")

Mumbai: In 2021, the Ghaziabad civic body wanted to raise funds for a tertiary sewage treatment plant to treat water for industrial use at a time when the groundwater levels were rapidly depleting. It was a project aimed at environmental conservation and sustainability, and looking at global experience, the Ghaziabad Nagar Nigam opted to try out the option of a green municipal bond though the concept was fresh in India.

Five years on, the city has completed the project, earned awards for it, repaid the first tranche of the principal amount and has significantly improved its fiscal discipline.

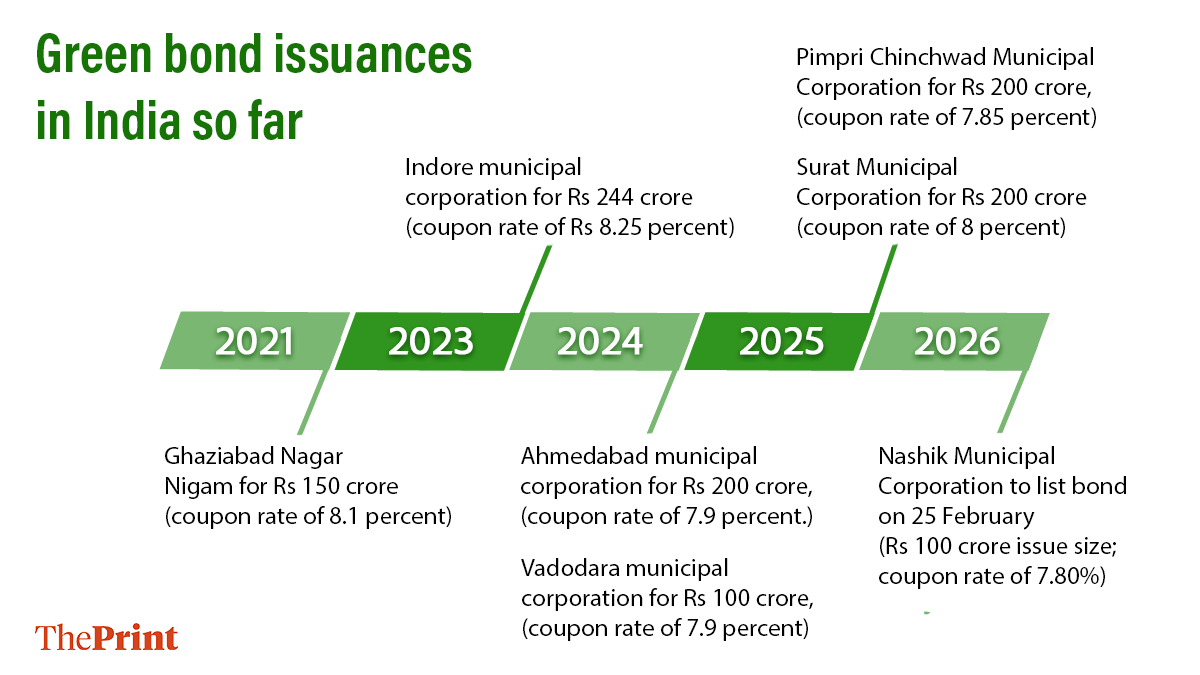

Over the years, at least five more municipal corporations have issued municipal green bonds—with financial incentives of the Union government giving impetus to the concept—and recorded pretty much the same benefits as Ghaziabad, and a sixth one—Nashik Municipal Corporation—is now scheduled to list its municipal green bond on 25 February.

Overall, only a handful of urban local bodies have opted for municipal bonds, primarily due to weak finances and bookkeeping techniques. And those who have opted for green bonds are even fewer, with the process of issuing a green bond being a lengthier and relatively complex one, requiring detailed certifications. But, those who have taken the leap have stories of success.

“With a green bond, it’s possible to take up a sustainable development project and plan to complete it in a time-bound manner rather than depend on the budgetary allocations approved by the elected general bodies of corporations. Issuing green bonds also helps local bodies be eligible for various financial incentives that the Union government gives to civic bodies tapping the markets for funds,” said Shekhar Singh, former municipal commissioner of the Pimpri Chinchwad Municipal Corporation (PCMC), which was Maharashtra’s first civic body to issue a green bond.

