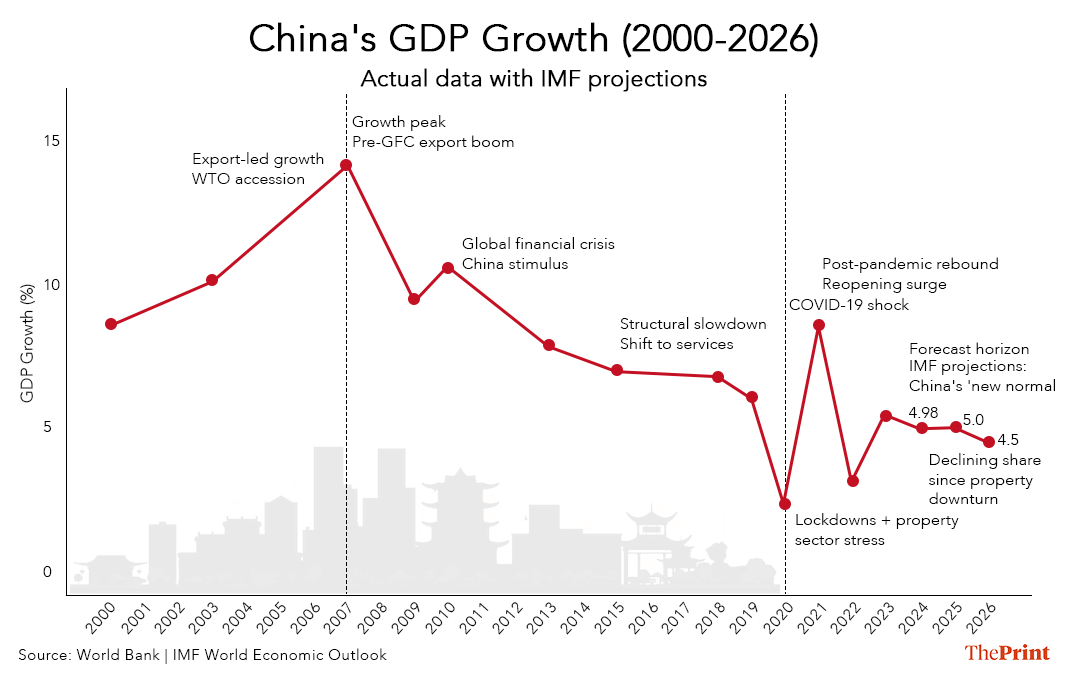

For over 30 years, a single statistic has characterised the dynamics of the global economy: China’s growth rate. Consistently, the world’s second-largest economy has expanded at an exceptional pace, often achieving double-digit growth. However, this era may now be approaching its conclusion. During China’s annual parliamentary meetings this week, Beijing indicated its comfort with targeting an economic growth rate of approximately 4.5-5 per cent. While such expansion would be commendable for most nations, for China, it signifies a profound shift. The nation, once perceived as capable of sustaining rapid growth indefinitely, is now transitioning to a much slower trajectory.

This shift is not merely a cyclical slowdown; it signifies the gradual depletion of the economic model that fuelled China’s rise.

The model that built modern China

Over the past four decades, China’s economic growth has been driven by a potent combination of investment, exports, and construction. The nation allocated substantial resources to infrastructure, manufacturing facilities, and urban development. High savings rates, robust state coordination, and an open global trading system facilitated China’s rapid industrialisation.

