Long before the first missiles were fired in the Middle East, the warning signs of a 2013-style capital exodus were visible in the gap between India’s ambitions and economic resources. Once the Iran war revived the dollar’s safe-haven appeal, the bottom gave way under the rupee.

Asia’s worst-performing currency over the past year weakened through a key psychological barrier of 95 against the greenback to hit a record intraday low of 95.12 on Monday. The conflict in the Persian Gulf is the trigger for the unusual weakness, but the fragility is domestic.

Traders rightly sensed Reserve Bank of India’s mandate to cap local banks’ end-of-day currency positions at $100 million as a desperate measure. Announced late last Friday, the restriction was widely expected to knock off one-way bets against the rupee. But it backfired. The market is no longer confident that the RBI will be able to stop the rupee from slipping past 100. After all, when a monetary authority restricts how lenders manage their books, it unwittingly ends up signaling that traditional tools like interest-rate hikes or dollar sales are no longer sufficient. That’s when speculators swoop in.

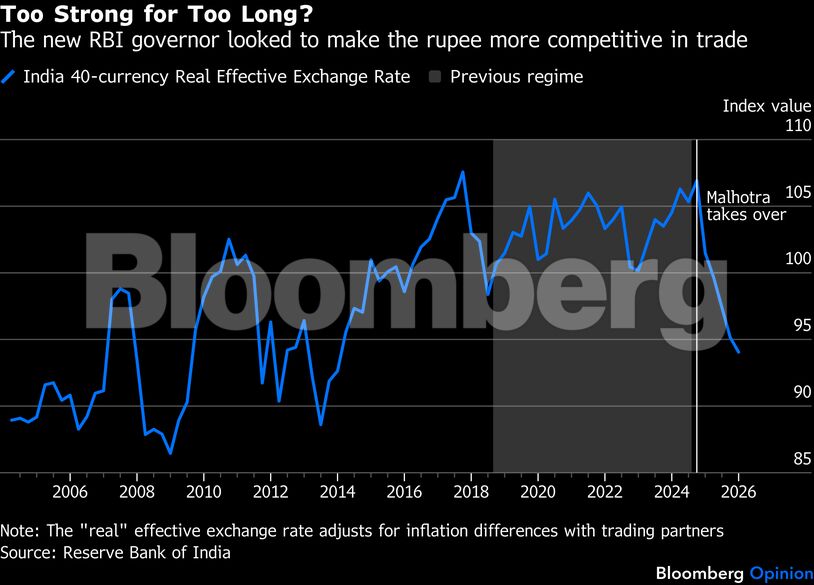

In a globally integrated financial system, a central bank faces a choice: It can either defend the exchange rate or control domestic interest rates. It cannot do both. For too long, the RBI tried to skirt this reality. Governor Sanjay Malhotra inherited a rupee that had become overvalued under his predecessor’s strategy of squeezing out exchange-rate volatility to anchor inflation. After taking charge in late 2024, the new chief slashed interest rates to revive investment — effectively taking his foot off the other stool. He let the rupee weaken to insulate the economy from the Trump administration’s tariff chokehold on exports.

The gamble worked for a while, but when the oil shock hit, it became untenable. To save the currency now, the monetary authority might have to raise borrowing costs, thereby stifling growth. To save growth, it must let the rupee go. Neither option is appealing.

For the middle class, a triple-digit rupee translates into a higher cost of living. The domestic Indian consumer lacks the financial cushion to withstand global energy spikes, which cannot be absorbed by the state without losing its barely investment-grade credit rating. With Brent crude four-fifths more expensive than earlier this year, a weaker currency acts as a double tax by amplifying the rupee-denominated price of imported fuel. This pressure migrates from the pump to the food-supply chain as transport, cooking-gas, and fertilizer costs rise in tandem.

The impact extends to aspirational spending. India is the leading source of international students in the US. An 8% depreciation in a single year can render a multi-year degree unaffordable for families who have already stretched their finances and taken out education loans.