“Above all, issuing a green bond also brings a civic body tremendous goodwill. It puts out the intent of the city that we are working for projects that are good for the environment. When you go to the market with this intent, it creates a good feeling, a good buzz. It helps the local body show its commitment and crystallise it,” said Singh, who was last year appointed the commissioner of the 2027 Nashik Kumbh Mela.

As per India’s latest Economic Survey Report for 2025-26, municipal green bonds have the potential to unlock $2.5 billion to $6.9 billion for climate action driven by urban local bodies over the next 5-10 years.

Also read: Tale of 2 drains—how Delhi’s drinking water flows dangerously close to Haryana sewage drain 6

What are green bonds

A green bond is a fairly new global phenomenon. It is like any other bond where an issuer issues a debt instrument to raise funds from investors. The only difference is that the proceeds of a green bond are specifically set aside for environmentally sustainable “green” projects.

The very first green bond was floated by the World Bank and the European Investment Bank in 2008 marking a milestone in sustainable finance. It was only in 2013 that the first sovereign and municipal green bonds were floated by a bunch of countries and cities across the world such as Poland, Sweden and Massachusetts.

India started laying the groundwork for green bonds in 2017, and in 2021, the Ghaziabad civic body became the first municipal corporation to issue a green bond for a tertiary water treatment plant and piped water supply, and in 2023, the Indore civic body became the second urban local body in India to issue a green municipal bond for a 60 megawatt solar plant.

Following Indore, the Ahmedabad and Vadodara civic bodies issued green bonds in 2024, Pimpri Chinchwad and Surat issued green bonds in 2025, and now Nashik is preparing to list one too.

As per SEBI data, as of 31 December 2025, various entities in India, including corporate entities, had issued green bonds worth Rs 11,023 crore. However, of these, municipal green bonds accounted for less than 10 per cent.

On the other hand, as of 30 September, 2025, there were 26 outstanding issuances of regular municipal bonds amounting to Rs 3,783.90 crore.

Several of the corporations that have issued a green bond had previously issued a regular municipal bond to raise funds. For instance, the Surat municipal corporation tapped the bond market in 2019 to raise Rs 200 crore, and then opted for a green bond to raise a second tranche of funds from the markets in 2025.

Surat civic chief M. Nagarajan told ThePrint, though the paperwork and certifications required are more in the case of green bonds, the financial incentives offered by the Union government for issuing green bonds encourage local bodies to opt for them.

“In green bonds, a third party review/certification is required, which is a detailed process. Accordingly, we obtained a third-party review from KPMG and a green certification from Climate Bonds Initiative. In the case of issuance of green bonds, the merchant banker carried out detailed due diligence of information memorandum which was not required at the time of the first tranche (regular municipal bonds) in 2019,” Nagarajan said.

According to a March 2025 report by the Council on Energy, Envinronment and Water (CEEW)-Green Finance Centre, 60 per cent of the municipal bonds issued in India in the last decade were actually green, but weren’t labelled green bonds.

“This represents a missed opportunity that could have led to lower borrowing costs and dedicated climate-focused investors,” the report said.

‘Greenium’ yet to be established

An official with the Maharashtra government who did not wish to be named said the jury is still out on whether green bonds have brought any significant financial benefits for local bodies over regular municipal bonds.

Green bonds should typically come with a ‘greenium’ (green premium), which means they should have lower interest rates, or yields, compared to conventional bonds. The idea is that investors are willing to accept lower returns for the environmental benefits that they are helping create.

“Green bonds should give a dividend where investors would like to give a discount to the mark up price on the yield. That’s not necessarily happening. On the other hand, a green bond comes with a higher compliance cost. Local bodies have to hire consultants for a green rating of the project, SEBI has specific guidelines, etc.,” the official said.

India’s market regulator, the Securities and Exchange Board of India (SEBI), first published disclosure norms for issuance of green bonds in 2017, which it later updated in 2023. In 2022, the Union finance ministry came up with a framework for sovereign green bonds.