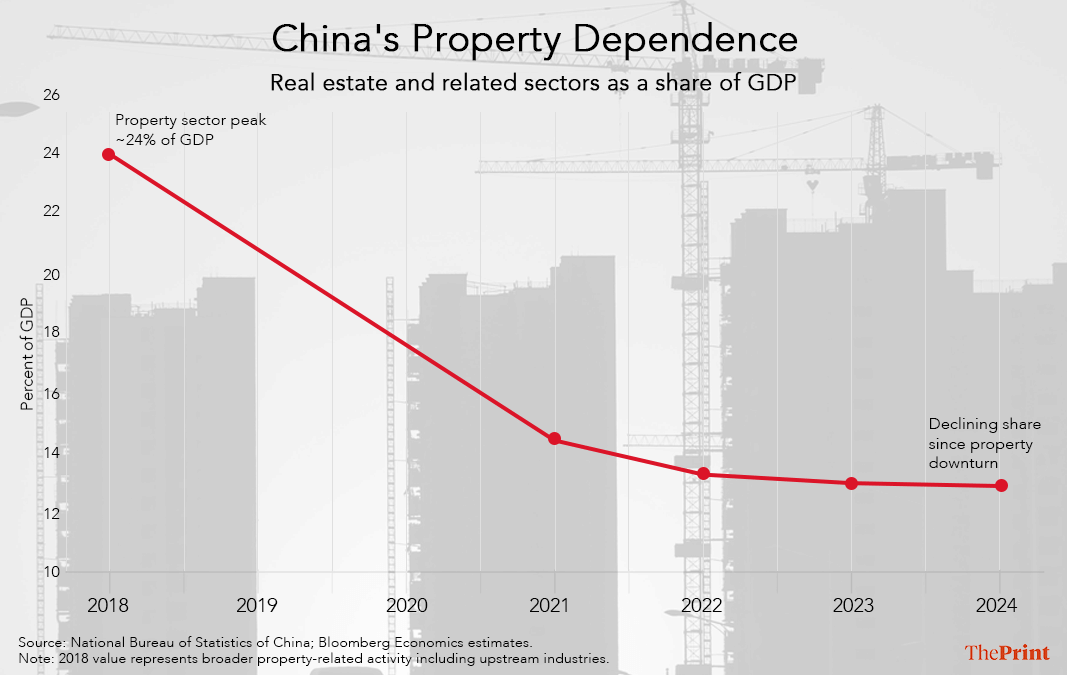

Central to this growth model stood the property sector. Housing construction, land sales, and real estate investment emerged as pivotal drivers of economic activity. At its peak, the property sector and its associated industries constituted approximately a quarter of China’s GDP, influencing sectors ranging from steel and cement production to local government finances.

The consequences of that dependency are now becoming evident. China’s property sector has entered a sustained downturn, with major developers grappling with significant debt burdens and weakening housing demand. The decline in property investment has reverberated throughout the broader economy, impacting construction activity, local government revenues, and household wealth.

The limits of the old model

Concurrently, the previously effective investment-intensive strategy that facilitated rapid expansion is now encountering diminishing returns. Following decades of constructing highways, railways, and urban centres, China has established extensive infrastructure networks. Consequently, further investment yields reduced economic benefits while worsening debt levels among local governments and state-owned enterprises. This pattern is well-documented in development economics. In the initial stages of growth, nations can achieve rapid expansion by transitioning workers from agriculture to manufacturing, importing foreign technology, and developing basic infrastructure. These transformations result in large productivity gains, enabling economies to grow at remarkable rates — a phenomenon often referred to as catch-up growth.

However, this process eventually decelerates. As urbanisation reaches maturity and infrastructure networks become largely complete, additional investment produces smaller gains. Economists describe this as diminishing returns to capital: the more roads, factories, and residential buildings a country possesses, the less each additional one contributes to growth. China appears to be approaching this stage.

History precedents exist, such as Japan’s similar slowdown following its post-war boom in the early 1970s, and the moderation of growth in South Korea and Taiwan upon reaching middle-income status. The transition from rapid expansion to more stable growth is a recognised phase in the development of successful economies.

Also read: How China sees Iran’s post-Khamenei trajectory. It depends on four factors

Beijing’s search for the next growth engine

In response to these structural transformations, Chinese policymakers are attempting to reformulate the nation’s growth paradigm. Official discourse increasingly underscores the importance of “high-quality growth”, a term indicative of a shift from mere rapidity to a focus on sustainability, innovation, and productivity. A key objective is to enhance the contribution of household consumption. In comparison to advanced economies, consumer expenditure constitutes a relatively modest proportion of China’s GDP. Stimulating increased household spending could help reduce the dependency on investment and property-driven growth. However, this transition presents challenges. Diminished consumer confidence, employment concerns, and declining housing wealth have rendered households cautious.

Another pillar of China’s strategy is technological advancement. Beijing is making substantial investments in sectors such as artificial intelligence, robotics, electric vehicles, and advanced manufacturing. The goal is to move up the global value chain while diminishing reliance on foreign technologies. Despite a deceleration in growth, China will persist as a pivotal force in the global economy. Its vast scale ensures that annual expansion continues to contribute significantly to global output. Nonetheless, the nature of China’s economic influence is evolving.

A slower Chinese economy could suppress global demand for commodities that previously fuelled construction booms. At the same time, Chinese enterprises facing weaker domestic conditions may intensify their expansion into international markets, thereby pumping up competition in manufacturing sectors globally. For nations such as India, this moment is particularly important. As China transitions to a phase of moderate expansion, India is anticipated to experience more rapid growth in the forthcoming years — a divergence that could reshape investment flows and supply chains across Asia.

Nevertheless, it would be premature to interpret China’s slowdown as a decline. The country is undergoing a transition that many rapidly developing economies eventually encounter: moving from high-speed catch-up growth to a more mature, stable model.

The true narrative, therefore, is not that China is faltering, but that the era of miraculous growth — a defining characteristic of the global economy for a generation — is gradually concluding.

Bidisha Bhattacharya is an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Aamaan Alam Khan)