A financial discrepancy amounting to Rs 590 crore has emerged in government-linked accounts at a Chandigarh branch of IDFC FIRST Bank. It represents a recent point of concern within India’s financial system. This irregularity was reportedly identified during a reconciliation process initiated by Haryana government departments as they sought to close and transfer account balances. Ongoing investigations have resulted in arrests, and the bank has announced that it has reimbursed approximately Rs 583 crore, inclusive of interest, to the relevant departments, while inquiries continue.

Although the immediate financial exposure appears to have been mitigated, the analytical significance of this episode lies not in the magnitude of the funds involved but in its implications for understanding the evolving nature of risk within an expanding financial system.

Fundamentally, this is not a credit-quality story; it is a governance story.

When systems scale, risk changes form

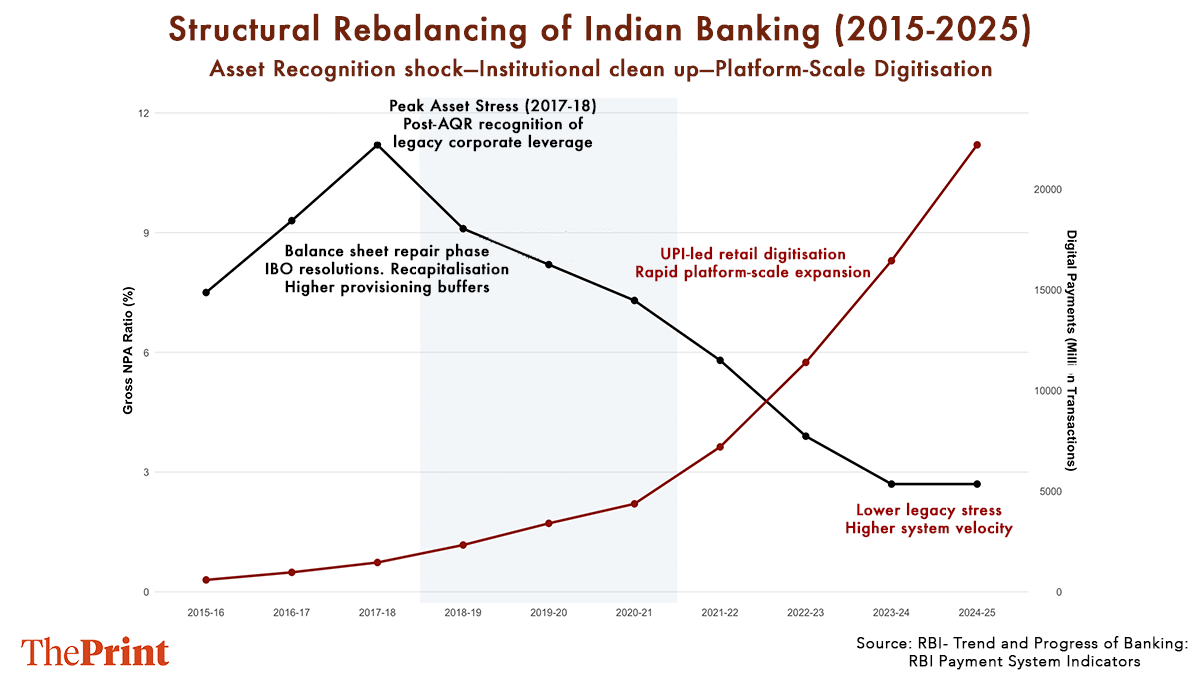

Over the past decade, India’s banking sector has experienced significant structural reforms. Asset-quality ratios have shown substantial improvement, provisioning buffers have been fortified, and capital adequacy has increased. In a previous Economix column examining the sharp decline in non-performing assets, I’d argued that the most critical phase of a banking cycle begins not during a crisis, but post- recovery—when confidence is restored, and the urgency for vigilance may diminish.

The current scenario exactly illustrates this progression. As credit stress has declined, financial complexity has escalated.

The digital payments infrastructure has expanded exponentially, with transaction volumes multiplying across UPI, RTGS and NEFT platforms. Government departments and public agencies now engage with banks through increasingly sophisticated digital channels. In such a context, operational architecture must evolve in tandem with credit discipline.

The contrast we see in the graph above is quite telling. As legacy credit stress was acknowledged and gradually addressed, digital transactions expanded at an unprecedented rate. Risk has not been eliminated; rather, it has changed its form—shifting from balance-sheet strain due to non-performing loans to the operational challenges of managing vast, rapidly evolving digital flows.

The identification of discrepancies during account closure highlights this transition. Oversight appears to have been activated at a procedural checkpoint rather than as part of continuous, real-time monitoring. In a banking system now characterised less by stressed assets and more by transaction volume, periodic reconciliation is no longer sufficient. Integrated systems, automated controls and early anomaly detection are not merely technological upgrades; they are basic governance requirements.

This does not imply systemic fragility. The prompt return of funds and the initiation of investigations demonstrate institutional responsiveness. However, in a digitally scaled financial system, responsiveness must be complemented by more robust embedded controls. The next phase of reform is therefore not focused on rectifying past loans, but on strengthening the architecture that manages the current transaction intensity.