SEBI’s framework clarifies aspects such as what qualifies as a green bond, the disclosures needed about environmental objectives, and preventing any misuse of the green label.

Issuers have to clearly define to which category of green projects the bond proceeds will go. These categories have to be recognised by SEBI as green categories. Bond issuers have to disclose the decision-making process behind the project. The funds raised have to be exclusively used for the stated green projects, and need to be tracked and managed separately. There is also a significant bit of reporting involved as issuers have to give periodic updates on the proceeds and the project status.

SEBI norms also mandate the issuer to have second party opinions, verifications and certifications.

As per the Economic Survey Report (ESR) , cross-country experience shows that the ‘greenium’ depends not just on investor intent, but on market design, liquidity, credibility and reporting frameworks.

The report further said, in the European Union, it has been stable at about 2 basis points, in the United Kingdom it is episodic—small, but positive. In France, it has been between 2 and 5 basis points, while in India it has varied between 0 and 6 basis points. As per the ESR, the main challenges in India are limited secondary market liquidity, smaller issue sizes and fragmented issuances, lagged impact reporting and green bonds largely held to maturity.

The ESR said, “In India, the modest and episodic greenium observed so far does not necessarily reflect a lack of investor interest. Deepening secondary market liquidity, consolidating issuances into benchmark sizes, and strengthening post-issuance reporting can help translate into a more significant cost-of-capital advantage over time.”

Also read: Capital trouble: Delhi groundwater crosses ‘over exploited’ mark, warns RBI report

Ghaziabad’s green script

By 2021, the Ghaziabad Nagar Nigam knew that it was facing a problem of rapid groundwater depletion due to overexploitation owing to rapid urbanisation and the mushrooming of industries. It was a situation that was only likely to get worse. In this backdrop, the civic body decided to take up a project to reduce the dependence of industries on the city’s water resources.

It planned a tertiary sewage treatment plant with a treatment capacity of 40 million litres a day to be connected to a 88-km pipeline network. The plant was to sell treated water to 1,445 industrial units.

The project uses advanced membrane filtration technologies such as micro filtration, ultrafiltration, nanofiltration and reverse osmosis, and is only the second such plant in India after Chennai, Ghaziabad civic chief Vikramaditya Singh Malik told ThePrint.

The total cost of the project was estimated at Rs 319.14 crore.

“We wanted to make the plant fully operational soon and decided to explore alternative sources of funding. Since this was a project that was a genuine need of the city, aimed at sustainability, we decided to opt for a green bond,” Malik said, adding that the Union government’s promised financial incentive for floating a green bond also helped.

That’s how the Ghaziabad Nagar Nigam came to be India’s first municipal corporation to issue a green bond and raise Rs 150 crore. The issue was oversubscribed more than four times.

The civic body faced several challenges along the way such as convincing the corporation’s political body and the heads of departments about the issue. Gathering all information and documents—given the very little digitisation at that time in the corporation—was also a lengthy process.

