On 27 June, the government changed the laws governing cooperative banks through an ordinance — a positive move towards reforming the Reserve Bank of India’s oversight of banks, and enabling resolution.

The ordinance does three things. First, it changes the way the RBI can intervene in failing banks to protect deposits. Second, it allows cooperative banks to raise capital through issuing securities. Third, and most important, it increases the power of the RBI over cooperative banks.

Currently, the RBI can intervene in failing banks only after placing them under a moratorium. During the moratorium, depositors cannot access their funds. Naturally, this distresses depositors who can’t access their own money. The requirement for a moratorium is why, in the Yes Bank resolution, depositors had limited access to their accounts.

The ordinance changes this. Now, the RBI can intervene in a failing commercial bank (usually by merging it with another bank) without placing the failing bank in a moratorium. Depositors’ money will not be stuck. One day, they will wake up and find that their bank has been taken over by another. However, the new bank will continue to operate their accounts seamlessly.

Also read: Protect bankers, act against miscreants with full force of law: Finance ministry tells states

India’s silent banking crisis

The most significant reform in the ordinance is RBI’s increased control over cooperative banks. India has been undergoing a silent banking crisis — between 2013 and 2018, 127 banks had to be shut down by the RBI. Most of them were unable to pay their depositors. More than four lakh depositors had to be reimbursed through the deposit insurance system.

The reason that this did not attract national attention is that the ones that failed are cooperative banks.

Spread out mostly through rural India, these banks are tiny compared to commercial banks which dominate the urban landscape. However, cooperative banks serve India’s rural and poor populations, so when they fail, the financial disruption to the lives of depositors is probably worse.

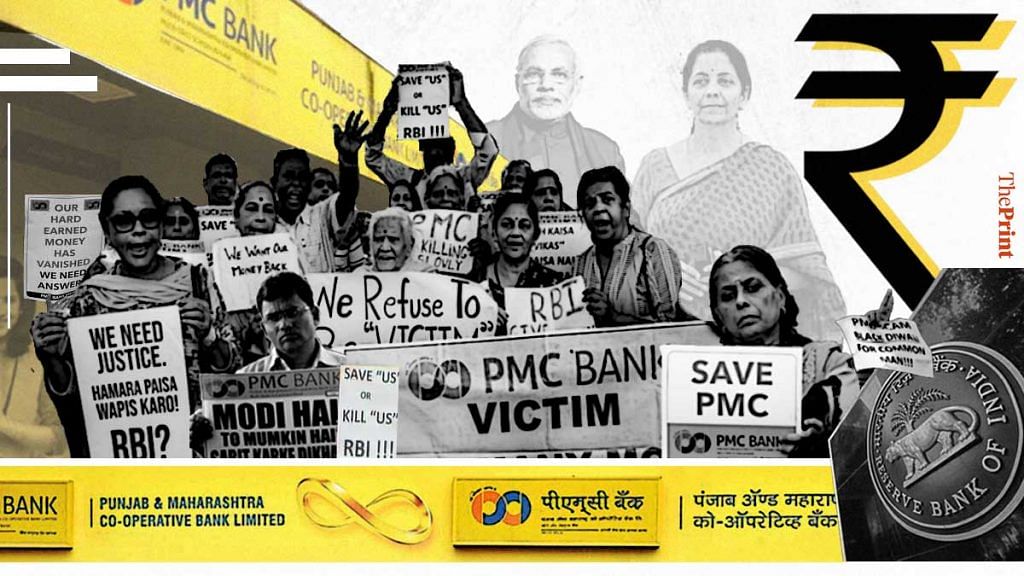

Sadly, it took the failure of the Punjab & Maharashtra Co-operative Bank (PMC Bank) last year to bring about legal changes. PMC Bank, unlike other cooperative banks, had aggressively expanded into India’s financial capital, Mumbai. When it failed, it left a large number of urban depositors in the lurch, which brought about the political will needed to change the system.

Who governs cooperative banks, states or Centre?

Cooperative banks sit uncomfortably in India’s constitutional structure. The incorporation, regulation and winding up of cooperatives is a subject for states to legislate on (Entry 32 of List II of the Seventh Schedule), while banking is supposed to be governed by laws made by the Union legislature (Entries 43 and 45 of List I of the Seventh Schedule). The division between state and central responsibilities raises the uncomfortable question: Who regulates cooperative banks? The states or the Union?

The problem has been plaguing India since the beginning of the republic. An uneasy system prevailed in the Banking Regulation Act, where the RBI would have some powers over the banking functions of the cooperative. In contrast, the regulation of the management of the cooperative is left to the states. States usually have a registrar of cooperatives (analogous to the registrar of companies) who exercises control over the election and removal of management of cooperatives. The provisions of the Banking Regulation Act would apply in a truncated and modified way to cooperatives, subject to many conditions.

The set-up makes it impossible to separate the management of the bank from the operations of the bank. If the management is incompetent, or worse, is stealing from the bank, the regulator cannot take appropriate action. RBI has to regulate the banks but cannot take any action against the bank’s management, or close it down. The rot at the top is outside the reach of the regulator.

Also read: How a reform on Modi govt agenda can protect your deposits & keep banks from failing

How the ordinance changes things

The ordinance changes this uneasy tension between state laws governing cooperative management and the RBI which regulates the banking functions.

From now on, the Banking Regulation Act (with some modifications) will enjoy supremacy over cooperative banks. The power of RBI to remove management or draw up plans to merge/dissolve cooperative banks will override the power of the state registrar of cooperatives.

The change does not completely level the playing field between cooperative banks and commercial banks, but reduces the anomalies substantially. With additional powers over the banks, the RBI may be in a better position to prevent a rerun of the PMC Bank scam.

Another set of provisions allows cooperative banks to issue shares, debentures and other securities. This will allow cooperative banks to access financial markets. The provision to allow cooperative banks to raise capital through securities is another step towards making them safer. Equity capital acts as a buffer to protect depositors from smaller losses of the bank. The share-holders absorb the first losses. Only if the losses are more than the equity capital do the depositors lose money. That is why laws require commercial banks to maintain equity capital equal to 9-12 per cent of their deposits.

Before this ordinance, cooperative banks were exempt from this requirement, and usually had deficient equity capital. Now, the RBI can require such cooperative banks to raise capital (like commercial banks) as they grow.

The ordinance gives RBI more powers over cooperative banks. However, for them to be regulated and supervised better, the central bank needs to ramp up its supervisory capacity.

Its failures in detecting scams in Yes Bank and other Scheduled Commercial Banks, where it had the power to do so, show that there will still be many challenges.

Ila Patnaik is an economist and a professor at the National Institute of Public Finance and Policy.

Shubho Roy is a researcher at the University of Chicago.

Views are personal.

Also read: Private banks are also in trouble, Modi govt must act now to set up resolution capability