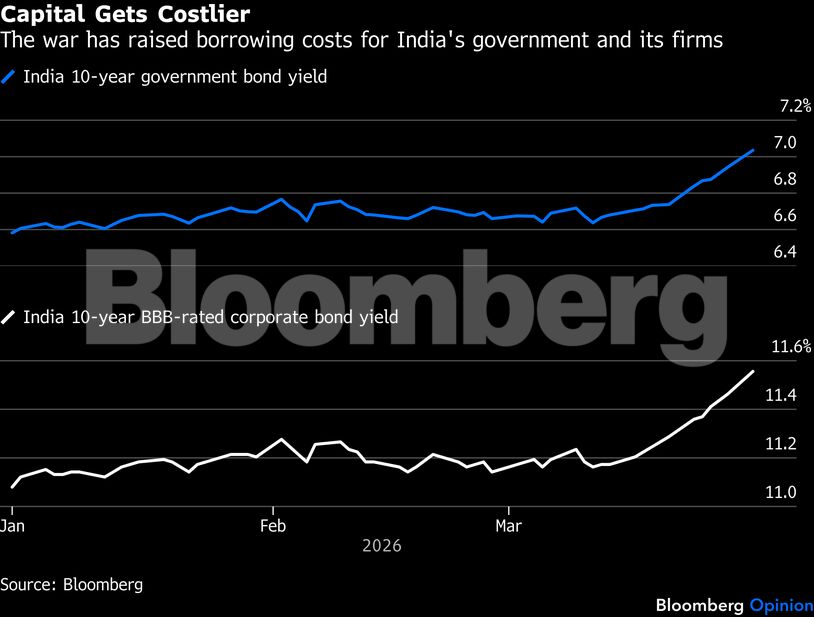

The federal government will have to borrow heavily to maintain subsidies on fertilizer and cooking gas to prevent rural unrest. This fiscal strain is showing up in the secondary market where the yield on the 10-year benchmark sovereign bond climbed to a near-two-year high of 7.1% Thursday. None of this augurs well for funding India’s 2026-2027 infrastructure pipeline.

The pressure is more acute at the regional level. Investors are balking at Indian states’ high debt-to-GDP ratios and cash-for-votes programs that create no long-term assets. Constraints on public funding push private borrowers out — even companies without foreign debt face higher borrowing costs, stymying capital expenditure.

On the eve of the 2013 taper tantrum, India ran loose monetary and fiscal policies in the face of high inflation. The market forced a correction by pummeling the rupee. Back then, households weren’t happy with low real returns on bank deposits. This time around, there has been little price pressure, at least under Malhotra’s supervision, but savers have been busy chasing yields in a red-hot market for initial public offerings. Then, when precious metals surged last year, the love for gold kicked in — just like in 2013. The banking system’s liquidity shortage worsened.

Global investors judge markets on dollar-denominated returns. If the local currency loses 10% of its value, equity gains vanish. The record $12 billion outflow from Indian stocks in March indicates the exit sign is currently more attractive than the growth story. As capital leaves, the rupee weakens further.

The most acute pain is felt by the working poor. They rely on labor-intensive sectors like textiles and diamond polishing, which have seen margins collapse under 50% US tariffs, energy shortages, and waning global demand. What’s more, the safety net of remittances from family members overseas is fraying as the Iran conflict threatens jobs in the Gulf. Without this inflow, overleveraged rural households will be further in debt to meet basic needs.

After Monday’s debacle, the RBI managed to engineer the biggest rally in the rupee in 12 years on Thursday by doubling down on currency controls. Such administrative measures could delay the slide, but they may not steady the rupee at 93. As the exchange rate nears 100, the focus must shift from defending a number to managing the social and economic consequences of a weaker currency.

Fortunately celebrities are not adding to the pain by mocking the fall of the Rupee.