The average Indian investor today faces high unpredictability on multiple fronts: the United States and Israel’s war on Iran, the US yo-yoing on its trade policy, the volatility of the Indian rupee, and AI-linked technological disruptions. Such volatility risks pushing households back toward gold and real estate, just as India’s financialisation of savings begins to gather momentum. How should policy respond to this threat?

Indian households and institutional custodians of Indian savings, such as pension and provident funds, should be encouraged to diversify their portfolio globally. While the gains from global diversification have been generally shrinking, the war on Iran shows that international diversification also helps shrink war-linked losses. Indian policymakers’ role, therefore, is to reverse their decades-old anti-diversification stance and remove the frictions associated with international diversification.

Gains from diversification

Assets distributed across different countries and regions are less correlated than those concentrated in the same country and region—they tend not to move in the same direction. A globally diversified portfolio acts as natural insurance against country-level or regional stocks.

However, the gains from international diversification have been reducing as the world gets increasingly integrated. These gains depend on low correlations between foreign and domestic stock returns. The financial econometrics literature since the 1990s suggests that returns on international securities have become more correlated over time due to the integration of financial markets.

In sum, the gains exist, but are getting thinner.

Also read: What India can learn from the US-Israel war on Iran

Diversification pays, except during war

Diversification benefits often shrink during wars because global markets react simultaneously to geopolitical shocks. However, the extent of the shrinkage depends on the nature of diversification.

War announcements produce significant negative returns—estimates vary from -1 to -10 per cent in many markets—in the short run. The impact across equity markets is, however, uneven. Developed markets tend to move together, as do markets with greater economic ties to the region of conflict. For example, researchers have shown that Russia’s war on Ukraine significantly reduced equity returns across the G7 countries in the short run, but the shrinkage was way smaller across select markets in Africa.

The takeaway is that diversification across multiple developed countries alone may not help in the face of war, as developed countries’ markets tend to move together. A truly globally diversified portfolio is one that is diversified across developed and developing markets.

Gains diminish, but so do losses

It is tempting to discount the virtues of diversification during wartime due to the diminishing returns. However, the US-Israeli war on Iran has so far shown the opposite for Indian households and institutional investors. Despite shrinking gains from diversification, a diversified Indian portfolio would be better off than one solely focused on India.

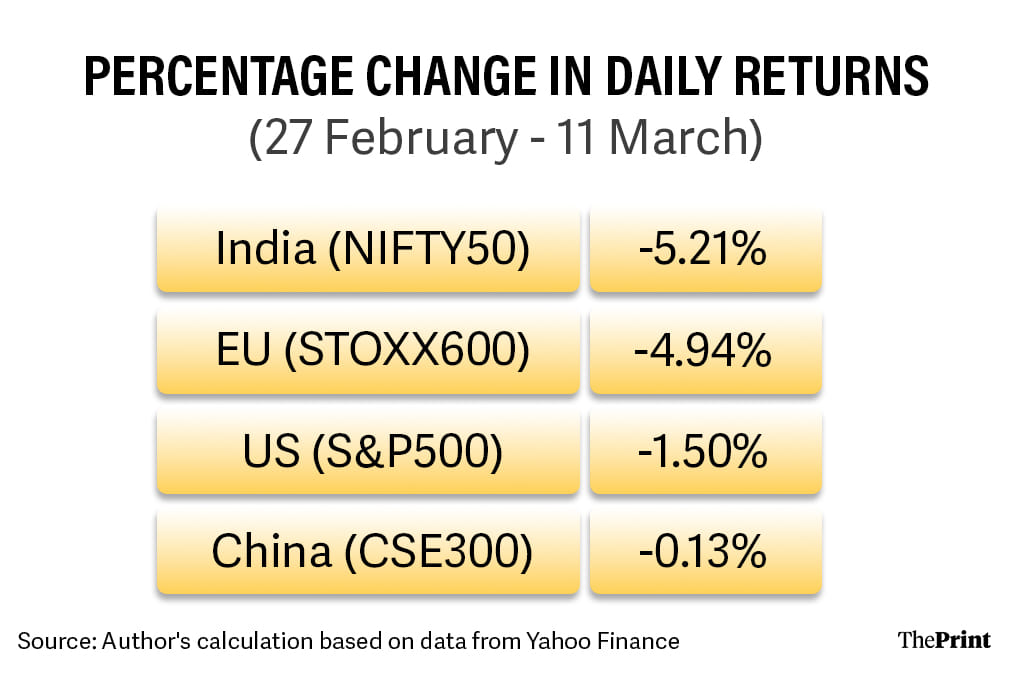

The table below shows the performance of four widely traded indices during the period beginning 27 February—a day before the US and Israel mounted strikes on Iran—and ending on 11 March. Two of these indices, S&P500 and STOXX600, represent the most widely traded companies in the US and the European Union, respectively. CSE300 represents the largest Chinese companies by market capitalisation. NIFTY50 is the Indian index.

