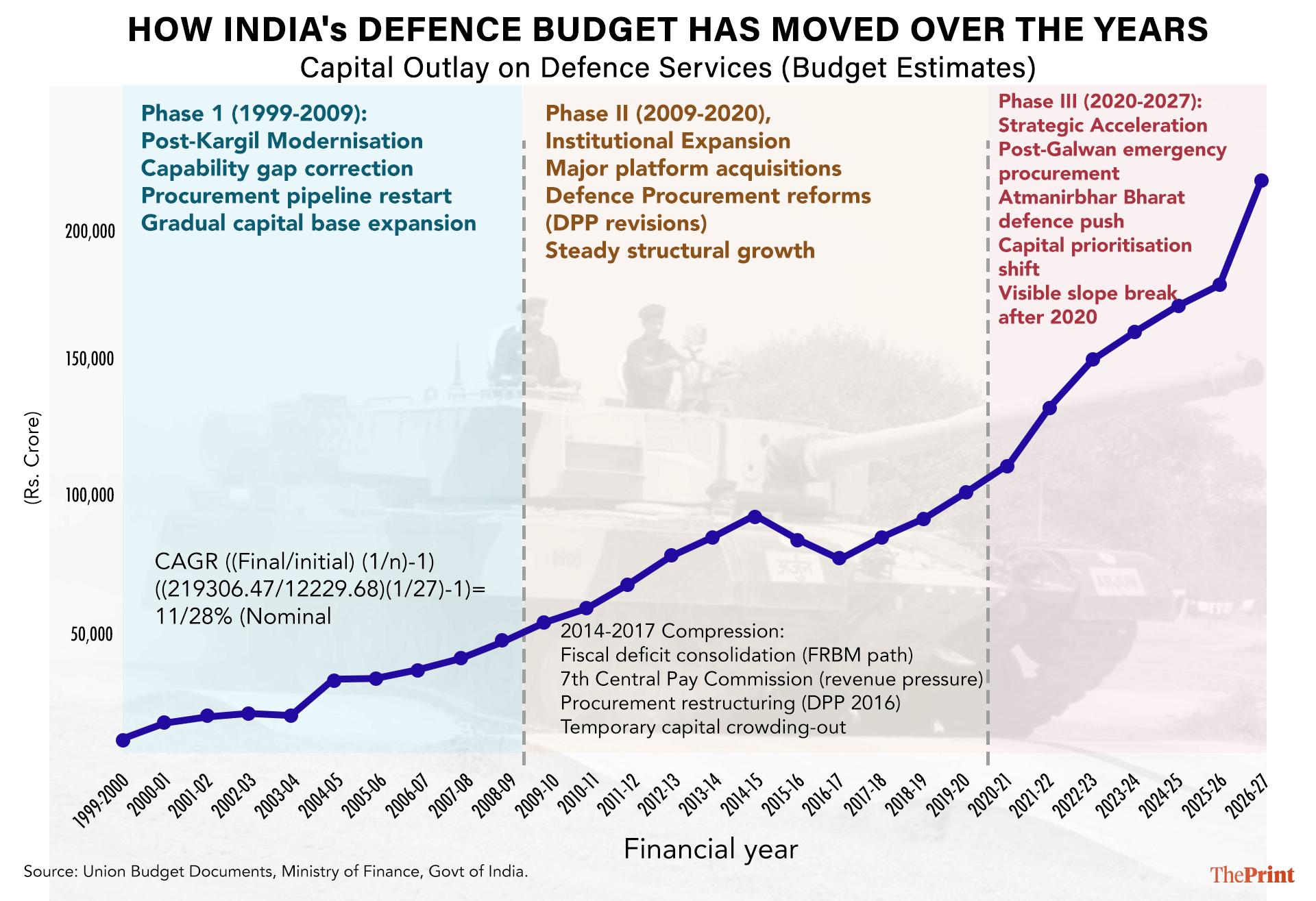

From Kargil to consolidation—expansion with friction

The long-term Budget Estimates trend can be analysed in terms of three distinct structural phases.

1999-2009: Post-Kargil restoration

In the aftermath of the Kargil conflict, India was facing significant capability gaps in areas like surveillance, artillery, ammunition reserves, and high-altitude warfare readiness. During the 2000s, capital outlay increased progressively.

Economically, this period represented a catch-up cycle. Procurement pipelines were reinitiated, legacy delays were resolved, and the capital base expanded in a measured manner. There was no significant fiscal shock during this period, and capital growth remained broadly aligned with macroeconomic expansion.

