The Reserve Bank of India (RBI) raised the repo rate by 35 basis points in its December policy — the fifth consecutive increase this year. With the latest hike, the repo rate has reached 6.25 per cent. The stance of the policy was retained as ‘withdrawal of accommodation’.

While the projection for inflation has been retained at 6.7 per cent for this year, the projection for growth has been revised downwards from 7 per cent to 6.8 per cent. Even though the headline inflation has seen a moderation, RBI’s Monetary Policy Committee (MPC) is likely to retain its focus on inflation as going by the RBI’s own projections, inflation is likely to remain elevated in the next three quarters.

The clear commitment to break the persistence of core inflation and anchor inflation expectations is a welcome development.

Concern on the inflation front, optimism on the growth prospects and anticipation of rate hikes by the US Federal Reserve implies that monetary policy tightening by the RBI will continue.

Also read: India’s GDP growth slowed to 6.3% in Q2 — why this isn’t as worrying as it sounds

Moderation in headline inflation but stickiness in core inflation more

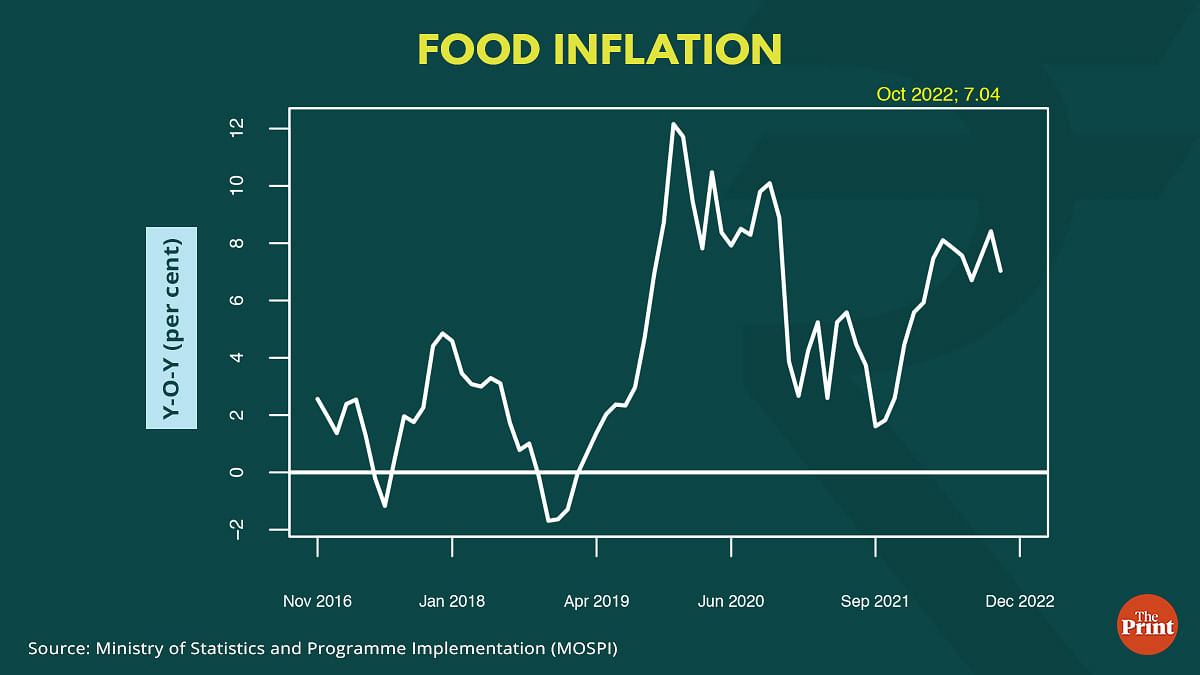

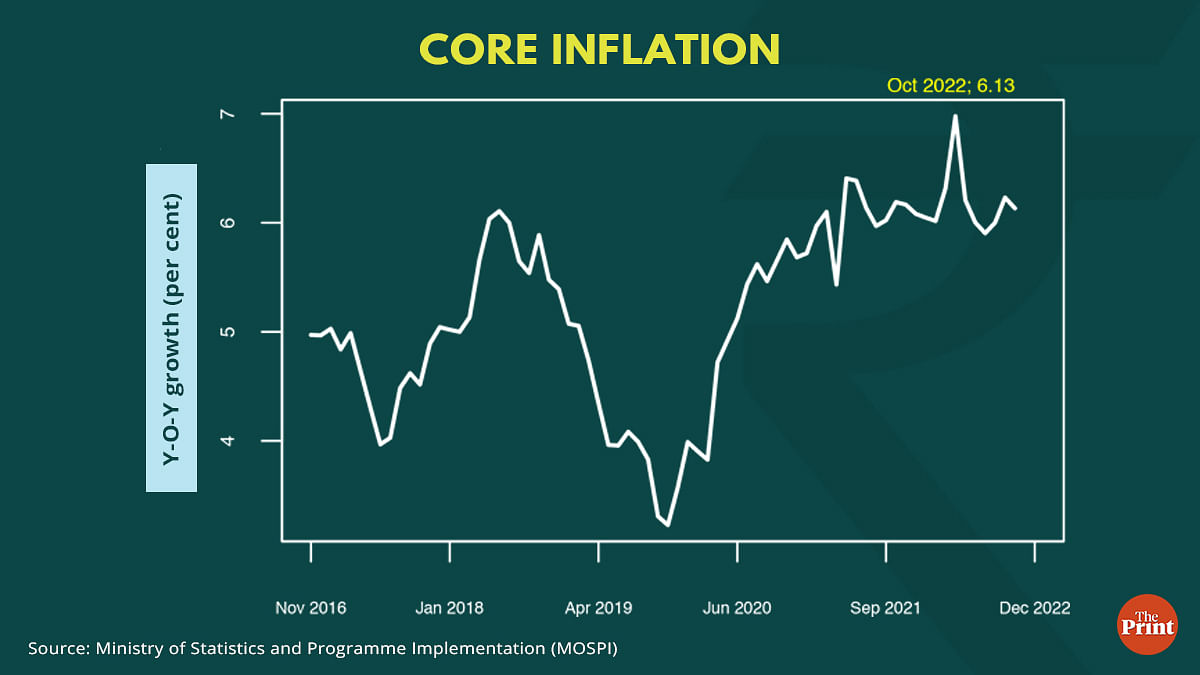

Consumer Price Index based inflation moderated to 6.8 per cent in October from 7.4 per cent in September. The fall in headline inflation was limited to food and fuel. Core inflation (CPI excluding food and fuel) continued to remain elevated at 6 per cent.

The decline in food inflation was also not broad-based. While inflation in vegetables and edible oils eased, that of cereals surged to more than 12 per cent. Prices of cereals, particularly of wheat and rice are expected to remain elevated owing to dip in stocks of wheat and rice with government agencies.

Core inflation has remained persistent at above 6 per cent for more than a year now. In particular, inflation in categories such as ‘household goods and services’, ‘personal care and effects’, ‘recreation and amusement’ has been above 6 per cent in October.

While globally input prices are witnessing a moderation, companies seem to be passing the accumulated input costs to consumers. Prices of metals, chemicals, vegetable oils, which are the key inputs used in the manufacturing process have started to ease but manufacturers and service providers are unlikely to pass on the benefits to the final consumers in the immediate to short-term.

Thus, core inflation is likely to remain sticky in the coming months.

