In recent years, the concept of ‘de-dollarisation’ has transitioned from academic debate to a prevalent topic in geopolitical discussions. From BRICS summits to energy trade negotiations, policymakers are increasingly advocating for a reduction in reliance on the US dollar. Factors such as sanctions on Russia, the rise of China, and a more fragmented geopolitical environment have intensified speculation that the international monetary system may be entering a transformative phase. However, during periods of genuine uncertainty in global financial markets, investor behaviour tells a very different story.

In times of crisis, there remains a pronounced tendency to gravitate towards the dollar.

Over the past two decades, episodes of financial stress, geopolitical conflict, and market panic have consistently bolstered the dollar rather than weakened it. This explanation is attributable not to political dynamics but to the foundational architecture of global finance.

When panic hits, liquidity wins

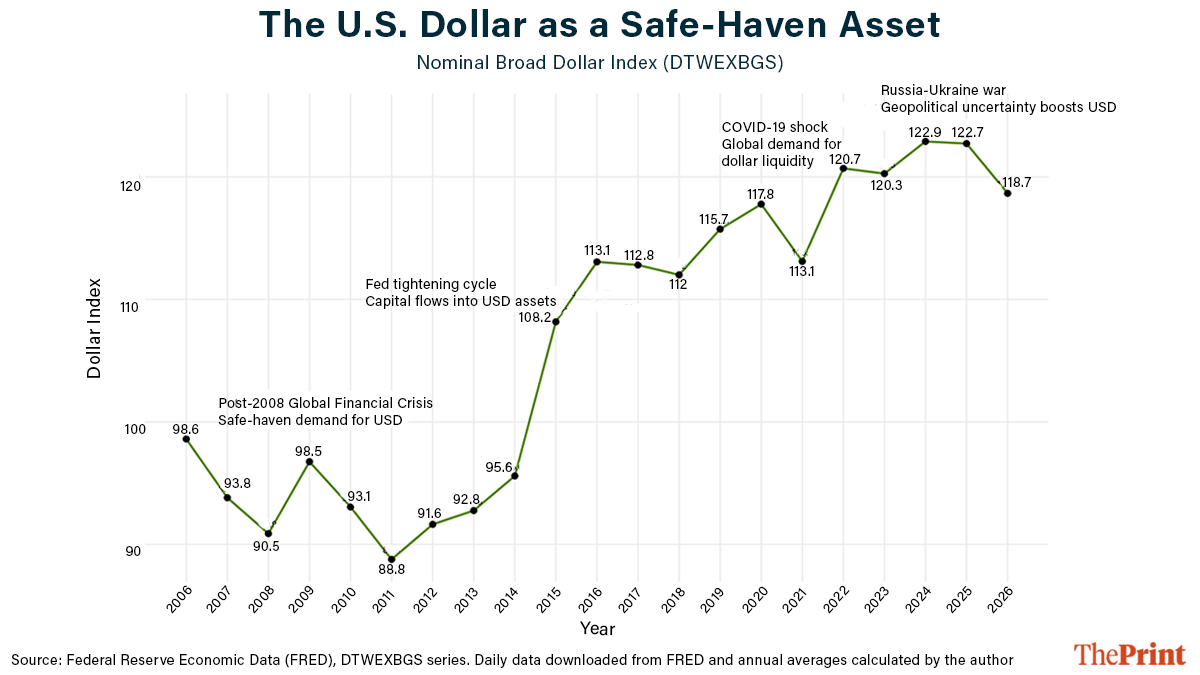

Consider the global financial crisis of 2008. The crisis originated within the United States, triggered by the collapse of American mortgage markets and the failure of major financial institutions. One might have anticipated that investors would abandon the currency at the epicentre of the turmoil. However, the opposite occurred.

As markets descended into panic, global investors rushed to acquire US Treasury securities. Capital flowed into dollar-denominated assets despite the crisis having begun within the American financial system. This pattern reemerged during the Covid-19 pandemic of 2020. As financial markets froze and uncertainty escalated, companies, banks and governments around the world scrambled to secure dollar liquidity.