2009-2020: Institutional expansion & fiscal compression

From 2009 onwards came steady structural growth. Major platform acquisitions, naval expansion and air power modernisation drove higher allocations. Procurement procedures were revised to enhance transparency and promote domestic manufacturing.

However, between 2014 and 2017, the rate of capital expansion visibly flattened. The economic context of this period is crucial. India was consolidating its fiscal deficit under the Fiscal Responsibility and Budget Management (FRBM) framework at the time. Fiscal deficit reduction is not merely an accounting orthodoxy. High deficits increase borrowing, increase interest payments, and can destabilise macroeconomic stability. Consolidation, therefore, necessitated expenditure restraint.

At the same time, the 7th Pay Commission significantly increased salaries and pensions—revenue expenditures that are legally and politically challenging to compress. When revenue commitments rise sharply and fiscal space is constrained, capital expenditure ends up being adjusted—essentially, revenue crowding out capital.

Additionally, the restructuring of the Defence Procurement Procedure in 2016, while intended to promote indigenisation and rationalise categories, is likely to have slowed down approvals in the short term. Typically, contracts are reclassified, compliance requirements shift, and decision-making becomes cautious during such transition. The result, therefore, was not a collapse in capital spending, but a compression. Announced allocations grew, but at a moderate pace relative to the earlier momentum.

Post-2020: Strategic acceleration

After 2020, the numbers indicate a clear inflection point, with capital outlay accelerating sharply. The shift corresponds to the Galwan crisis, and the subsequent reordering of strategic priorities. Capital spending was no longer considered deferrable. It became urgent. The significant spike in the budgetary allocation for FY 2026-27 comes after Operation Sindoor.

Also Read: Defence budget through the years: Big leap for 2026-27, but what numbers since 1999 reveal

Announcements vs absorption—the underspending phase

To understand the compression phase, it is essential to look at the actual capital expenditure in relation to Budget Estimates. Between 2014 and 2017, actual spending consistently fell short of Budget Estimates, resulting in an expanding execution gap, which reflects systematic underspending.

The underlying causes point to the macroeconomic pressures prevalent during that period. The consolidation of the fiscal deficit necessitated stringent expenditure control, while the Pay Commission’s recommendations increased committed revenue expenditure.

Additionally, procurement restructuring delayed contract finalisation. In situations where ministries encounter cash management constraints, capital payments are frequently deferred to safeguard revenue obligations.

This was not necessarily a case of strategic neglect, but rather fiscal prioritisation under constraint. The figures illustrate a period in which defence modernisation ambitions were moderated by macroeconomic discipline and institutional transition. Although budget figures indicated intent, the limitations of absorption capacity and fiscal space limited delivery.

Galwan & the shift to execution discipline

The Revised Estimates highlight a significant behavioural shift post-2020. Prior to 2014, revisions were modest and generally stable. Between 2014 and 2017, downward adjustments reflected a realistic approach under fiscal stress, with planned spending being curtailed mid-year.

However, post-2020, Revised Estimates have shown an upward trend, indicating that mid-year fiscal recalibrations were employed to expand rather than compress capital outlay. The use of emergency procurement powers expedited timelines, and strategic urgency took precedence over previous caution.

The post-2020 period reveals another critical development—the narrowing of the gap between Budget Estimates and actual spending. In FY2020-21, actual expenditure even surpassed initial Budget Estimates, reflecting rapid mobilisation. In subsequent years, the actual spends have been closely aligned with Revised Estimates. The convergence points to improved forecasting and coordination between the defence and finance ministries, and more effective procurement execution. It indicates that allocations were not merely political statements, but operational commitments.

Economically, India appears to have transitioned from optimistic budgeting with slippage, to responsive budgeting with discipline.

The broader takeaway is not merely that India is increasing its defence expenditure, but that fiscal governance has undergone significant evolution. The period preceding 2017 illustrates how capital modernisation efforts can be constrained by revenue pressures and deficit consolidation. Conversely, the post-2020 phase demonstrates how strategic shocks can act as catalysts for institutional acceleration, thereby aligning allocation with execution.

The central issue is sustainability. While strategic urgency can improve system efficiency, the question remains whether execution discipline will persist if fiscal pressures re-emerge. Revenue expenditure in defence continues to be structurally high. Future pay revisions, pension liabilities, or macroeconomic slowdowns could once again challenge capital prioritisation.

Recent data suggests that after years of friction, India may finally be achieving alignment between ambition and absorption. If the alignment is maintained, the true reform in India’s defence sector will not be a singular platform acquisition, but the gradual institutionalisation of fiscal credibility.

(Edited by Mannat Chugh)