It is clear that an India-only portfolio bore the brunt of the war. A US-only portfolio would be moderately affected, and a China-focused one would remain mostly unchanged. This is not to say that one must invest in China or the US alone. Doing so would expose the portfolio to shocks specific to those countries.

The insight from this experience is that while a NIFTY-only portfolio declined by 5.21 per cent since the strikes on Iran, a portfolio equally diversified across these four asset classes would have declined by about 2.95 per cent. So, diversification would not have delivered gains, but would have reduced losses by about 43 per cent.

The shrinking of gains from diversification does not mean that it is no longer beneficial. On the contrary, as the current experience shows, an internationally diversified portfolio continues to be a hedge against global shocks, even as large as the war on Iran.

Also read: Nepal must go back to old map, assure Delhi its territory won’t be used against India

India’s anti-diversification policy stance hurts

How do we square the circle of diminishing returns and diminishing losses associated with international diversification? For India, this requires policymakers to ensure that the returns from international diversification must outweigh the costs associated with it. Indian financial portfolios have been hobbled by the government’s and regulators’ decades-old anti-diversification stance. The State either caps or imposes heavy transaction costs on global diversification. Three policy interventions stand out.

First, the RBI imposes a maze of controls on who can invest outside India, for what purposes, in what kinds of instruments, and on what terms and conditions. Unlisted Indian companies cannot directly invest in listed stocks abroad. Listed Indian companies’ offshore portfolio is capped as a percentage of their networth. For retail investors, a viable route to take global exposure was through Indian mutual funds and exchange-traded funds (ETFs) with schemes dedicated to global stocks. However, the aggregate exposure that such mutual funds could take to foreign listed securities was capped at $7 billion in 2009. The industry reached this cap in 2022, shutting down this route as well. This is the most significant barrier preventing the diversification of Indian retail portfolios.

Second, retail investors can still take exposure by sending remittances abroad under a Liberalised Remittance Scheme (LRS) that allows Indian individual residents to remit up to $250,000 annually abroad for any purpose, including investing in stocks. This limit is, by itself, enough to allow households to globally diversify. However, as Renuka Sané and I have argued earlier, the transaction costs associated with directly investing abroad are high. These come in varied forms: minimum investment size, remittance and brokerage fees, and tax traps in countries like the US, which imposes a 40 per cent estate tax on equity holdings exceeding certain thresholds. The recent 20 per cent TCS levied by the Indian government on all remittances under LRS amplifies these transaction costs. As the gains from global diversification diminish, these transaction costs make it harder to justify a global diversification strategy for any retail investor.

Third, the custodians of large Indian household savings, such as pension funds, are also entirely focused on India-only portfolios. For example, the PFRDA Act—the law governing pension funds in India—prohibits pension fund managers from investing subscribers’ money in international securities. For due measure, the law clarifies that pension funds cannot make such investments directly or indirectly, implying that they cannot globally diversify through Indian mutual funds or Indian exchange-traded funds either. The EPFO similarly invests its entire corpus in Indian securities, with zero global exposure.

In sum, Indian financial portfolios are not by choice, but by policy design, long India, but long only India.

Concentrated risks

The financialisation of Indian household savings is one of the most important economic shifts of the past decade. But financialisation without diversification creates fragile balance sheets. By restricting global investment, the State is forcing its savers to take concentrated risks in a single economy.

In an era of geopolitical shocks, technological disruption and volatile capital flows, diversification is not a luxury. It is basic risk management. If policymakers want Indian households to trust financial markets, they must allow them to diversify beyond India’s borders.

Bhargavi Zaveri-Shah is the co-founder and CEO of The Professeer. She tweets @bhargavizaveri. Views are personal.

(Edited by Prasanna Bachchhav)