As tensions between Israel and Iran intensified, the price of Brent crude oil responded almost immediately. At the same time, insurance costs for tankers in the Gulf region increased. Media channels were quick to go back to 1973, a year when the oil embargo significantly altered the global economy and triggered a surge in inflation.

This reaction is a well-known pattern. Each escalation in the West Asian region revives the same concern: will oil prices escalate, inflation rise, and policymakers lose control?

While the comparison to past events is tempting, it is not yet proven. The real question is not whether oil prices increase during conflicts, as they typically do, but whether they remain elevated for a sufficient duration to change the prevailing inflationary regime.

Oil markets price fear

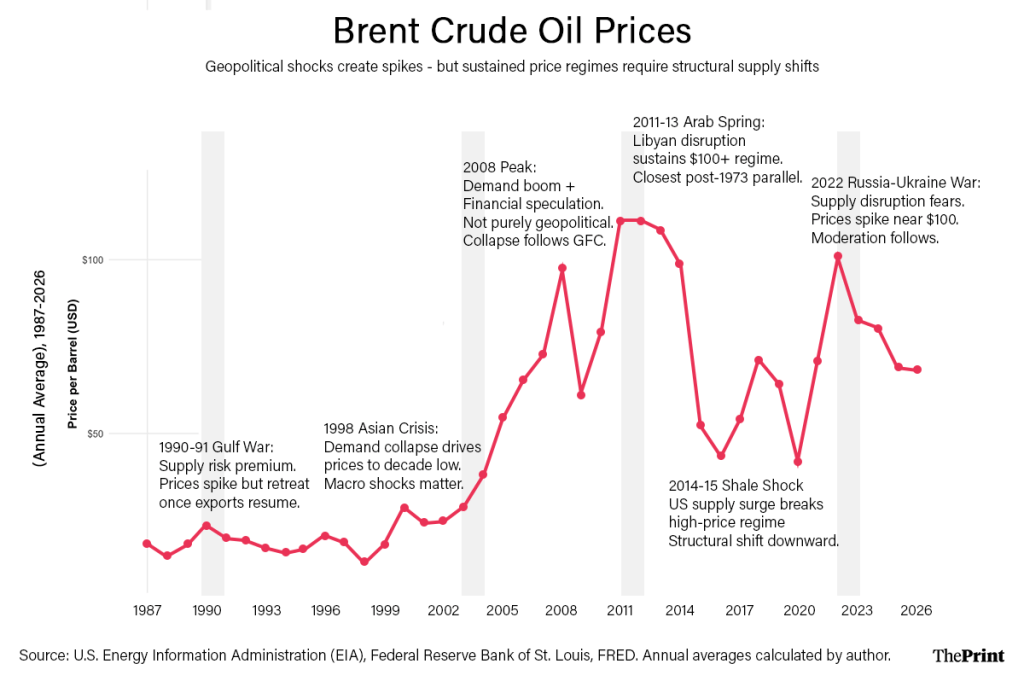

Four decades of annual data present a consistent story. Oil prices experience spikes at the onset of geopolitical disruptions, such as the Gulf War, the Iraq invasion, the Arab Spring, and Russia’s invasion of Ukraine. In 1990-91, Brent crude oil prices surged as Iraqi forces invaded Kuwait, only to decline within two years. The 2003 Iraq War similarly lifted crude prices but did not result in a lasting shortage.

During the dramatic peak in 2008, over the surging global demand and constrained supply, prices nearly reached an average of $100 per barrel. It eventually collapsed as global demand weakened during the financial crisis. The only period resembling a sustained regime was 2011-13, when disruptions in Libya pushed the prices above $100 for three years. However, this period ended not due to the absence of geopolitical tensions, but because of an expansion in supply, with US shale production fundamentally altering the balance.

The situation in 1973 was different, as supply was deliberately and persistently withdrawn, leading to a prolonged increase in prices and embedding inflation expectations. The post-1987 record does not suggest that every escalation in the Middle East results in a structural shift. Nevertheless, for India, even temporary spikes matter, and the reason is arithmetic.

India imports approximately 85 to 88 per cent of its crude oil requirements, amounting to more than 4.5 million barrels per day. In most years, crude oil alone constitutes nearly a quarter of India’s merchandise import expenditure. Around 60 per cent of these imports originate from West Asia, indicating that geopolitical instability in the Gulf is not merely a global concern but is directly linked to India’s external economic balance.

While the direct impact of oil on the consumer price index (CPI) is limited, its indirect influence is substantial. Oil permeates the economy through sectors such as transportation, fertilisers, plastics, logistics, and aviation fuel, in ways not always reflected in the CPI basket. A sustained increase of $10 in crude oil prices significantly widens the current account deficit, complicates fiscal calculations, and raises costs across various sectors. However, India’s vulnerability extends beyond oil.

It intensifies when oil prices intersect with fluctuations in the dollar.