Also read: RBI is buying time by not cutting the repo rate. Past policy needs a breather to work

Public funds and the architecture of oversight

Government departments today engage in diversified banking relationships in order to optimise liquidity management and enhance service efficiency. This diversification can bolster competition and operational flexibility. Nevertheless, the custodianship of public deposits imposes increased governance expectations. Public funds, representing taxpayer resources, necessitate procedural redundancy, including layered verification, synchronised reporting between departments and banks, and digital audit trails capable of identifying discrepancies before they escalate. The dimension of scale is of paramount importance.

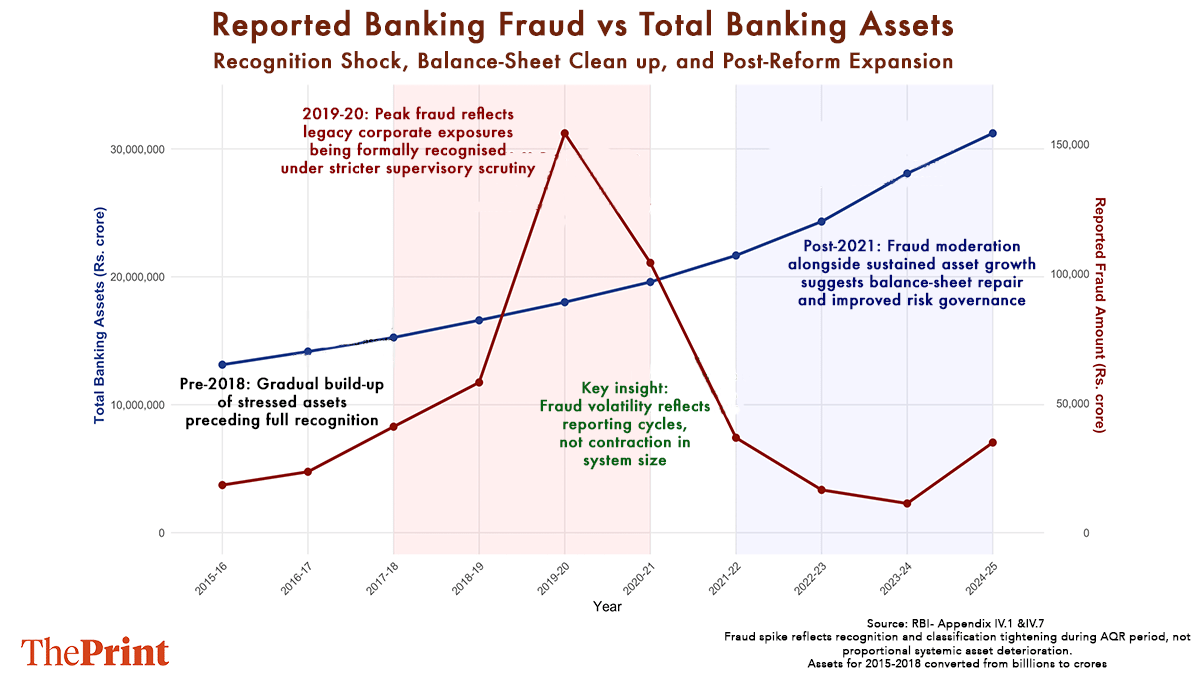

When considered in relation to the overall size of the system, individual instances of fraud may seem isolated. However, as total banking assets increase and financial networks become more intricate, the repercussions of operational failures gain systemic significance. Oversight frameworks must expand proportionately with asset growth and the increasing complexity of digital operations.

When considered in relation to the overall size of the system, individual instances of fraud may seem isolated. However, as total banking assets increase and financial networks become more intricate, the repercussions of operational failures gain systemic significance. Oversight frameworks must expand proportionately with asset growth and the increasing complexity of digital operations.

Complex systems rarely fail due to visible risks; rather, they deteriorate when institutional capacity fails to keep pace with structural complexity.

The Rs 590 crore discrepancy may remain an isolated incident; however, its true significance lies in what it signals. India’s banking system has progressed beyond mere balance-sheet repair, with strengthened capital, improved asset quality, and enhanced supervisory transparency. The next phase is not characterised by credit stress, but rather by the need for operational resilience on a large scale.

As assets expand and the intensity of digital transactions increases, governance systems must evolve at a commensurate pace. Continuous reconciliation, real-time anomaly detection, and clearly defined custodial accountability have transitioned from procedural enhancements to structural necessities. Financial systems seldom unravel during periods of visible distress; they are tested when stability returns, and complexity accelerates. While strong balance sheets are a commendable achievement, the next requirement is institutional precision.

The previous decade demanded credit discipline, whereas the forthcoming decade will demand governance depth. This transition from recovery to refinement constitutes the more rigorous test.

Bidisha Bhattacharya is an Associate Fellow, Chintan Research Foundation. She tweets @Bidishabh. Views are personal.

(Edited by Theres Sudeep)