Here’s a market-by-market look at how a trade war will affect Asian debt.

When it comes to Asian sovereign bonds it’s better being at the epicentre of a U.S.-China trade war than on the fringes of the quake radius.

Chinese and South Korean notes are climbing as the rise in protectionism batters their stock markets, drives a flight to safety and, in China’s case, prompts a more dovish monetary policy. Indonesia, India and the Philippines, by contrast, are more removed from the turbulence but are suffering from currency vulnerability due to current-account deficits.

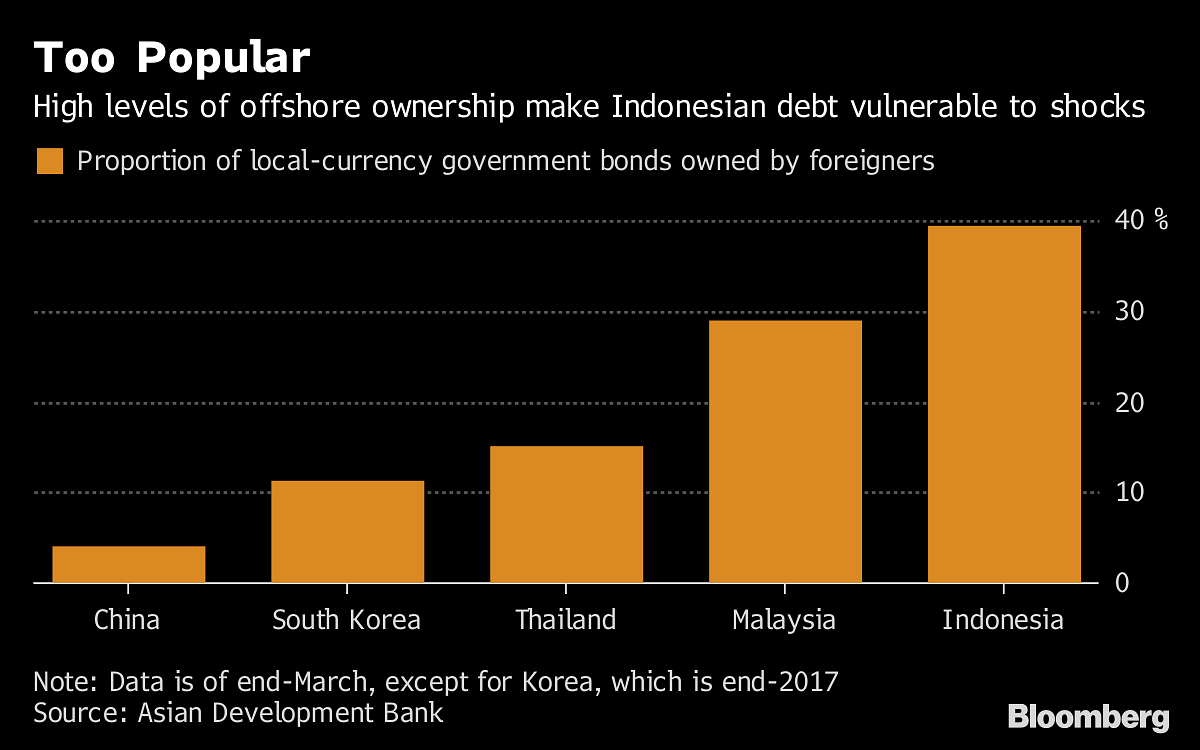

The proportion of foreign ownership is the other big differentiator as the simmering tension threatens to boil over into all-out war on July 6 when a deadline for U.S. duties kicks in. China and Korea — plus Thailand and India — benefit from a relatively small offshore presence, while Indonesia is at risk.

“Markets with a deep onshore investor base will be better insulated from swings in foreign portfolio flows,” said Jennifer Kusuma, a senior Asia rates strategist at Australia & New Zealand Banking Group Ltd. in Singapore. A relatively benign economic outlook for China, South Korea, Thailand and Malaysia will aid their bonds as investors avoid risk-taking, while Indonesia, India and the Philippines are exposed, she said.

Here’s a market-by-market look at how a trade war will affect Asian debt.

China

Chinese government debt is already benefiting from the trade spat as stocks have fallen into a bear market and a reserve-ratio cut has boosted liquidity. Foreign investors bought the bonds at the fastest pace since September 2016 last month, while the 10-year yield reached a 14-month low of 3.47 percent on July 2.