Also read: Iran’s dictatorship deserved universal condemnation—but US-Israel strikes not reliable cure

The double exposure

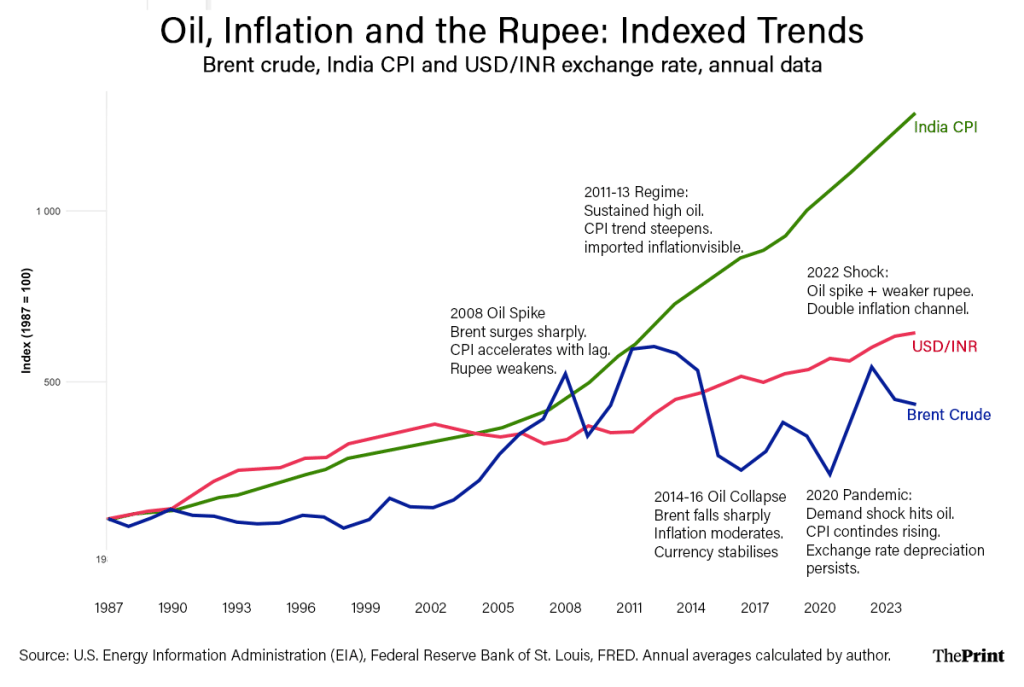

Oil is denominated in dollars, and during periods of global economic stress, the dollar tends to appreciate. When oil prices increase, currently with the appreciation of the dollar, India experiences a compounded economic impact. This is due to the global rise in oil prices and the increased cost of each dollar in terms of rupees.

Historical trends illustrate this phenomenon clearly. In 2008, there was a surge in oil prices, the rupee weakened, and inflation accelerated with a lag. Similarly, during the prolonged period of elevated oil prices from 2011 to 2013, inflationary pressures intensified. In 2022, following Russia’s invasion of Ukraine, there was a significant spike in oil prices alongside a global strengthening of the dollar, which amplified imported inflation across emerging markets.

While India is not alone in encountering this dynamic, its high oil import dependence and increasing energy demand render its exposure particularly significant. Consequently, the discourse on inflation in India must extend beyond considerations of monsoons and repo rates. When a substantial portion of inflationary pressures is externally driven, monetary policy tightening alone is insufficient to fully mitigate these effects. The Reserve Bank of India cannot increase oil supply; it can only manage expectations and liquidity. That distinction matters.

Now the question arises: does the current confrontation between Israel and Iran pose a risk of evolving into a crisis akin to the 1973 oil shock?

This risk materialises only if the disruption becomes both prolonged and physical. The Strait of Hormuz is a critical chokepoint, facilitating approximately one-fifth of the world’s oil trade. A significant and sustained disruption in shipping, resulting in the removal of several million barrels per day from the global supply, could lead to persistently elevated oil prices, thereby influencing inflation expectations. However, at present, oil continues to be transported without significant interruption.

The contemporary energy landscape is notably more diversified than in the 1970s. The US has emerged as a major oil producer, with countries such as Brazil and Canada contributing additional supply. OPEC+ maintains spare production capacity, and strategic petroleum reserves are in place to mitigate temporary supply disruptions.

Financial markets are inherently prone to overreacting, often pricing in worst-case scenarios immediately and subsequently adjusting if these scenarios do not materialise.

Also read: Regime decapitation in Iran is a high-voltage instrument. No guarantee of stability

Economic impact in India

The critical factor in this context is the duration of any potential disruption.

Should oil flows remain uninterrupted, the current spike is likely to be perceived as a risk premium rather than a fundamental structural shift. Conversely, a significant curtailment of supply would deepen the macroeconomic consequences, not just for India, but on a global scale.

For India, the larger lesson is structural in nature. The country‘s energy dependence translates directly into macroeconomic vulnerability. Therefore, diversifying energy supply sources, expanding storage capacity, and reducing reliance on fossil fuels are not merely environmental goals; they are essential strategies for ensuring economic stability.

This situation does not mirror the events of 1973. Nevertheless, when oil prices rise in conjunction with a strengthening dollar, India experiences immediate economic impacts. While the underlying regime remains unchanged, the exposure to these dynamics is tangible.

Bidisha Bhattacharya is an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Saptak Datta)