Uncertainty in global inflation

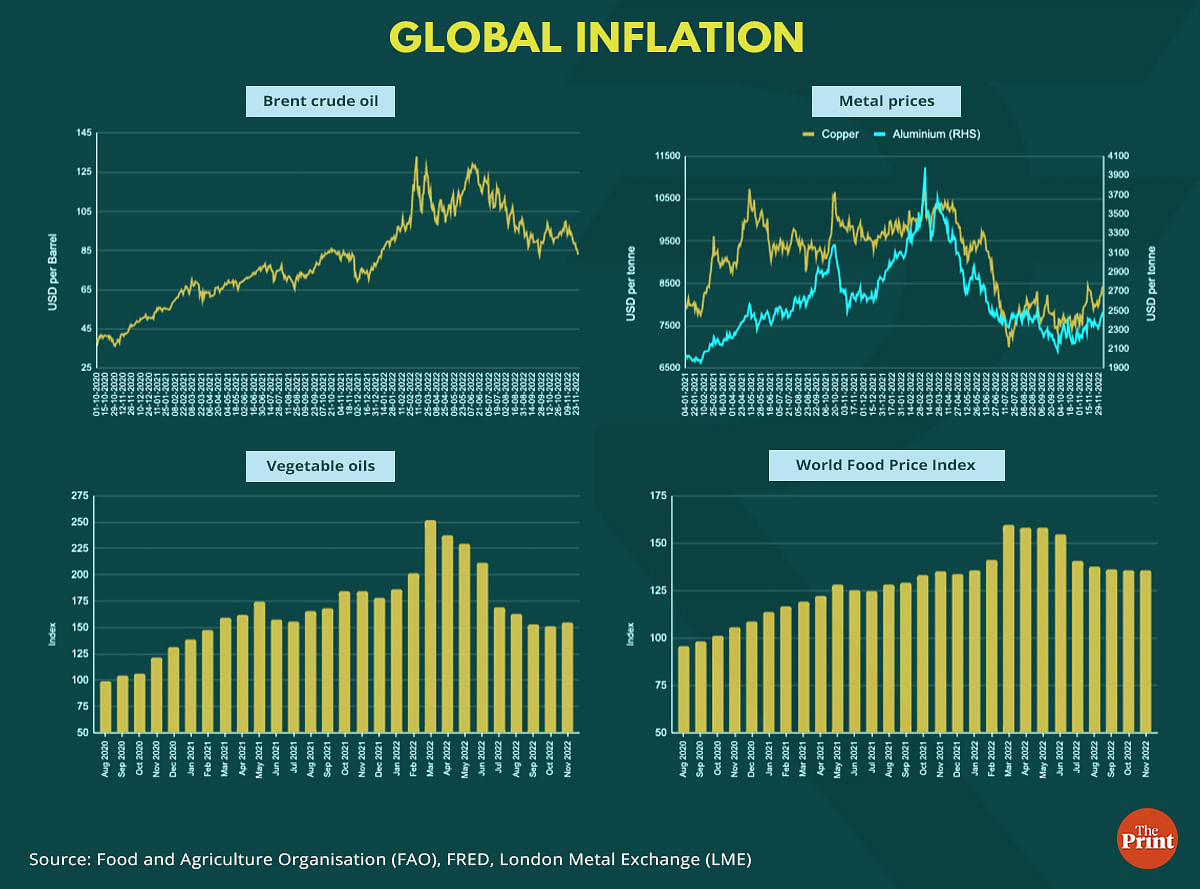

The FAO Food Price Index (FFPI), a gauge of the monthly change in international prices of a basket of food commodities, has seen a steady decline after peaking in March. The data for November indicates that while cereals and dairy and meat sub-indices saw a decline, vegetable oil price index saw an uptick. The movements in these sub-indices in the coming months would have a bearing on the domestic food inflation.

While global crude oil prices have seen a dramatic decline in November, the future trajectory will depend on a host of factors such as the European Union’s (EU) ban on seaborne exports of Russian crude, the price caps by the G-7 countries on exports of Russian crude and the OPEC+ decision on future production cuts. The OPEC+ could signal deeper cuts to prevent a significant fall in prices. The RBI has assumed an average crude oil price (Indian basket) of US$ 100 per barrel, to base its inflation projections.

Rate hike as a rupee defence measure

The policy rate hike by the RBI is in alignment with the hawkish commentary by the advanced economies central banks. The rate hike will lend support to the rupee ahead of the US Federal Reserve’s meeting next week where it will announce another rate hike.

After staging a recovery in November, the rupee has come under pressure due to stronger dollar and concerns around a persistent current account deficit. Narrowing interest differential between India and US could hurt the rupee by triggering outflows of foreign capital.

In a recent speech at the Brookings Institute, the Fed Governor signalled that while there could be a scope for reduction in the pace of rate hikes, the rate hike cycle could be longer than anticipated earlier. Governor maintained that while goods inflation has seen a sharp decline, services inflation would remain the priority going forward. Thus, while the quantum of rate hikes may see a reduction, the rate hike cycle could continue longer.

Growth prospects encouraging

Despite a downward revision in the growth projection for the current financial year, growth prospects look bright. This has given the RBI the headroom to focus on managing inflation.

Prospects of a good rabi harvest, rebound in the contact-intensive services signal sustained revival in growth. Broad-based growth in credit including a sharp pick up in credit by large industries should bolster investment activity.

High-frequency indicators such as the Purchasing Managers’ Index (PMI) for the manufacturing and the services sector touched a three-month high in November signalling increase in output and a strong domestic demand.

The World Bank has also revised upwards its GDP growth forecast from 6.5 per cent to 6.9 per cent for the current financial year on account of higher resilience of the economy to global shocks.

Overall, while the peak of inflation may be behind us, the vigil on inflation is desirable.

Radhika Pandey is a consultant at National Institute of Public Finance and Policy.

Views are personal.

Also read: India’s public sector banks are laughing all the way to profits. But new stress can interrupt