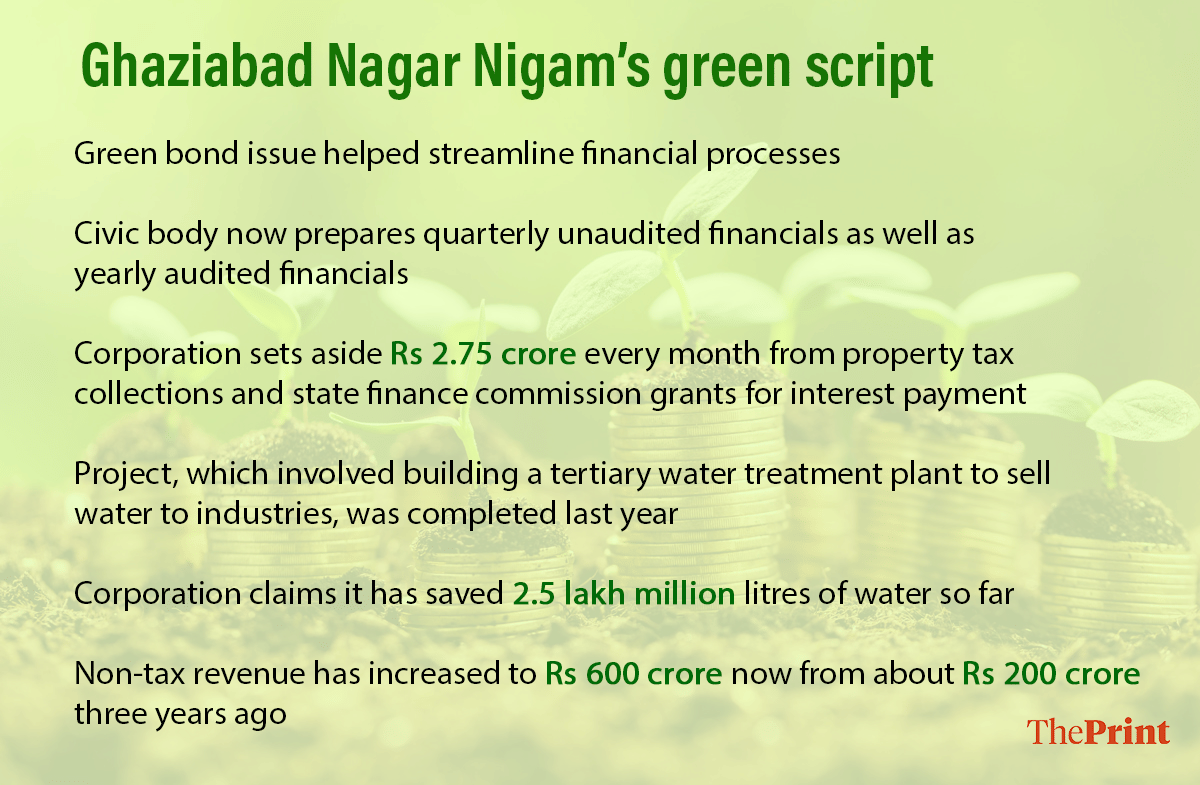

But since then, the corporation has kept its credit rating at AA, ensured all deadline payments and milestone payments are met on time, and brought about tremendous changes to improve its bookkeeping discipline.

Every month, the Ghaziabad Nagar Nigam sets aside Rs 2.75 crore from its property tax collections and state finance commission grants to ensure there are funds for timely payments on due dates.

There’s also a dedicated special reserve account where the corporation puts in two years’ worth of interest payments as a reserve; and the incentive of Rs 19 crore that it got from the Union government for issuing a green bond has been kept as cash collateral.

The civic body completed the project about four months ago and, as per the civic body’s internal estimates, has saved 2.5 lakh million litres of water since then.

“Last year, we paid the first tranche of the principal amount of Rs 21 crore (there are a total of seven installments) and the second one is due this year. Apart from raising funds and increasing transparency, issuing a green bond has brought about a lot of fiscal discipline in the corporation. Normally, urban local bodies are not good at it,” Malik said.

“Urban local bodies have to prepare a lot for issuing bonds. There was a time when we would prepare unaudited balance sheets once in 3-4 years to now when we are preparing our quarterly unaudited financials and yearly audited financials within the prescribed timelines. Previously, it used to take almost a year to get the accounts edited,” Malik said.

With good fiscal practises and planning, the corporation has also increased its non-tax revenue to about Rs 600 crore now from less than Rs 200 crore in 2023.

“In 2021, this figure was not even Rs 150 crore. The corporation didn’t have enough funds and was reliant on grants from the Centre and state, which are for specific projects. We are now moving towards self sustainability,” Malik said.

How others have followed

Most of the civic bodies which have opted for green bonds have done so mainly due to the Union government’s incentives. The issue has helped them accelerate projects that the bonds were raised for.

For instance, in December last year, the Nashik Municipal Corporation raised Rs 200 crore in municipal bonds through a private placement—a non-public issue when a company sells stocks or bonds directly to a select group of investors. The corporation named it ‘Clean Godavari bond’ as it was meant for various infrastructure development projects around the Godavari river.