A similar dynamic ensued following Russia’s invasion of Ukraine in 2022. The conflict incited volatility in energy markets, sweeping sanctions, and heightened geopolitical risk. Once again, demand for dollar assets surged. Economists frequently describe this behaviour as the safe-haven effect. During periods of instability, investors prioritise liquidity above almost everything else. They seek assets that can be traded easily, in substantial quantities, and within stable legal systems.

No market globally currently matches the scale and liquidity of US Treasury securities. Consequently, in times of global uncertainty, the dollar functions as the ultimate financial refuge.

The recurring pattern is visible once again in the current geopolitical climate. As tensions intensify in the Middle East, particularly following the confrontation involving Israel, Iran and the United States, the US dollar has experienced a strengthening in global markets. The increase in geopolitical risk and the volatility of energy prices have driven investors toward dollar-denominated assets, thereby reinforcing a well-established tendency in global finance: As uncertainty escalates, so does the demand for dollar liquidity.

Also read: India uses BRICS to push reforms—not to challenge the US

The sanctions paradox

Recent geopolitical developments have introduced an additional dimension to the ongoing debate. Over the past decade, the United States has increasingly employed financial sanctions as a tool of foreign policy, encompassing actions such as freezing reserves, restricting banking access, and limiting participation in global payment systems. The comprehensive sanctions imposed on Russia following its invasion of Ukraine have illustrated the extraordinary reach of the US financial system. Critics argue that this “weaponisation” of finance will accelerate the search for alternatives to the dollar. In response, some countries have increased their gold reserves, experimented with local currency trade, and even explored alternative payment mechanisms.

However, sanctions also reveal another aspect: The remarkable infrastructure that sustains the dominance of the dollar.

Global finance remains intricately linked to dollar-based institutions, including correspondent banking networks, dollar-clearing systems, and international bond markets. Sanctions are effective precisely because a significant portion of global finance passes through these channels. This situation creates what may be termed a sanctions paradox. The more visible the power of the dollar system becomes, the more evident it is why operating outside of it is so challenging.

Also read: A BRICS currency can weaken US hold over emerging economies. India needs to decide its role

Can the world actually de-dollarise?

The international monetary system is not destined to remain static indefinitely. Over an extended period, economic transformations may gradually alter the currency landscape. China’s expanding economic influence, regional financial arrangements, and technological advancements, such as digital currencies, may gradually diversify the system. Certain nations may seek to reduce exposure to sanctions risk by conducting more trade in alternative currencies. As a result, a more multipolar monetary order is conceivable in the forthcoming decades. However, structural changes in global currency systems typically transpire over generations rather than political cycles.

The underlying reason is attributed to what we, in economics, refer to as network effects. The dollar predominates in global trade invoicing, cross-border lending, and international bond markets. According to IMF data, it still constitutes approximately 58 per cent of global foreign-exchange reserves. The euro lags significantly behind, while other currencies remain relatively minor participants.

The more widely a currency is used, the more convenient it becomes for others to adopt it as well. These self-reinforcing networks establish formidable barriers to change. Effectively, the dollar functions as the operating system of global finance.

Replacing such a system necessitates not only a rival currency but also an equally robust financial market, trusted institutions, and a global ecosystem of banks, investors, and payment infrastructure. Currently, no alternative offers this combination. This is exactly why discussions regarding de-dollarisation often confuse geopolitical ambition with financial reality.

Governments may aspire to reduce reliance on the dollar, but markets continue to depend on it. When global uncertainty escalates—when wars erupt, financial markets fluctuate, or economic shocks reverberate across continents—investors do not seek a new financial centre. They revert to the one that already exists.

The paradox of the international monetary system is that the very forces frequently cited as evidence of American decline, namely, geopolitical instability, sanctions and financial fragmentation, often reinforce the currency at its core. In an increasingly uncertain world, the dollar is not merely enduring global crises; it is frequently strengthened by them.

Bidisha Bhattacharya is Consulting Editor (Economy) at ThePrint. She tweets @Bidishabh. Views are personal.

(Edited by Theres Sudeep)