Banks have had to write off three quarters of loans, after selling the operating company of the Jharkhand power plant.

Deep in the jungles of eastern India lies an abandoned power plant, a warning symbol for the $38 billion of additional bad loans which are about to engulf the country’s banks.

Like many of India’s power stations, the Jharkhand project had all the markings of success when a group led by State Bank of India lent about $700 million five years ago to build it. There’s abundant coal and water in the area, a rail track was set to run through the premises, and its promise of 1,080 megawatts of electricity was alluring in a country that faces persistent power shortages and blackouts.

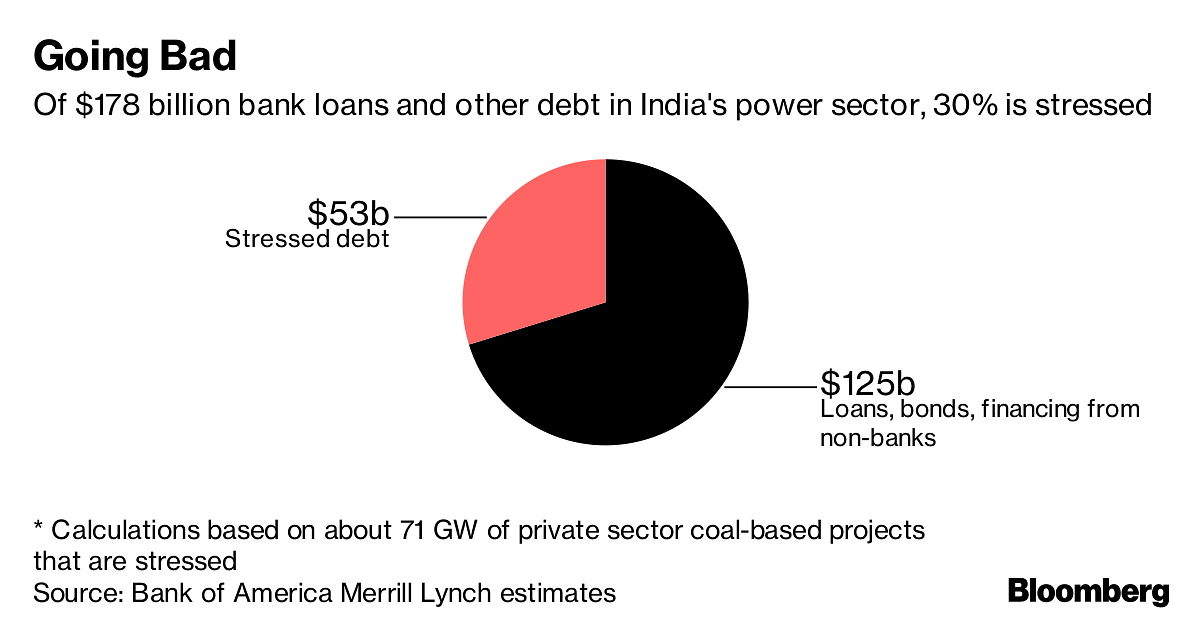

Yet today it stands deserted and Indian banks have had to write off three quarters of their loans, after selling the operating company to a specialist in distressed debt. Haircuts of that magnitude are now expected across the whole power sector in India, according to Bank of America Merrill Lynch, suggesting local banks face a new $38 billion wave of losses. That would be more than four times the $9 billion they’ve written off from a previous tide of bad loans from India’s troubled steel sector.

“It is the largest bad-loan risk in the country,” said Vinayak Bahuguna, chief executive officer of Asset Reconstruction Co. of India Ltd., the firm which bought the Jharkhand plant from its creditors in 2015, about two years after construction stopped. “Just as the banks are beginning to put the stress on steel accounts behind them the power accounts are emerging as the new pain point.”

India’s banks, which have some of the highest stressed asset ratios globally, are under mounting pressure from regulators to clean up their books as the government attempts to revive loan growth and boost the economy. That is likely to intensify the reckoning they face from lending to India’s power sector, which is plagued by fuel shortages and difficulties negotiating long term supply contracts with the country’s debt-laden electricity distributors.

The problem is especially acute for state-owned banks, which are already reeling under the weight of their problem debts. Out of 21 government-controlled lenders, accounting for more than two thirds of the total loans in India, 19 reported losses in the three months to 31 March.

After taking haircuts of between 40-60 per cent on their loans to troubled steel projects, the banks face a 75 per cent loss ratio on their power lending, according to the Bank of America Merrill Lynch estimate.

Many banks are unwilling to accept losses of that magnitude, leading to a tussle between lenders and potential buyers over valuations. Such disputes have delayed a solution for power projects such as those owned by Lanco Infratech Ltd. and Jaiprakash Power Ventures, which together account for some of the biggest stressed loan accounts in India.

“Sales will happen if banks take a more realistic approach on valuations they seek and are willing to take decisive action,” said Hemant Kanoria, chairman of India Power Corp., whose bid for the Jharkhand power plant was rejected by bankers citing different views on the valuation.

For some projects, banks are proposing to wait out the problems in the hopes that the situation will improve. At a meeting in Mumbai last month, lenders including State Bank of India, Bank of Baroda and Punjab National Bank suggested the creation of a new company to take over management of about 10 power projects, until demand for the assets picks up.

But recovery hinges more on addressing the fundamental issues that plague the Indian power sector, notably the difficult condition of many of the state-owned distribution firms.

“Ultimately the question is whether the distributors will start buying power and paying,” said PK Gupta, managing director at State Bank of India, the nation’s largest lender, which has a so-called watch list of about $1.6 billion of problematic power sector loans.

A recent proposal by the Reserve Bank of India to tighten up further on when lenders have to recognize loan losses elicited protests from Indian power companies, which feared it would force many more into insolvency. The Association of Power Producers wrote to RBI Governor Urjit Patel earlier this year to say the tougher rules would propel projects generating 75 gigawatts of electricity, about a fifth of India’s installed capacity, into bankruptcy.

Back at the Jharkand site, there’s little hope that the project will start providing power soon. On a visit last month, the only sign of life was a group of about a dozen private security guards protecting the rusting structure from thieves. – Bloomberg

If the so called Govt. understand what a backward integration can do, no such projects could go down the drain. Weather it is State or Central Govt. neither have the political/management/administrative skills and vision to deliver.

Good One. We really hope that they understand this now