The notes stand to gain if the People’s Bank of China eases policy further to safeguard growth. Further declines in the yuan are a risk for foreign investors, but the PBOC pledged on Tuesday to keep the currency stable.

“Any worsening of the China-U.S. trade spat would be good news for sovereign bonds, as it would pressure the economy and weaken risk appetite,” said Meng Xiangjuan, an analyst at SWS Research Co. in Shanghai. “But as investors already have a very pessimistic outlook on the trade tensions, the room for any sharp declines in yields is limited,” she said, adding that the 10-year yield could drop to as low as 3.40 percent in the second half.

South Korea

South Korean sovereign bonds typically benefit from a flight-to-quality in times of stress and the trade war is no exception. Overseas investors pumped a net $15.8 billion into the notes last quarter, the most in five years, helping push the 10-year yield down six basis points to 2.56 percent. The country posted a surprise drop in exports in June, a sign the uncertainty may be starting to affect shipments to China.

“South Korea will be directly hit by a trade war and, should it continue to escalate, it will be difficult for the Bank of Korea to raise interest rates,” said Kong Dongrak, a fixed-income strategist at Daishin Securities Co. in Seoul. While Daishin is still forecasting one rate increase in the second half, it’s “open to the possibility of zero BOK hikes this year,” he said. Kong is recommending investors keep buying Korean debt but notes the won, which fell 4.4 percent against the dollar last quarter, remains a risk.

Indonesia

Bank Indonesia has raised its policy rate by 100 basis points since mid-May to defend the rupiah, and most analysts are forecasting there will be more hikes. With almost 40 percent of its bonds owned by global funds, Indonesian debt suffers the most in Asia when foreign money leaves emerging markets.

Elevated yields — the 10-year reached an 18-month high of 7.9 percent last week — are making the notes attractive, but the trade war and dollar strength make the global environment a lot less forgiving, said Eugene Leow, a fixed-income strategist at DBS Bank Ltd. in Singapore . Yields will probably move “sideways” in the second half, Leow said.

India

India’s policy of not letting much foreign money into its sovereign bond market — only around 5 percent of the notes are offshore-owned — acts as a buffer in times of stress. While the notes haven’t been immune to worsening sentiment pushing down the rupee — there were $6.4 billion of outflows from debt last quarter — the oil price will probably remain the market’s biggest driver.

Rupee Hits Record Low as India Pays for Insatiable Oil Demand

A trade war could result in economic inefficiencies leading to faster inflation that would be bad for bonds, but it could also damp growth, which would be good for debt, said Sandeep Bagla, associate director at Trust Capital Services India Pvt. in Mumbai. He forecasts the 10-year yield will fall to 7.25 percent, from 7.88 percent on Tuesday, by the end of the year.

Thailand

Thai bonds have been popular in recent years due to the country’s large current-account surplus and the resilient baht, and managed to attract inflows in June. While a trade war will likely lead to a drop in Thai exports and a narrower excess, the relatively low level of overseas ownership should act as a cushion, said Kobsidthi Silpachai, head of capital market research at Kasikornbank Pcl in Bangkok.

Kasikornbank forecasts the Bank of Thailand will stay on hold for the rest of this year and sees the 10-year yield rising to 3 percent at year-end, from 2.56 percent on Wednesday.

Malaysia

A preponderance of hold-until-maturity Islamic investors and the possibility of a dovish shift from the central bank means Malaysian debt may do comparatively well as protectionism rises. Elevated oil prices are also supporting the crude exporter and acting as a buffer for the local currency.

Ringgit bonds may be relatively resilient to a trade war as much of the investor base — Islamic funds and lenders, regional central banks and sovereign wealth funds — are long-term holders, said Winson Phoon, the head of fixed-income research at Maybank Kim Eng Securities Ltd. in Singapore. The 10-year yield, at 4.19 percent on Wednesday, will probably move in a range of 4 to 4.10 percent over the next three to six months, he forecast.

Philippines

The trade dispute will keep the pressure on Philippine government bonds due to the nation’s twin deficits and high inflation, said Arup Ghosh, a senior Asia rates strategist at Standard Chartered Bank in Singapore.

Foreign interest in the debt remains light amid peso underperformance, issuance pressure and tighter funding costs, said Ghosh, adding that he saw upside risks to inflation due to the weakening currency and higher oil prices. – Bloomberg