Now, the Nashik civic body, which is preparing to host the Simhasta Kumbh Mela in 2027, is preparing for a second issue—a green bond open to retail investors, to raise another Rs 200 crore.

“We get a certain incentive from the Union government for the first bond issue. For a second issue, we can avail a financial benefit if it is a green bond or a social bond. So, we decided to opt for a green bond now because we are incentivised to do so,” Nashik Municipal Commissioner Manisha Khatri told ThePrint.

The proceeds from the green bond will go towards improving the core water infrastructure. The civic body is hoping to reduce its non-revenue water losses form 47 per cent to 20 per cent.

“We are setting up a water treatment plant of a much higher capacity, laying down water pipelines. It will help us for Kumbh as well as to ensure 24/7 water supply in the city,” Khatri said, adding that the project implementation is already underway and the civic body aims to complete it by March 2027.

The total project cost is Rs 397 crore.

In a Lok Sabha reply to an unstarred question by Hema Malini in August 2025, the Union Ministry of Housing and Urban Affairs said the government gives an incentive of Rs 13 crore for every Rs 100 crore of municipal bonds, including green bonds issued, capped at Rs 26 crore. A second-time incentive is also available at Rs 10 crore for every Rs 100 crore of bonds issued, capped at Rs 20 crore.

So far, the ministry said, urban local bodies have raised Rs 5,359 crore through municipal bonds and green bonds to finance infrastructure projects. These have been issued by 18 urban local bodies, namely Agra, Ahmedabad, Amaravati, Bhopal, Chennai, Gandhinagar, Ghaziabad, Hyderabad, Indore, Lucknow, Rajkot, Prayagraj, Pune, Surat, Vadodara, Varanasi, Vishakhapatnam and Pimpri Chinchwad. The ministry has so far released Rs 377.33 crore as incentive, including for the green bonds issued by Ahmedabad, Ghaziabad, Indore, Pimpri Chinchwad and Vadodara.

In the 2026-27 Union budget, Finance Minister Nirmala Sitharaman also announced a new Rs 100 crore incentive for high-value municipal bond issuances, setting Rs 1,000 crore as the threshold.

Additionally, the Union government has also set up an Urban Challenge Fund to incentivise civic bodies to raise minimum 50 per cent of the cost from the market for projects related to water, sanitation, renewal of business districts and heritage precincts, transit-oriented development, climate resilience and development of growth hubs. Such projects will be eligible for some central assistance.

“After issuing a green bond, we also applied for central assistance from the urban challenge fund. While we have made ample provisions for timely payment of interest and principal, if granted, the urban challenge fund incentive will be enough to effectively take care of our interest commitments on the green bond, which leaves the civic body in a strong position,” Singh, former civic chief of the Pimpri Chinchwad municipal corporation, said.

The civic body raised funds through green bonds for a ‘Harit Setu’ project under which the civic body is redesigning footpaths, building cycle tracks and increasing green cover in the Nigdi area. Part of the funds will also be used for the redevelopment of the Telco Road in the corporation’s jurisdiction. Both projects, it says, are aimed at encouraging non-motorised transport and improving last-mile connectivity.

For Surat, three of the six works for which it raised funds through green bonds have already been completed. These include installation of a 10 megawatt ground-mounted solar power plant in the Banaskantha district, development of a depot for electric bus operations at Kolad and upgrading a water treatment plant at Variav and Ranger. The other three projects that are in progress include a wind power plant, a centralised dry and wet waste processing plant and the construction of an intake well and transmission line.

“The issuance of green bonds has helped in financing climate-resilient infrastructure in the city. Further, it has helped Surat get an incentive of Rs 20 crore from the Union government. It also showcases a city’s commitment to sustainable development, enhancing the reputation of the civic body,” Surat civic chief M. Nagarajan said.

He added, the rigorous reporting requirements associated with green bonds, though tedious, are helpful in more ways than one.

“We need to give regular updates on how funds are used. It improves accountability, and investor trust,” he added.

(Edited by Viny Mishra)

Also read: Delhi govt’s Yamuna cruise sails into a storm of doubts. Luxury ride or ‘dystopia tour’?

Thank you for publishing such informative stories.

Subscription paisa vasool!!